- United Kingdom

- /

- Software

- /

- AIM:KAPE

Kape Technologies Plc Just Missed EPS By 24%: Here's What Analysts Think Will Happen Next

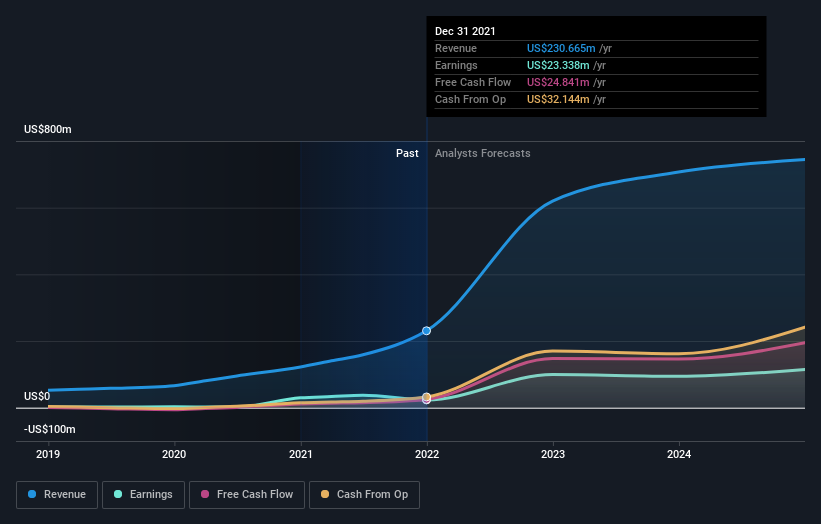

Investors in Kape Technologies Plc (LON:KAPE) had a good week, as its shares rose 3.8% to close at UK£4.00 following the release of its full-year results. Results overall were not great, with earnings of US$0.094 per share falling drastically short of analyst expectations. Meanwhile revenues hit US$231m and were slightly better than forecasts. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for Kape Technologies

Following the latest results, Kape Technologies' five analysts are now forecasting revenues of US$619.7m in 2022. This would be a substantial 169% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to leap 297% to US$0.26. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$620.0m and earnings per share (EPS) of US$0.27 in 2022. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

It might be a surprise to learn that the consensus price target was broadly unchanged at UK£4.99, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Kape Technologies at UK£5.73 per share, while the most bearish prices it at UK£4.24. This is a very narrow spread of estimates, implying either that Kape Technologies is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Kape Technologies' rate of growth is expected to accelerate meaningfully, with the forecast 169% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 31% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 13% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Kape Technologies to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Kape Technologies. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Kape Technologies going out to 2024, and you can see them free on our platform here..

Before you take the next step you should know about the 3 warning signs for Kape Technologies (1 is potentially serious!) that we have uncovered.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kape Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:KAPE

Kape Technologies

Kape Technologies PLC, together with its subsidiaries, develops and distributes digital products in the online security space.

Undervalued with solid track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion