Advertisement

- United Kingdom

- /

- Real Estate

- /

- LSE:IWG

3 UK Growth Stocks With High Insider Ownership And 95% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

Share

The United Kingdom's FTSE 100 index has recently faced challenges, closing lower due to weak trade data from China, which has impacted companies closely tied to its economic performance. In such volatile market conditions, growth stocks with high insider ownership can be appealing as they may indicate confidence from those within the company and potential resilience in earnings growth.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 62.5% |

| Foresight Group Holdings (LSE:FSG) | 34.8% | 27% |

| Helios Underwriting (AIM:HUW) | 23.9% | 23.1% |

| Facilities by ADF (AIM:ADF) | 13.2% | 161.5% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.7% | 21.1% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Judges Scientific (AIM:JDG) | 10.7% | 27.9% |

| Audioboom Group (AIM:BOOM) | 27.8% | 175% |

| Getech Group (AIM:GTC) | 11.8% | 114.5% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 116.2% |

Let's uncover some gems from our specialized screener.

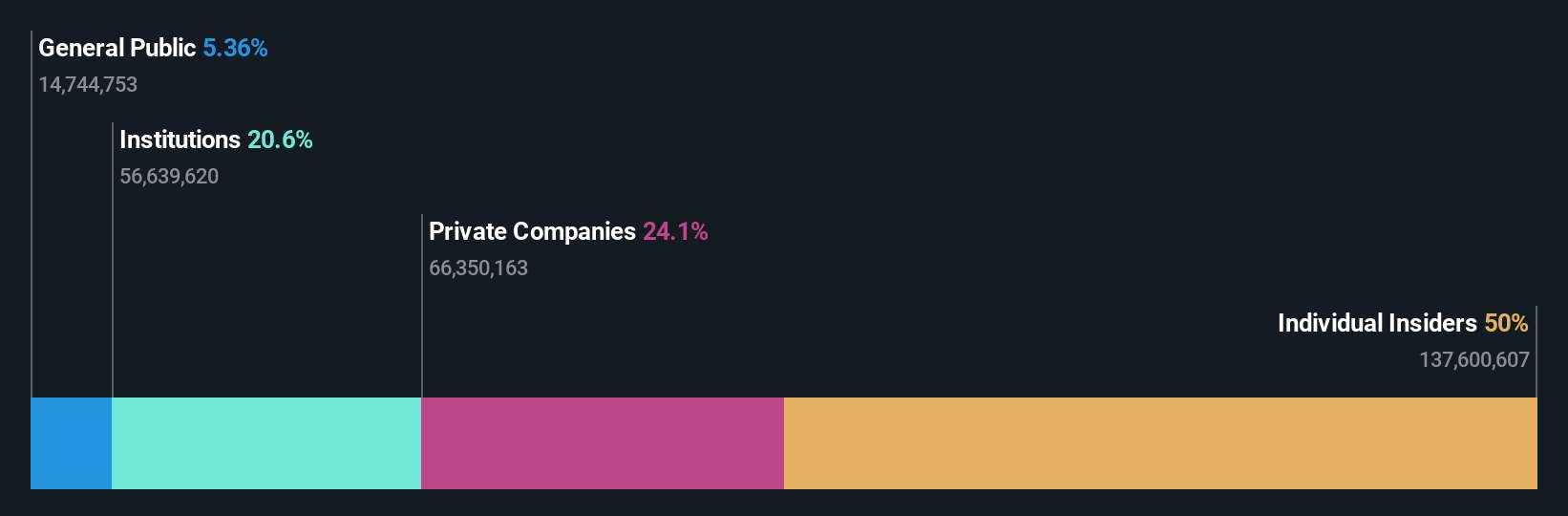

Franchise Brands (AIM:FRAN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Franchise Brands plc operates in franchising and related activities across the United Kingdom, North America, and Europe, with a market cap of £274.74 million.

Operations: Franchise Brands plc generates revenue through its subsidiaries by engaging in franchising and related activities across the United Kingdom, North America, and Europe.

Insider Ownership: 22.4%

Earnings Growth Forecast: 29.4% p.a.

Franchise Brands has demonstrated robust growth, with earnings increasing significantly by 139.8% over the past year and a forecasted annual profit growth of 29.4%, outpacing the UK market average. Recent insider activities reveal substantial buying, indicating confidence in its future prospects. The company reported strong financials for 2024, with sales reaching £139.21 million and net income rising to £7.28 million, alongside strategic leadership changes to support its "One Franchise Brands" initiative aimed at operational efficiency and debt reduction.

- Get an in-depth perspective on Franchise Brands' performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that Franchise Brands is trading beyond its estimated value.

