- Hong Kong

- /

- Real Estate

- /

- SEHK:1972

Here's Why It's Unlikely That Swire Properties Limited's (HKG:1972) CEO Will See A Pay Rise This Year

Key Insights

- Swire Properties' Annual General Meeting to take place on 7th of May

- Total pay for CEO Tim Blackburn includes HK$3.92m salary

- The total compensation is similar to the average for the industry

- Swire Properties' EPS declined by 14% over the past three years while total shareholder loss over the past three years was 16%

Shareholders will probably not be too impressed with the underwhelming results at Swire Properties Limited (HKG:1972) recently. At the upcoming AGM on 7th of May, shareholders can hear from the board including their plans for turning around performance. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. We present the case why we think CEO compensation is out of sync with company performance.

See our latest analysis for Swire Properties

How Does Total Compensation For Tim Blackburn Compare With Other Companies In The Industry?

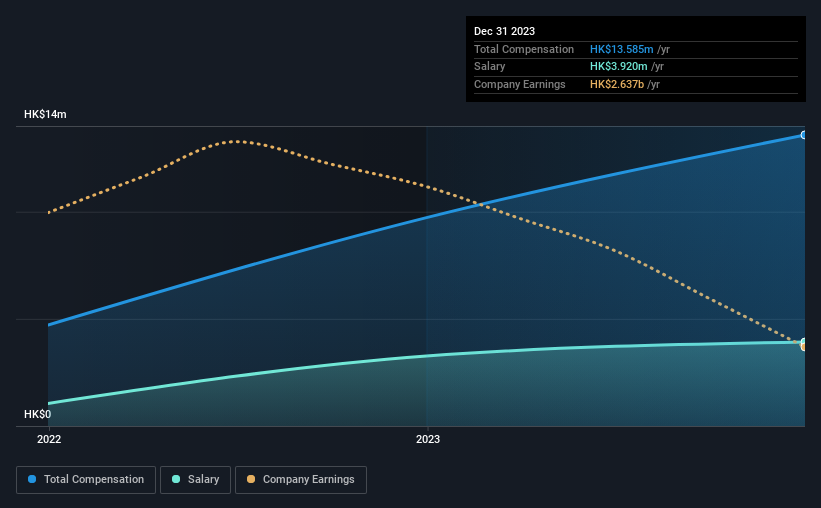

At the time of writing, our data shows that Swire Properties Limited has a market capitalization of HK$95b, and reported total annual CEO compensation of HK$14m for the year to December 2023. That's a notable increase of 40% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at HK$3.9m.

In comparison with other companies in the Hong Kong Real Estate industry with market capitalizations over HK$63b, the reported median total CEO compensation was HK$14m. So it looks like Swire Properties compensates Tim Blackburn in line with the median for the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$3.9m | HK$3.3m | 29% |

| Other | HK$9.7m | HK$6.5m | 71% |

| Total Compensation | HK$14m | HK$9.7m | 100% |

Talking in terms of the industry, salary represented approximately 75% of total compensation out of all the companies we analyzed, while other remuneration made up 25% of the pie. In Swire Properties' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Swire Properties Limited's Growth

Over the last three years, Swire Properties Limited has shrunk its earnings per share by 14% per year. In the last year, its revenue is up 4.9%.

The decline in EPS is a bit concerning. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Swire Properties Limited Been A Good Investment?

Since shareholders would have lost about 16% over three years, some Swire Properties Limited investors would surely be feeling negative emotions. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 3 warning signs for Swire Properties (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1972

Swire Properties

Develops, owns, and operates mixed-use, primarily commercial properties in Hong Kong, Mainland China, and the United States.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Community Narratives