Advertisement

Should You Be Adding FirstFarms (CPH:FFARMS) To Your Watchlist Today?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like FirstFarms (CPH:FFARMS). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide FirstFarms with the means to add long-term value to shareholders.

See our latest analysis for FirstFarms

How Fast Is FirstFarms Growing?

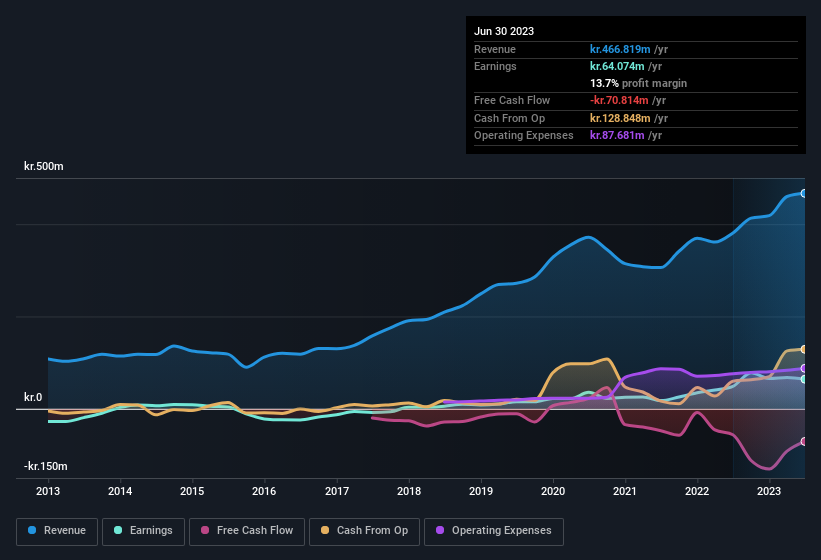

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. We can see that in the last three years FirstFarms grew its EPS by 8.2% per year. That's a pretty good rate, if the company can sustain it.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The music to the ears of FirstFarms shareholders is that EBIT margins have grown from 16% to 20% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

Since FirstFarms is no giant, with a market capitalisation of kr.796m, you should definitely check its cash and debt before getting too excited about its prospects.

Are FirstFarms Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

First and foremost; there we saw no insiders sell FirstFarms shares in the last year. Even better, though, is that the Chairman of the Board, Henrik Hougaard, bought a whopping kr.4.5m worth of shares, paying about kr.80.00 per share, on average. Big buys like that may signal an opportunity; actions speak louder than words.

And the insider buying isn't the only sign of alignment between shareholders and the board, since FirstFarms insiders own more than a third of the company. In fact, they own 38% of the shares, making insiders a very influential shareholder group. Those who are comforted by solid insider ownership like this should be happy, as it implies that those running the business are genuinely motivated to create shareholder value. To give you an idea, the value of insiders' holdings in the business are valued at kr.298m at the current share price. That should be more than enough to keep them focussed on creating shareholder value!

Does FirstFarms Deserve A Spot On Your Watchlist?

As previously touched on, FirstFarms is a growing business, which is encouraging. In addition, insiders have been busy adding to their sizeable holdings in the company. These factors alone make the company an interesting prospect for your watchlist, as well as continuing research. We don't want to rain on the parade too much, but we did also find 2 warning signs for FirstFarms that you need to be mindful of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of FirstFarms, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CPSE:FFARMS

FirstFarms

Through its subsidiaries, engages in the agriculture and food products businesses in Denmark, the Czech Republic, Slovakia, Hungary, and Romania.

Low risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor