- United Kingdom

- /

- Oil and Gas

- /

- LSE:BP.

BP p.l.c. Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

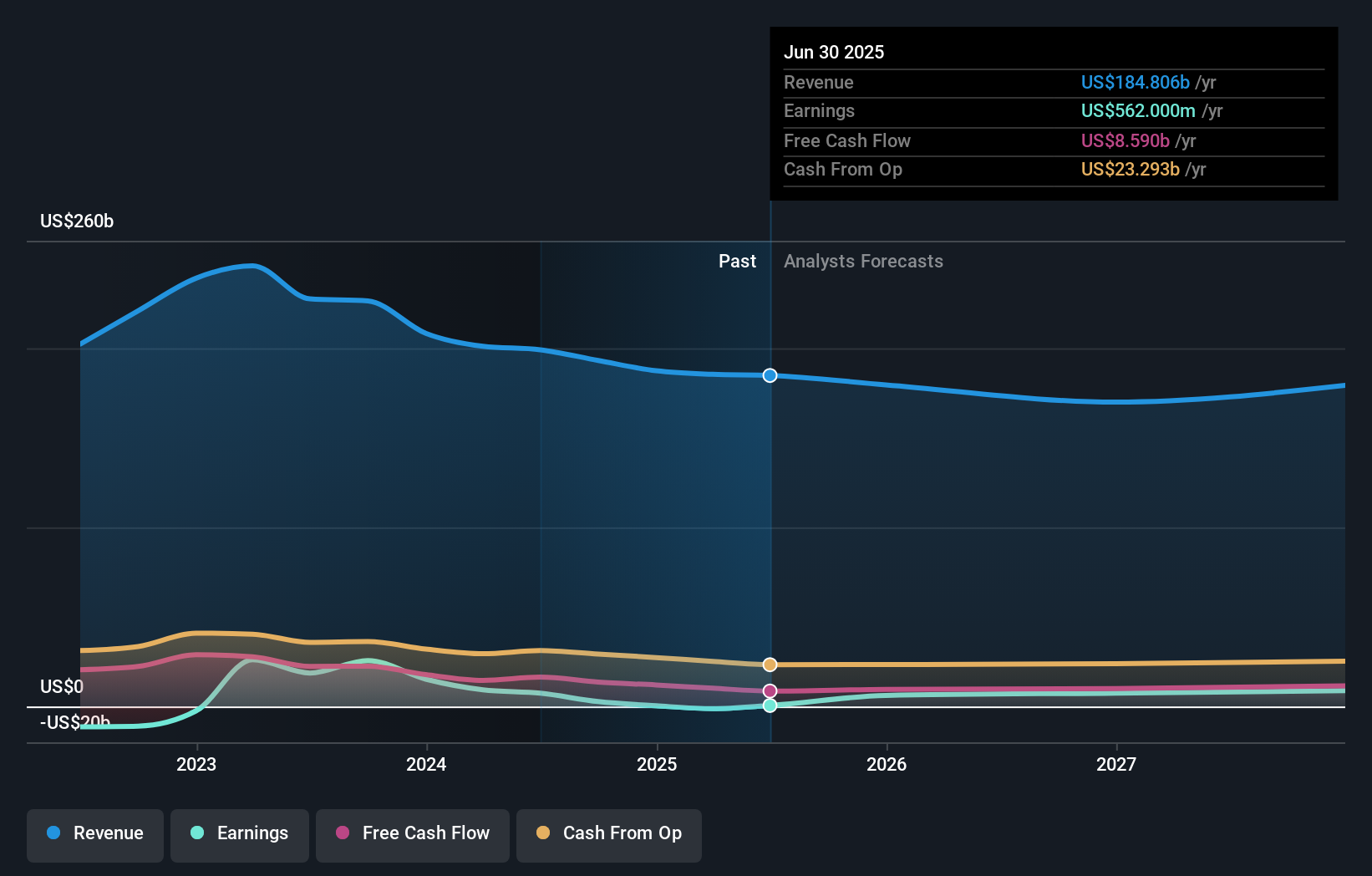

BP p.l.c. (LON:BP.) defied analyst predictions to release its second-quarter results, which were ahead of market expectations. It was a solid earnings report, with revenues and statutory earnings per share (EPS) both coming in strong. Revenues were 15% higher than the analysts had forecast, at US$47b, while EPS were US$0.10 beating analyst models by 22%. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Taking into account the latest results, the current consensus, from the 22 analysts covering BP, is for revenues of US$179.5b in 2025. This implies a perceptible 2.8% reduction in BP's revenue over the past 12 months. Per-share earnings are expected to soar 910% to US$0.37. Before this earnings report, the analysts had been forecasting revenues of US$178.3b and earnings per share (EPS) of US$0.41 in 2025. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a minor downgrade to their earnings per share forecasts.

See our latest analysis for BP

The consensus price target held steady at UK£4.28, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values BP at UK£5.23 per share, while the most bearish prices it at UK£3.51. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await BP shareholders.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the BP's past performance and to peers in the same industry. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 5.6% by the end of 2025. This indicates a significant reduction from annual growth of 7.7% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 13% annually for the foreseeable future. It's pretty clear that BP's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for BP. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that BP's revenue is expected to perform worse than the wider industry. The consensus price target held steady at UK£4.28, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on BP. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple BP analysts - going out to 2027, and you can see them free on our platform here.

Plus, you should also learn about the 4 warning signs we've spotted with BP .

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if BP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BP.

BP

An integrated energy company, engages in the oil and gas business worldwide.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)