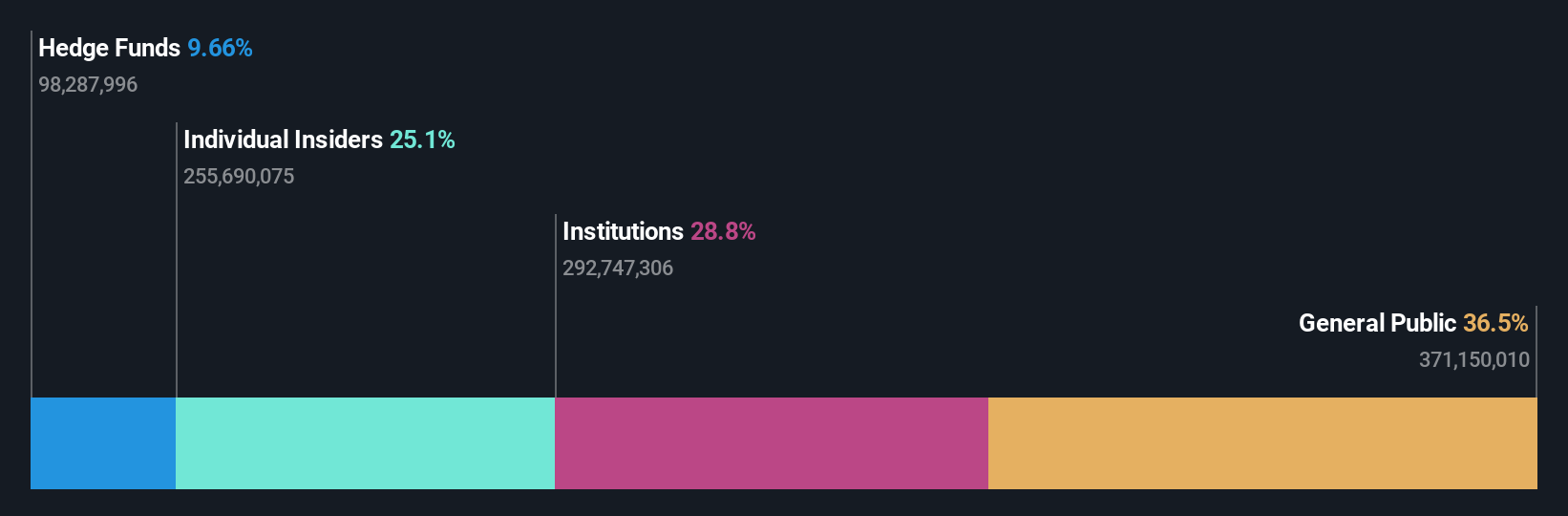

Genel Energy (LSE:GENL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Genel Energy plc is an independent oil and gas exploration and production company with a market cap of £197.42 million.

Operations: The company's revenue segment consists of $74.70 million from production activities.

Insider Ownership: 25.9%

Earnings Growth Forecast: 95.7% p.a.

Genel Energy is poised for growth, with revenue expected to increase 12% annually, surpassing the UK market average. Despite a volatile share price and current unprofitability, the company aims to become profitable within three years. Recent strategic moves include a $100 million bond issuance and entering Oman's Block 54 exploration project with OQEP. However, financial challenges persist as evidenced by a net loss of $76.9 million in 2024 amid declining sales figures.

- Click to explore a detailed breakdown of our findings in Genel Energy's earnings growth report.

- The valuation report we've compiled suggests that Genel Energy's current price could be inflated.

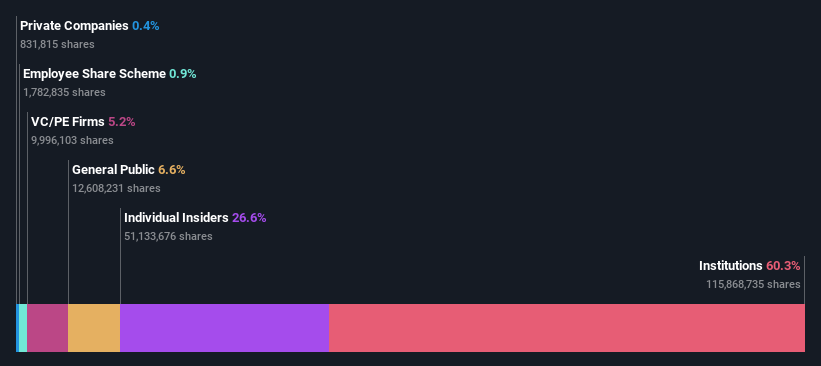

International Workplace Group (LSE:IWG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: International Workplace Group plc, along with its subsidiaries, offers workspace solutions across the Americas, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of £1.89 billion.

Operations: The company generates revenue from various segments, including $1.29 billion from the Americas, $334 million from the Asia Pacific, $389 million from Digital and Professional Services, and $1.67 billion from Europe, the Middle East, and Africa (EMEA).

Insider Ownership: 25.2%

Earnings Growth Forecast: 49.1% p.a.

International Workplace Group has become profitable, reporting a net income of US$20 million for 2024, contrasting with the previous year's loss. Earnings are projected to grow significantly by 49.1% annually, outpacing the UK market. However, revenue growth is modest at 4.8% per year. The company announced a US$50 million share buyback to reduce share capital, indicating confidence in its financial health despite concerns over interest coverage and large one-off items affecting results.

- Unlock comprehensive insights into our analysis of International Workplace Group stock in this growth report.

- According our valuation report, there's an indication that International Workplace Group's share price might be on the expensive side.

Seize The Opportunity

- Delve into our full catalog of 67 Fast Growing UK Companies With High Insider Ownership here.

- Ready For A Different Approach? Uncover 14 companies that survived and thrived after COVID and have the right ingredients to survive Trump's tariffs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:IWG

International Workplace Group

Provides workspace solutions in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

High growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor