Advertisement

- United Kingdom

- /

- Capital Markets

- /

- LSE:FSG

UK Penny Stocks With Potential: 3 Picks Under £600M Market Cap

Simply Wall St

Reviewed by Simply Wall St

The London markets have recently faced challenges, with the FTSE 100 and FTSE 250 indices closing lower amid weak trade data from China, highlighting the interconnectedness of global economies. Despite these broader market pressures, there remains a niche area of interest for investors: penny stocks. Although once a buzzword, penny stocks continue to offer growth opportunities in smaller or newer companies with strong financial health. In this article, we'll explore several UK penny stocks that stand out for their balance sheet strength and potential for long-term success.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Rewards & Risks |

| DSW Capital (AIM:DSW) | £0.50 | £12.57M | ✅ 3 ⚠️ 4 View Analysis > |

| Foresight Group Holdings (LSE:FSG) | £4.695 | £535.43M | ✅ 4 ⚠️ 0 View Analysis > |

| Warpaint London (AIM:W7L) | £2.05 | £165.61M | ✅ 4 ⚠️ 2 View Analysis > |

| Ingenta (AIM:ING) | £0.98 | £14.8M | ✅ 2 ⚠️ 3 View Analysis > |

| System1 Group (AIM:SYS1) | £2.13 | £27.03M | ✅ 3 ⚠️ 3 View Analysis > |

| Integrated Diagnostics Holdings (LSE:IDHC) | $0.655 | $380.77M | ✅ 4 ⚠️ 2 View Analysis > |

| RWS Holdings (AIM:RWS) | £0.775 | £286.58M | ✅ 5 ⚠️ 2 View Analysis > |

| Spectra Systems (AIM:SPSY) | £1.345 | £64.96M | ✅ 3 ⚠️ 3 View Analysis > |

| M.T.I Wireless Edge (AIM:MWE) | £0.49 | £42.24M | ✅ 3 ⚠️ 3 View Analysis > |

| Begbies Traynor Group (AIM:BEG) | £1.125 | £179.55M | ✅ 4 ⚠️ 2 View Analysis > |

Click here to see the full list of 302 stocks from our UK Penny Stocks screener.

Let's review some notable picks from our screened stocks.

Card Factory (LSE:CARD)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Card Factory plc is a specialist retailer of cards, gifts, and celebration essentials operating in the United Kingdom, South Africa, Republic of Ireland, the United States, and internationally with a market cap of £345.44 million.

Operations: The company's revenue is primarily generated from its Cardfactory Stores segment, which accounts for £513.2 million, supplemented by £32.1 million from Partnerships.

Market Cap: £345.44M

Card Factory plc, with a market cap of £345.44 million, has demonstrated financial resilience despite facing challenges. Its earnings grew by 5.1% last year, surpassing the Specialty Retail industry's decline, and its debt is well covered by operating cash flow. The company trades at a significant discount to its estimated fair value and has not diluted shareholders recently. However, net profit margins have slightly declined compared to the previous year. Recent developments include a share buyback program and an interim dividend increase of 4.9%, reflecting confidence in future performance amidst fluctuating earnings results.

- Take a closer look at Card Factory's potential here in our financial health report.

- Assess Card Factory's future earnings estimates with our detailed growth reports.

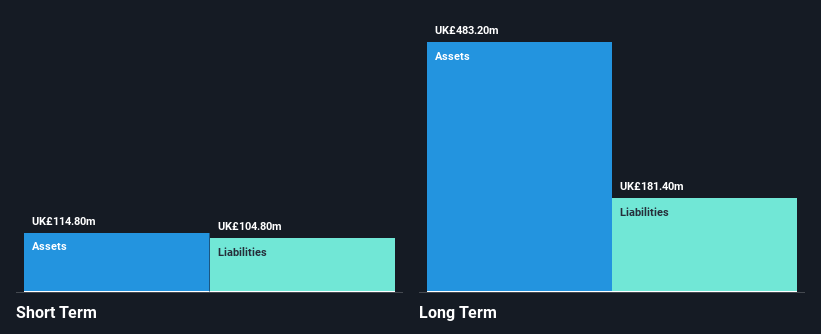

Foresight Group Holdings (LSE:FSG)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Foresight Group Holdings Limited is an infrastructure and private equity manager operating in the United Kingdom, Italy, Luxembourg, Ireland, Spain, and Australia with a market cap of £535.43 million.

Operations: The company's revenue is derived from three segments: Infrastructure (£95.89 million), Private Equity (£50.52 million), and Foresight Capital Management (£7.58 million).

Market Cap: £535.43M

Foresight Group Holdings, with a market cap of £535.43 million, exhibits strong financial health and growth potential. Its earnings have grown significantly by 25.5% annually over the past five years and surpassed industry growth last year at 25.8%. The company maintains high-quality earnings, with short-term assets covering both short- and long-term liabilities comfortably. Foresight's debt is well-covered by operating cash flow, while its return on equity stands at a robust 39%. Trading slightly below fair value estimates, it has not diluted shareholders recently and benefits from an experienced board of directors with stable weekly volatility.

