Advertisement

Wendy Lawrence became the CEO of Totally plc (LON:TLY) in 2013, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

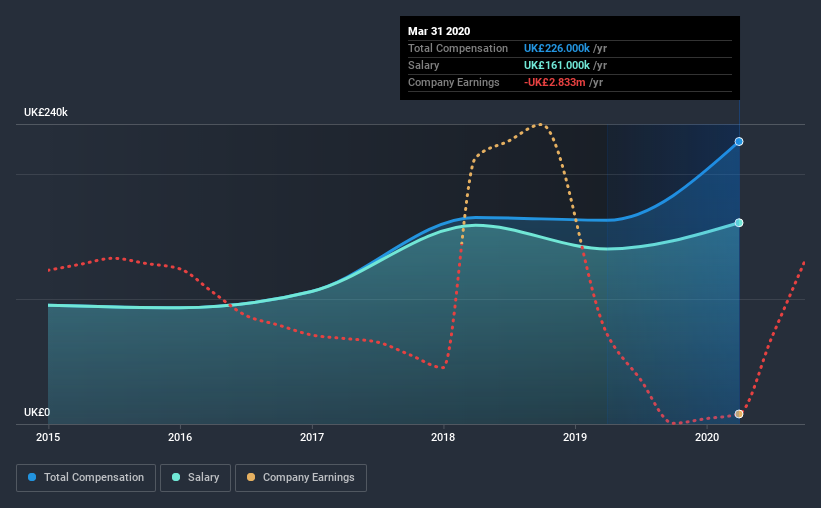

Check out our latest analysis for Totally

Comparing Totally plc's CEO Compensation With the industry

Our data indicates that Totally plc has a market capitalization of UK£61m, and total annual CEO compensation was reported as UK£226k for the year to March 2020. Notably, that's an increase of 39% over the year before. In particular, the salary of UK£161.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the industry with market capitalizations below UK£147m, we found that the median total CEO compensation was UK£190k. From this we gather that Wendy Lawrence is paid around the median for CEOs in the industry. Moreover, Wendy Lawrence also holds UK£43k worth of Totally stock directly under their own name.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | UK£161k | UK£140k | 71% |

| Other | UK£65k | UK£23k | 29% |

| Total Compensation | UK£226k | UK£163k | 100% |

Speaking on an industry level, nearly 74% of total compensation represents salary, while the remainder of 26% is other remuneration. Totally is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Totally plc's Growth Numbers

Over the last three years, Totally plc has shrunk its earnings per share by 34% per year. In the last year, its revenue is up 27%.

Investors would be a bit wary of companies that have lower EPS But on the other hand, revenue growth is strong, suggesting a brighter future. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Totally plc Been A Good Investment?

With a three year total loss of 13% for the shareholders, Totally plc would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

In Summary...

As we touched on above, Totally plc is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. However, revenues have increased over the past year, a positive sign for the company. In contrast, over the same time span, shareholder returns are negative. EPS is also not growing, undoubtedly leading to further headaches. Overall, we wouldn't say CEO is highly paid, but shareholders might not go for a raise before business metrics start to improve precipitously.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 4 warning signs for Totally you should be aware of, and 1 of them can't be ignored.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading Totally or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Totally might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:TLY

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor