- Hong Kong

- /

- Trade Distributors

- /

- SEHK:2302

We Like These Underlying Return On Capital Trends At CNNC International (HKG:2302)

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Speaking of which, we noticed some great changes in CNNC International's (HKG:2302) returns on capital, so let's have a look.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on CNNC International is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.12 = HK$70m ÷ (HK$647m - HK$73m) (Based on the trailing twelve months to December 2022).

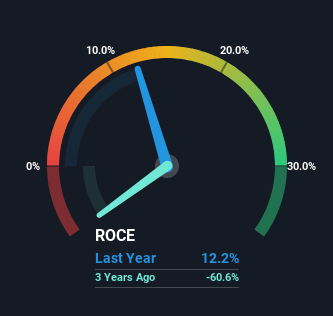

Thus, CNNC International has an ROCE of 12%. On its own, that's a standard return, however it's much better than the 4.4% generated by the Trade Distributors industry.

View our latest analysis for CNNC International

Historical performance is a great place to start when researching a stock so above you can see the gauge for CNNC International's ROCE against it's prior returns. If you're interested in investigating CNNC International's past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

Shareholders will be relieved that CNNC International has broken into profitability. While the business was unprofitable in the past, it's now turned things around and is earning 12% on its capital. Interestingly, the capital employed by the business has remained relatively flat, so these higher returns are either from prior investments paying off or increased efficiencies. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. So if you're looking for high growth, you'll want to see a business's capital employed also increasing.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 11%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. So shareholders would be pleased that the growth in returns has mostly come from underlying business performance.

The Key Takeaway

As discussed above, CNNC International appears to be getting more proficient at generating returns since capital employed has remained flat but earnings (before interest and tax) are up. Given the stock has declined 56% in the last five years, this could be a good investment if the valuation and other metrics are also appealing. With that in mind, we believe the promising trends warrant this stock for further investigation.

CNNC International does have some risks though, and we've spotted 1 warning sign for CNNC International that you might be interested in.

While CNNC International may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2302

CNNC International

An investment holding company, engages in the exploration, sale, and trading of uranium in Mainland China, Hong Kong, the United Kingdom, the United States, Japan, Canada, the Czech Republic, and Mongolia.

Proven track record with mediocre balance sheet.

Market Insights

Community Narratives