- Germany

- /

- Real Estate

- /

- XTRA:AT1

Growth Investors: Industry Analysts Just Upgraded Their Aroundtown SA (ETR:AT1) Revenue Forecasts By 10%

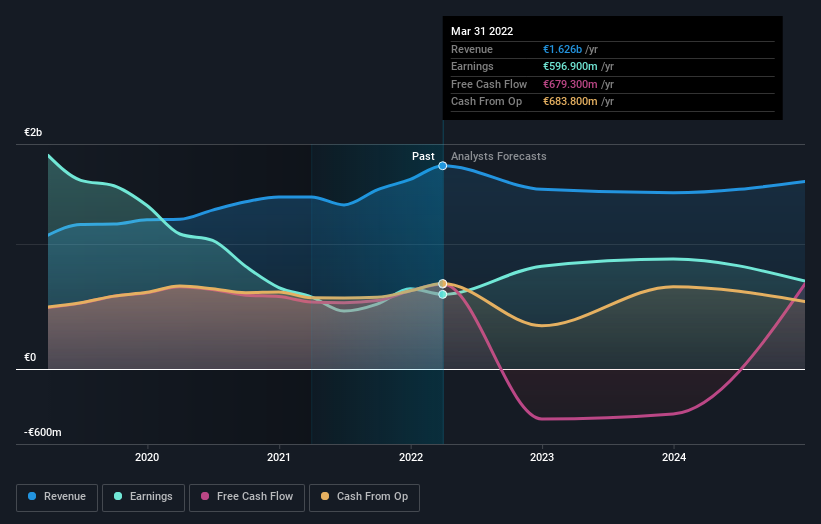

Celebrations may be in order for Aroundtown SA (ETR:AT1) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline.

Following the latest upgrade, the ten analysts covering Aroundtown provided consensus estimates of €1.5b revenue in 2022, which would reflect a not inconsiderable 10% decline on its sales over the past 12 months. Per-share earnings are expected to surge 25% to €0.68. Prior to this update, the analysts had been forecasting revenues of €1.3b and earnings per share (EPS) of €0.56 in 2022. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

Check out our latest analysis for Aroundtown

Although the analysts have upgraded their earnings estimates, there was no change to the consensus price target of €6.74, suggesting that the forecast performance does not have a long term impact on the company's valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Aroundtown, with the most bullish analyst valuing it at €8.40 and the most bearish at €4.50 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with a forecast 13% annualised revenue decline to the end of 2022. That is a notable change from historical growth of 18% over the last five years. Yet aggregate analyst estimates for other companies in the industry suggest that industry revenues are forecast to decline 11% per year.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Fortunately analysts also upgraded their revenue estimates, with sales performing well and Aroundtown's revenues performing in line with the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Aroundtown.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Aroundtown analysts - going out to 2024, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you're looking to trade Aroundtown, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:AT1

Aroundtown

Operates as a real estate company in Germany, the Netherlands, the United Kingdom, Belgium, and internationally.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Community Narratives