Advertisement

- United Kingdom

- /

- Consumer Durables

- /

- LSE:BTRW

Barratt Developments (LON:BDEV) Has Announced That Its Dividend Will Be Reduced To £0.044

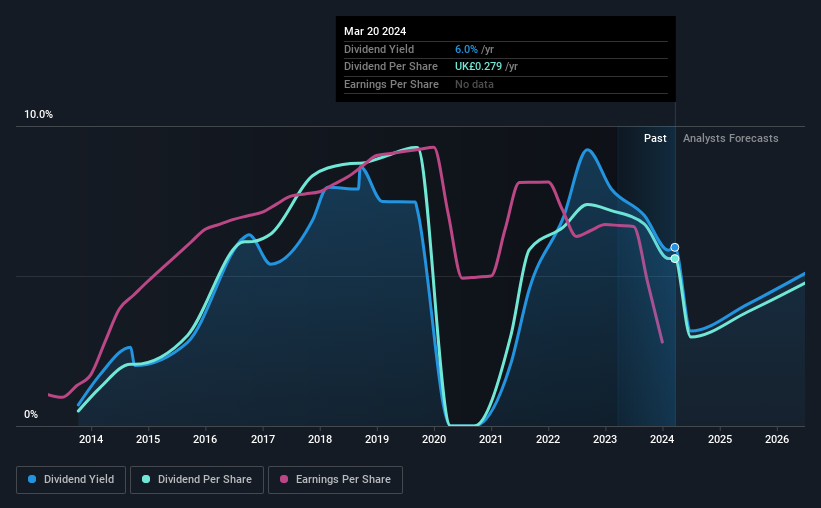

Barratt Developments plc (LON:BDEV) has announced that on 17th of May, it will be paying a dividend of£0.044, which a reduction from last year's comparable dividend. However, the dividend yield of 6.0% is still a decent boost to shareholder returns.

See our latest analysis for Barratt Developments

Barratt Developments' Dividend Is Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, the company's dividend was much higher than its earnings. Without profits and cash flows increasing, it would be difficult for the company to continue paying the dividend at this level.

The next year is set to see EPS grow by 83.5%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 75% which brings it into quite a comfortable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The dividend has gone from an annual total of £0.025 in 2014 to the most recent total annual payment of £0.279. This works out to be a compound annual growth rate (CAGR) of approximately 27% a year over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Over the past five years, it looks as though Barratt Developments' EPS has declined at around 21% a year. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this becomes a long term trend.

Barratt Developments' Dividend Doesn't Look Great

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company's earnings aren't high enough to be making such big distributions, and it isn't backed up by strong growth or consistency either. The dividend doesn't inspire confidence that it will provide solid income in the future.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 3 warning signs for Barratt Developments (1 is a bit concerning!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Barratt Redrow might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BTRW

Barratt Redrow

Engages in the housebuilding business in the United Kingdom.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

287 followersusers have followed this narrative

1 commentusers have commented on this narrative

42 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

98 followersusers have followed this narrative

2 commentsusers have commented on this narrative

28 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KI

kinnth on Reddit ·

Strong DAU drives Ads and AI Data narrative

Fair Value:US$309.7747.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Silver X Mining ·

Silver X Has 152 Million Ounces, Already Producing and Its Biggest Growth Phase May Still Be Ahead

Fair Value:CA$40.8998.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Cochlear ·

Cochlear’s Crossroads: Temporary Setback or Structural Shift?

Fair Value:AU$7042.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

98 followersusers have followed this narrative

2 commentsusers have commented on this narrative

28 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.229.5% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.1% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative