- United Kingdom

- /

- Retail Distributors

- /

- LSE:INCH

With EPS Growth And More, Inchcape (LON:INCH) Makes An Interesting Case

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Inchcape (LON:INCH). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

Check out our latest analysis for Inchcape

Inchcape's Improving Profits

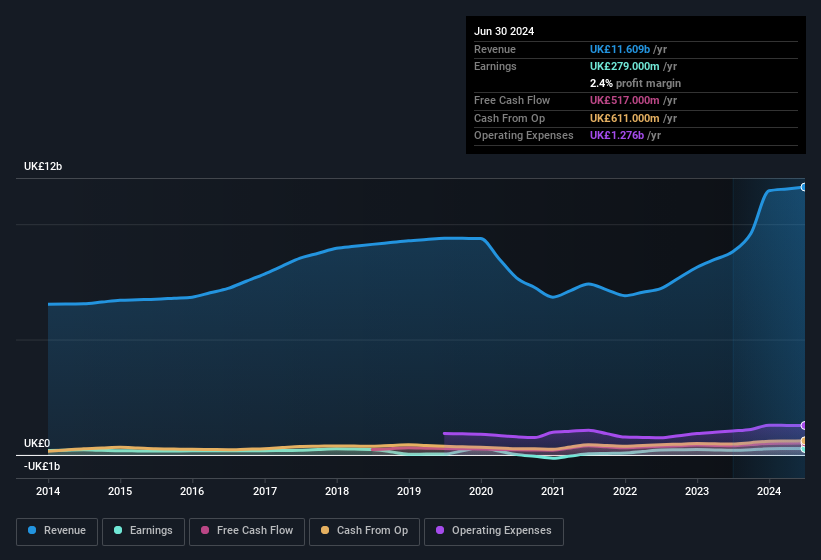

Inchcape has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. As a result, we'll zoom in on growth over the last year, instead. Inchcape's EPS shot up from UK£0.51 to UK£0.71; a result that's bound to keep shareholders happy. That's a fantastic gain of 39%.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. EBIT margins for Inchcape remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 32% to UK£12b. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

Fortunately, we've got access to analyst forecasts of Inchcape's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Inchcape Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Shareholders in Inchcape will be more than happy to see insiders committing themselves to the company, spending UK£375k on shares in just twelve months. When you contrast that with the complete lack of sales, it's easy for shareholders to be brimming with joyful expectancy. We also note that it was the Independent Chairman of the Board, Jerry Buhlmann, who made the biggest single acquisition, paying UK£100k for shares at about UK£6.41 each.

On top of the insider buying, it's good to see that Inchcape insiders have a valuable investment in the business. Holding UK£59m worth of stock in the company is no laughing matter and insiders will be committed in delivering the best outcomes for shareholders. This should keep them focused on creating long term value for shareholders.

Does Inchcape Deserve A Spot On Your Watchlist?

If you believe that share price follows earnings per share you should definitely be delving further into Inchcape's strong EPS growth. Not only that, but we can see that insiders both own a lot of, and are buying more shares in the company. Astute investors will want to keep this stock on watch. We don't want to rain on the parade too much, but we did also find 2 warning signs for Inchcape that you need to be mindful of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Inchcape, you'll probably love this curated collection of companies in GB that have an attractive valuation alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:INCH

Very undervalued with solid track record and pays a dividend.