Advertisement

- Hong Kong

- /

- Paper and Forestry Products

- /

- SEHK:2314

Lee and Man Paper Manufacturing (HKG:2314) Is Reducing Its Dividend To HK$0.11

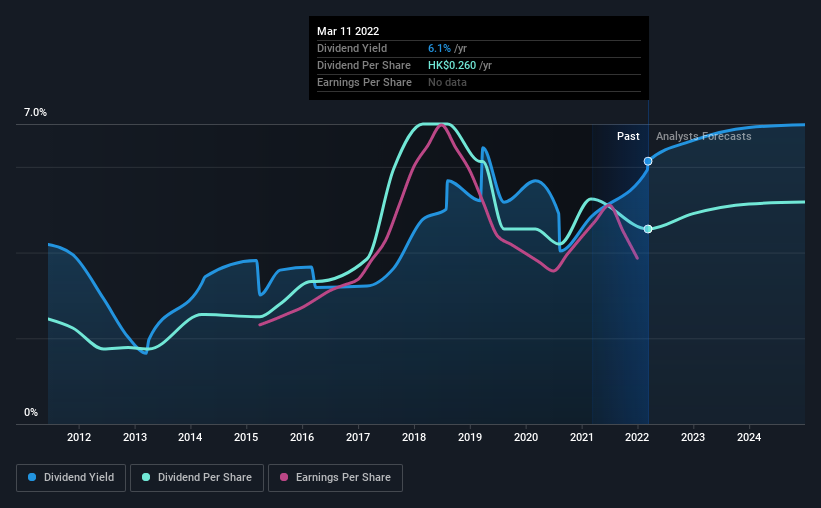

Lee and Man Paper Manufacturing Limited's (HKG:2314) dividend is being reduced to HK$0.11 on the 2nd of June. The dividend yield of 6.1% is still a nice boost to shareholder returns, despite the cut.

See our latest analysis for Lee and Man Paper Manufacturing

Lee and Man Paper Manufacturing's Earnings Easily Cover the Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Lee and Man Paper Manufacturing is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Looking forward, earnings per share is forecast to rise by 5.2% over the next year. If the dividend continues on this path, the payout ratio could be 36% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The first annual payment during the last 10 years was HK$0.14 in 2012, and the most recent fiscal year payment was HK$0.26. This works out to be a compound annual growth rate (CAGR) of approximately 6.4% a year over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

Dividend Growth May Be Hard To Achieve

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Earnings per share has been crawling upwards at 2.9% per year. If Lee and Man Paper Manufacturing is struggling to find viable investments, it always has the option to increase its payout ratio to pay more to shareholders.

Our Thoughts On Lee and Man Paper Manufacturing's Dividend

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. While Lee and Man Paper Manufacturing is earning enough to cover the payments, the cash flows are lacking. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 2 warning signs for Lee and Man Paper Manufacturing that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2314

Lee & Man Paper Manufacturing

Engages in the manufacture and trading of packaging papers, pulps, and tissue papers in the People’s Republic of China, Vietnam, Malaysia, Macau, and Hong Kong.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor