The Lectra SA (EPA:LSS) Third-Quarter Results Are Out And Analysts Have Published New Forecasts

Last week saw the newest third-quarter earnings release from Lectra SA (EPA:LSS), an important milestone in the company's journey to build a stronger business. Revenues came in 3.0% below expectations, at €132m. Statutory earnings per share were relatively better off, with a per-share profit of €0.89 being roughly in line with analyst estimates. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Lectra after the latest results.

See our latest analysis for Lectra

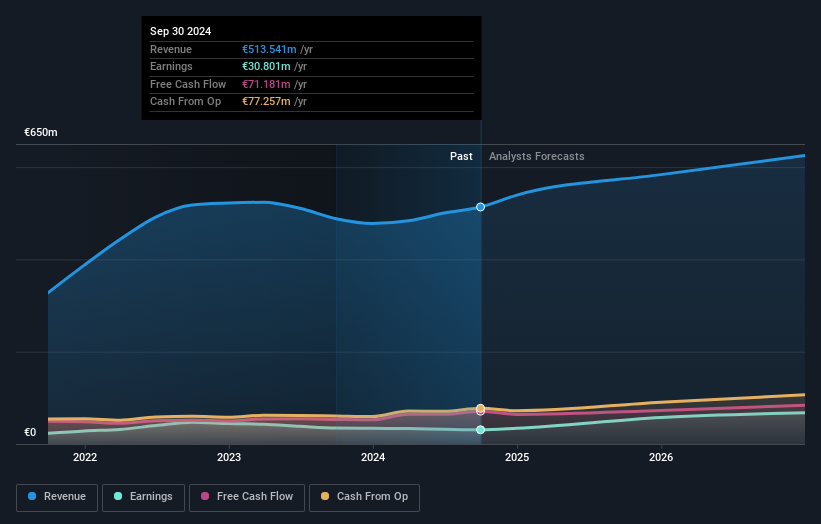

Following the latest results, Lectra's four analysts are now forecasting revenues of €583.6m in 2025. This would be a decent 14% improvement in revenue compared to the last 12 months. Per-share earnings are expected to bounce 84% to €1.50. Yet prior to the latest earnings, the analysts had been anticipated revenues of €605.1m and earnings per share (EPS) of €1.58 in 2025. The analysts are less bullish than they were before these results, given the reduced revenue forecasts and the small dip in earnings per share expectations.

The analysts made no major changes to their price target of €33.58, suggesting the downgrades are not expected to have a long-term impact on Lectra's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Lectra at €41.00 per share, while the most bearish prices it at €30.00. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Lectra's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 11% growth on an annualised basis. This is compared to a historical growth rate of 17% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 8.3% per year. Even after the forecast slowdown in growth, it seems obvious that Lectra is also expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. They also downgraded Lectra's revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. The consensus price target held steady at €33.58, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Lectra analysts - going out to 2026, and you can see them free on our platform here.

You can also see whether Lectra is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:LSS

Lectra

Provides industrial intelligence solutions for fashion, automotive, furniture markets, and other industries in Europe, the Americas, the Asia Pacific, and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)