- United Kingdom

- /

- Banks

- /

- LSE:HSBA

Is HSBC (LSE:HSBA) Still Undervalued After Its Strong Recent Share Price Rally?

Reviewed by Simply Wall St

HSBC Holdings (LSE:HSBA) has quietly built momentum this year, with the share price up roughly 42% year to date and total return near 55% over the past year, outpacing many global banks.

See our latest analysis for HSBC Holdings.

That run has been underpinned by solid earnings momentum and rising profitability, with the latest 90 day share price return of 9.56% and a three year total shareholder return of 175.93% suggesting bullish sentiment is still building around the $11.118 stock.

If HSBC’s rally has you thinking beyond big banks, it could be a good moment to see what else is gaining traction via fast growing stocks with high insider ownership.

Yet with the shares now trading above analyst targets but still showing a hefty intrinsic discount, the key question is whether HSBC remains undervalued or if the market is already pricing in its next phase of growth.

Most Popular Narrative: 4.7% Overvalued

With HSBC Holdings last closing at £11.12 against a narrative fair value of about £10.62, the current share price already runs ahead of that central estimate, setting up a debate around how much future growth is being brought forward.

The strategic shift away from underperforming and non core businesses in Europe and the Americas, and redeployment of capital into high return businesses in Asia and the Middle East, is expected to improve overall net interest margins and boost group return on equity through better allocation of resources. Disproportionate investment in digital transformation, including AI driven efficiency gains and digital onboarding, will generate structural cost reductions (organizational simplification savings), directly improving the cost to income ratio and lifting long term operating leverage and net margins.

Want to see how steady revenue expansion, rising margins and a richer earnings multiple all fit together into that fair value math? The narrative leans on bold efficiency gains, ambitious profitability targets and a long runway for capital redeployment, but the exact assumptions behind those projections might surprise you.

Result: Fair Value of $10.62 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained Hong Kong property weakness, or sharper than expected Asian macro and regulatory headwinds, could easily derail those margin and earnings ambitions.

Find out about the key risks to this HSBC Holdings narrative.

Another Angle on Valuation

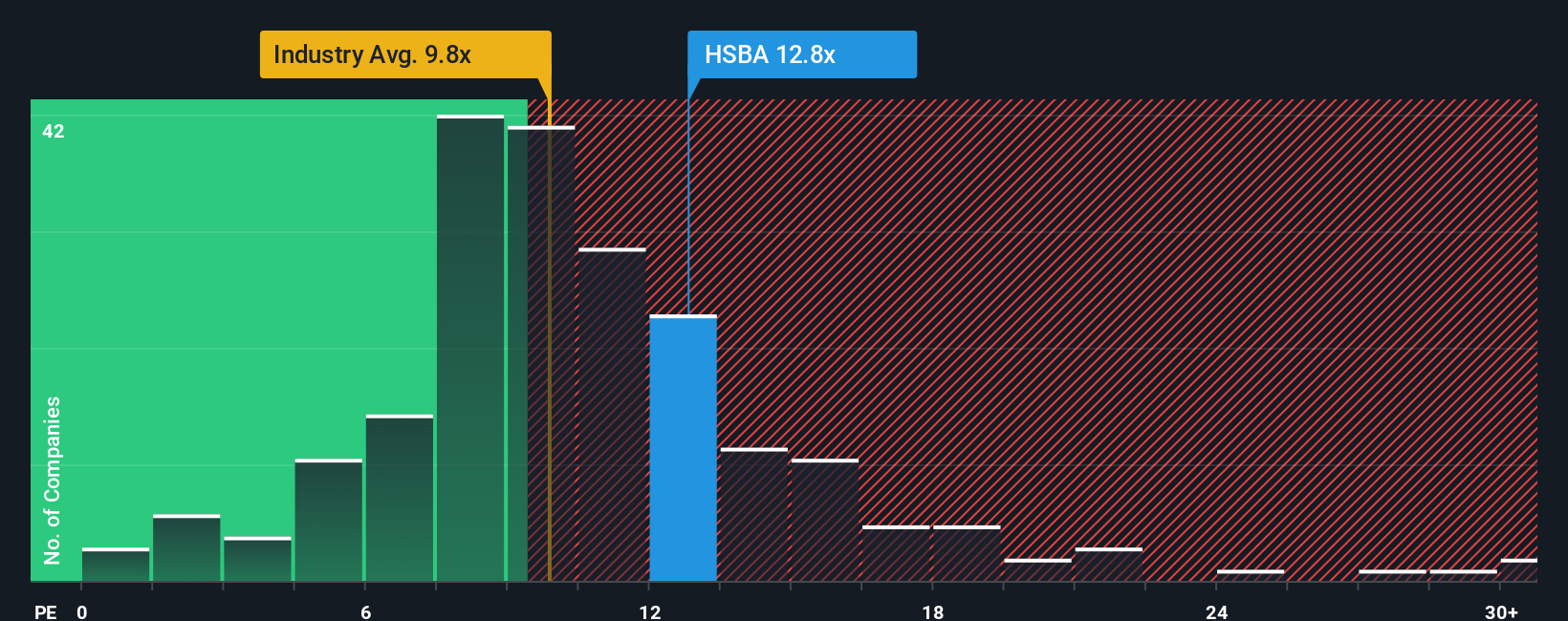

While the narrative fair value suggests HSBC is about 4.7% overvalued, its current price to earnings ratio of 15.4 times versus a European banks average of 10.5 times and a fair ratio of 10.2 times points to a much richer valuation that could cap upside if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out HSBC Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 915 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own HSBC Holdings Narrative

If you see the story differently, or would rather dig into the numbers yourself, you can spin up a tailored narrative in minutes: Do it your way.

A great starting point for your HSBC Holdings research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop with one bank when the market is full of potential. Use the Simply Wall Street Screener to uncover focused opportunities you might otherwise miss.

- Capture potential rebounds in overlooked names by scanning these 3633 penny stocks with strong financials that pair smaller market caps with surprisingly resilient fundamentals.

- Capitalize on major tech shifts by targeting these 25 AI penny stocks positioned at the intersection of artificial intelligence and scalable business models.

- Lock in value now by reviewing these 915 undervalued stocks based on cash flows where cash flow strength and discounted prices could set up powerful long term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if HSBC Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HSBA

HSBC Holdings

Engages in the provision of banking and financial products and services worldwide.

Adequate balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)