Advertisement

- United Kingdom

- /

- Specialty Stores

- /

- LSE:AO.

UK Exchange: Promising Penny Stocks To Watch In January 2025

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, impacting companies heavily reliant on Chinese demand. Despite these broader market pressures, investors continue to seek opportunities in lesser-known segments like penny stocks. Although the term "penny stocks" might seem outdated, it still refers to smaller or newer companies that can offer significant growth potential when backed by solid financials.

Top 10 Penny Stocks In The United Kingdom

| Name | Share Price | Market Cap | Financial Health Rating |

| ME Group International (LSE:MEGP) | £2.07 | £780M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.934 | £148.85M | ★★★★★★ |

| Foresight Group Holdings (LSE:FSG) | £3.71 | £432.46M | ★★★★★★ |

| Stelrad Group (LSE:SRAD) | £1.42 | £180.84M | ★★★★★☆ |

| Next 15 Group (AIM:NFG) | £3.45 | £343.12M | ★★★★☆☆ |

| Secure Trust Bank (LSE:STB) | £4.48 | £85.44M | ★★★★☆☆ |

| Ultimate Products (LSE:ULTP) | £1.065 | £90.69M | ★★★★★★ |

| Tristel (AIM:TSTL) | £3.825 | £182.42M | ★★★★★★ |

| Luceco (LSE:LUCE) | £1.384 | £213.45M | ★★★★★☆ |

| Helios Underwriting (AIM:HUW) | £2.08 | £148.39M | ★★★★★☆ |

Click here to see the full list of 445 stocks from our UK Penny Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

Gear4music (Holdings) (AIM:G4M)

Simply Wall St Financial Health Rating: ★★★★★☆

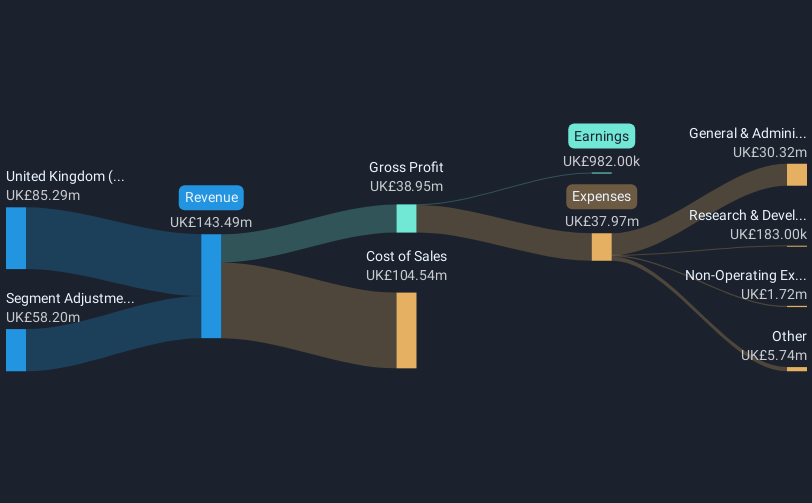

Overview: Gear4music (Holdings) plc is a retailer of musical instruments and equipment operating in the United Kingdom, Europe, and internationally with a market cap of £31.99 million.

Operations: The company's revenue segment consists of £143.49 million from the sale of musical instruments and equipment.

Market Cap: £31.99M

Gear4music (Holdings) plc, with a market cap of £31.99 million, has recently turned profitable, although its earnings have declined significantly over the past five years. The company reported half-year sales of £61.74 million and a reduced net loss compared to the previous year. Despite having satisfactory debt levels and short-term assets exceeding liabilities, its interest coverage is weak at 1.6 times EBIT, and return on equity remains low at 2.6%. A large one-off gain impacted recent financial results, while revenue is forecasted to grow modestly by 6.48% per year moving forward.

- Take a closer look at Gear4music (Holdings)'s potential here in our financial health report.

- Learn about Gear4music (Holdings)'s future growth trajectory here.

Zinnwald Lithium (AIM:ZNWD)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Zinnwald Lithium Plc is a mineral exploration and development company operating in the United Kingdom and Germany, with a market cap of £36.78 million.

Operations: Currently, the company does not report any revenue segments.

Market Cap: £36.78M

Zinnwald Lithium Plc, with a market cap of £36.78 million, is currently pre-revenue and unprofitable, making it challenging to assess its financial health solely on earnings. The company is debt-free and has not diluted shareholders over the past year, which can be seen as positive aspects for investors concerned about equity value preservation. However, Zinnwald faces a cash runway of less than one year if current cash flow trends persist. Despite these challenges, the management team and board are experienced with average tenures of 3.4 and 6.6 years respectively, which may provide stability during growth phases.

- Unlock comprehensive insights into our analysis of Zinnwald Lithium stock in this financial health report.

- Evaluate Zinnwald Lithium's prospects by accessing our earnings growth report.

AO World (LSE:AO.)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: AO World plc, along with its subsidiaries, operates as an online retailer of domestic appliances and ancillary services in the United Kingdom and Germany, with a market capitalization of £560.20 million.

Operations: The company generates £1.07 billion in revenue from its online retailing of domestic appliances and ancillary services.

Market Cap: £560.2M

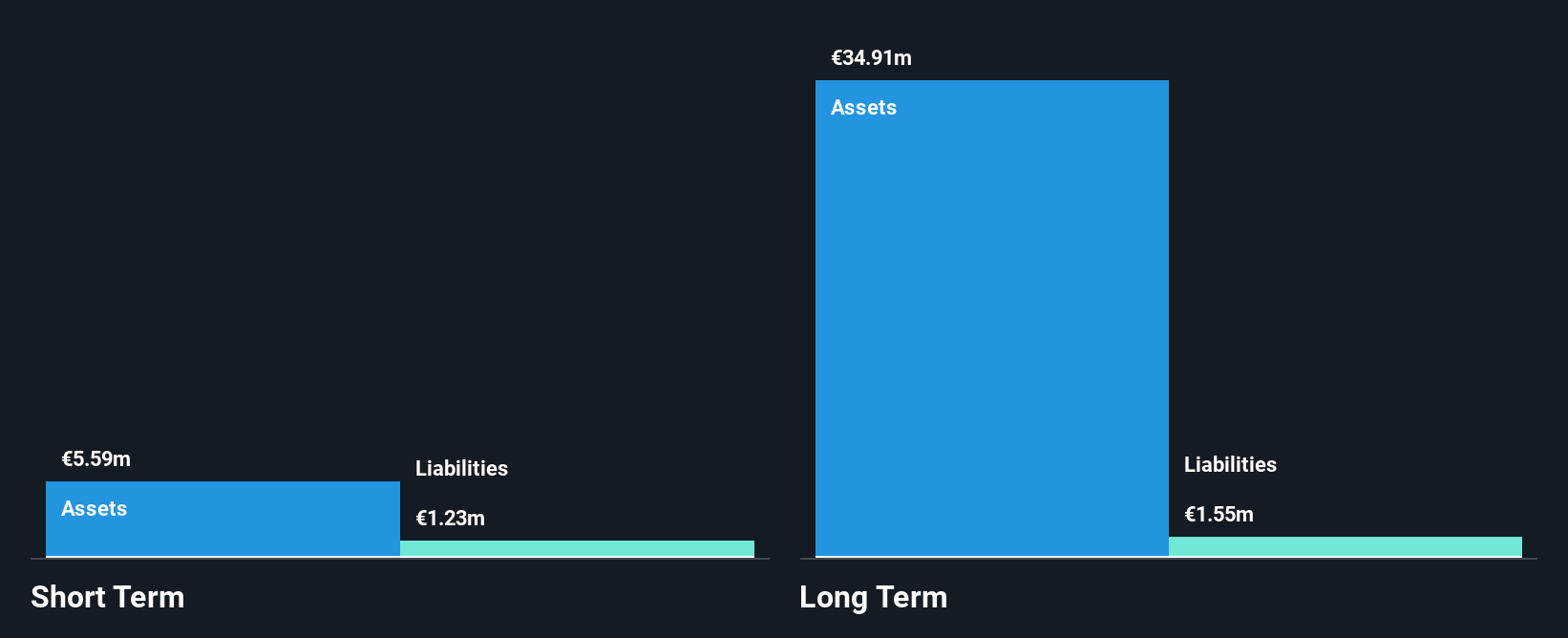

AO World plc, with a market cap of £560.20 million, has shown financial resilience despite recent challenges. The company's debt to equity ratio has significantly decreased over the past five years, and it maintains more cash than total debt, indicating strong fiscal management. Short-term assets exceed long-term liabilities; however, they fall short of covering all short-term liabilities. Recent earnings reports show improved sales and net income compared to last year, with a revised guidance projecting revenue growth exceeding 10% in B2C Retail for 2024. Despite these positives, AO's Return on Equity remains low at 18.6%.

- Click here and access our complete financial health analysis report to understand the dynamics of AO World.

- Examine AO World's earnings growth report to understand how analysts expect it to perform.

Turning Ideas Into Actions

- Unlock our comprehensive list of 445 UK Penny Stocks by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:AO.

AO World

Engages in the online retailing of domestic appliances and ancillary services in the United Kingdom and Germany.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor