Advertisement

- United Kingdom

- /

- Software

- /

- LSE:BYIT

Calculating The Fair Value Of Bytes Technology Group plc (LON:BYIT)

Key Insights

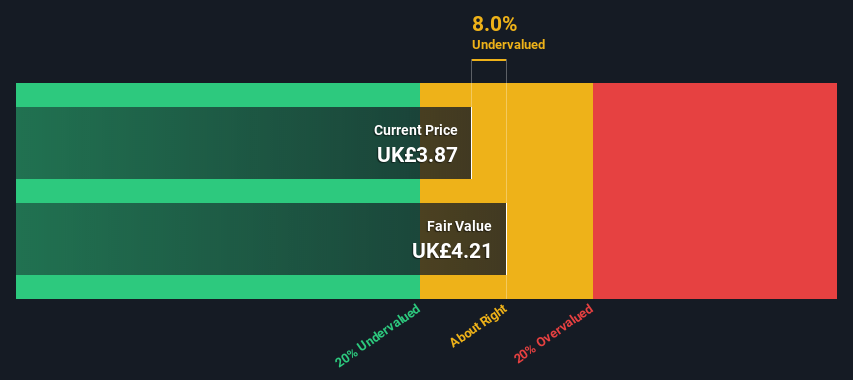

- Bytes Technology Group's estimated fair value is UK£4.2 based on 2 Stage Free Cash Flow to Equity

- Current share price of UK£3.9 suggests Bytes Technology Group is trading close to its fair value

- Analyst price target for BYIT is UK£5.33 which is 27% above our fair value estimate

In this article we are going to estimate the intrinsic value of Bytes Technology Group plc (LON:BYIT) by estimating the company's future cash flows and discounting them to their present value. We will use the Discounted Cash Flow (DCF) model on this occasion. It may sound complicated, but actually it is quite simple!

Companies can be valued in a lot of ways, so we would point out that a DCF is not perfect for every situation. Anyone interested in learning a bit more about intrinsic value should have a read of the Simply Wall St analysis model.

See our latest analysis for Bytes Technology Group

Step By Step Through The Calculation

We are going to use a two-stage DCF model, which, as the name states, takes into account two stages of growth. The first stage is generally a higher growth period which levels off heading towards the terminal value, captured in the second 'steady growth' period. To start off with, we need to estimate the next ten years of cash flows. Where possible we use analyst estimates, but when these aren't available we extrapolate the previous free cash flow (FCF) from the last estimate or reported value. We assume companies with shrinking free cash flow will slow their rate of shrinkage, and that companies with growing free cash flow will see their growth rate slow, over this period. We do this to reflect that growth tends to slow more in the early years than it does in later years.

A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, so we discount the value of these future cash flows to their estimated value in today's dollars:

10-year free cash flow (FCF) forecast

| 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | |

| Levered FCF (£, Millions) | UK£25.8m | UK£49.2m | UK£57.8m | UK£64.0m | UK£69.0m | UK£73.0m | UK£76.1m | UK£78.6m | UK£80.7m | UK£82.4m |

| Growth Rate Estimate Source | Analyst x2 | Analyst x3 | Analyst x3 | Est @ 10.69% | Est @ 7.78% | Est @ 5.74% | Est @ 4.32% | Est @ 3.32% | Est @ 2.62% | Est @ 2.13% |

| Present Value (£, Millions) Discounted @ 7.7% | UK£23.9 | UK£42.4 | UK£46.2 | UK£47.5 | UK£47.5 | UK£46.6 | UK£45.2 | UK£43.3 | UK£41.2 | UK£39.1 |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = UK£423m

We now need to calculate the Terminal Value, which accounts for all the future cash flows after this ten year period. The Gordon Growth formula is used to calculate Terminal Value at a future annual growth rate equal to the 5-year average of the 10-year government bond yield of 1.0%. We discount the terminal cash flows to today's value at a cost of equity of 7.7%.

Terminal Value (TV)= FCF2032 × (1 + g) ÷ (r – g) = UK£82m× (1 + 1.0%) ÷ (7.7%– 1.0%) = UK£1.2b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= UK£1.2b÷ ( 1 + 7.7%)10= UK£584m

The total value, or equity value, is then the sum of the present value of the future cash flows, which in this case is UK£1.0b. The last step is to then divide the equity value by the number of shares outstanding. Relative to the current share price of UK£3.9, the company appears about fair value at a 8.0% discount to where the stock price trades currently. Valuations are imprecise instruments though, rather like a telescope - move a few degrees and end up in a different galaxy. Do keep this in mind.

The Assumptions

Now the most important inputs to a discounted cash flow are the discount rate, and of course, the actual cash flows. If you don't agree with these result, have a go at the calculation yourself and play with the assumptions. The DCF also does not consider the possible cyclicality of an industry, or a company's future capital requirements, so it does not give a full picture of a company's potential performance. Given that we are looking at Bytes Technology Group as potential shareholders, the cost of equity is used as the discount rate, rather than the cost of capital (or weighted average cost of capital, WACC) which accounts for debt. In this calculation we've used 7.7%, which is based on a levered beta of 0.986. Beta is a measure of a stock's volatility, compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, which is a reasonable range for a stable business.

SWOT Analysis for Bytes Technology Group

Strength

- Earnings growth over the past year exceeded the industry.

- Currently debt free.

- Dividends are covered by earnings and cash flows.

Weakness

- Dividend is low compared to the top 25% of dividend payers in the Software market.

Opportunity

- Annual earnings are forecast to grow faster than the British market.

- Good value based on P/E ratio and estimated fair value.

- Significant insider buying over the past 3 months.

Threat

- Revenue is forecast to grow slower than 20% per year.

Looking Ahead:

Whilst important, the DCF calculation ideally won't be the sole piece of analysis you scrutinize for a company. The DCF model is not a perfect stock valuation tool. Preferably you'd apply different cases and assumptions and see how they would impact the company's valuation. For instance, if the terminal value growth rate is adjusted slightly, it can dramatically alter the overall result. For Bytes Technology Group, we've compiled three additional items you should further examine:

- Financial Health: Does BYIT have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Management:Have insiders been ramping up their shares to take advantage of the market's sentiment for BYIT's future outlook? Check out our management and board analysis with insights on CEO compensation and governance factors.

- Other Solid Businesses: Low debt, high returns on equity and good past performance are fundamental to a strong business. Why not explore our interactive list of stocks with solid business fundamentals to see if there are other companies you may not have considered!

PS. The Simply Wall St app conducts a discounted cash flow valuation for every stock on the LSE every day. If you want to find the calculation for other stocks just search here.

Valuation is complex, but we're here to simplify it.

Discover if Bytes Technology Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BYIT

Bytes Technology Group

Offers software, security, AI, and cloud services in the United Kingdom, Europe, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2550.7% undervalued

117 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4846.5% undervalued

220 followersusers have followed this narrative

9 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43043.8% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9954.9% undervalued

30 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

TR

TripleS on Vistance Networks ·

VISN trades at $11.83 with roughly $1.88 billion of cash and zero debt after closing the sale of its Ruckus division to Belden on July 1

Fair Value:US$1626.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Vertiv Holdings Co ·

Everyone's Favorite Stock Just Fell 17% in a Day. It Still Isn't Cheap.

Fair Value:US$2136.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ON

Ontological on Robo.ai ·

Robo.ai and Abu Dhabi Enterprise Jointly Establish AI Industrial Group Alif Holding to Serve Infrastructure, Government and Industrial Secto

Fair Value:US$10.2872.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28030.3% undervalued

217 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.917.4% overvalued

98 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6511.3% undervalued

75 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

1

|0

BL

Blegells on Terra Balcanica Resources ·

⏫42X THE AVERAGE DAILY TRADING VOLUME TODAY, JULY 28 🐂🐂🐂 FORTY-TWO!

1

|0