- Unlock comprehensive insights into our analysis of Foresight Group Holdings stock in this financial health report.

- Evaluate Foresight Group Holdings' prospects by accessing our earnings growth report.

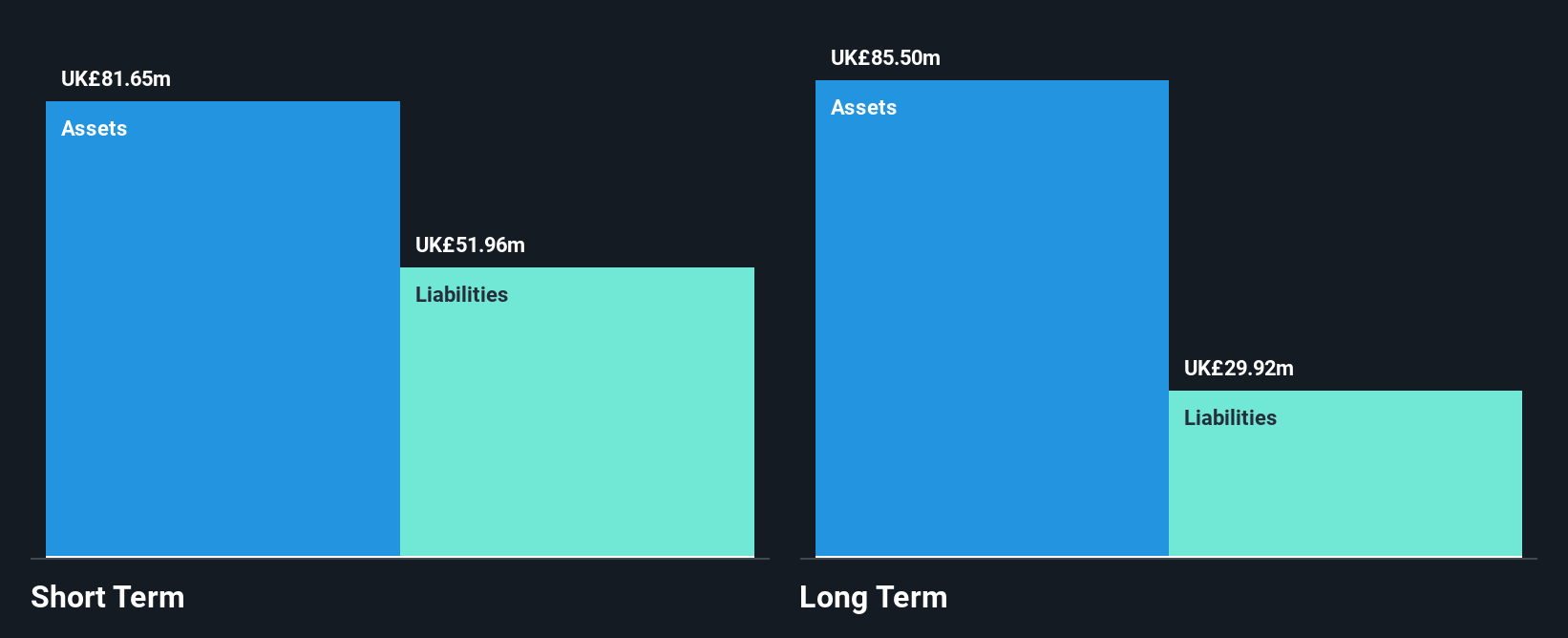

LSL Property Services (LSE:LSL)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: LSL Property Services plc operates in the United Kingdom, offering business-to-business services to mortgage intermediaries and estate agent franchisees, as well as valuation services to lenders, with a market cap of £250.89 million.

Operations: The company's revenue is primarily derived from three segments: Financial Services (£48.33 million), Surveying and Valuation (£102.08 million), and Estate Agency excluding Financial Services (£27.04 million).

Market Cap: £250.89M

LSL Property Services, with a market cap of £250.89 million, demonstrates financial stability with short-term assets exceeding both short- and long-term liabilities. The company has seen earnings growth of 23.8% over the past year, surpassing industry averages, though its five-year earnings trend shows a decline. Recent executive changes include the appointment of David Tilak as CFO and Executive Board Director, bringing extensive strategic experience. Despite trading below fair value estimates and maintaining stable weekly volatility, LSL's dividend is not well-covered by free cash flow. Shareholder dilution has been minimal amidst ongoing share buybacks.

- Click to explore a detailed breakdown of our findings in LSL Property Services' financial health report.

- Review our growth performance report to gain insights into LSL Property Services' future.

Seize The Opportunity

- Unlock our comprehensive list of 302 UK Penny Stocks by clicking here.

- Seeking Other Investments? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:FSG

Foresight Group Holdings

Operates as an infrastructure and private equity manager in the United Kingdom, Italy, Luxembourg, Ireland, Spain, and Australia.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

95 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative