Advertisement

- Germany

- /

- Healthtech

- /

- XTRA:COP

Here's Why CompuGroup Medical SE KGaA (ETR:COP) Has A Meaningful Debt Burden

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, CompuGroup Medical SE & Co. KGaA (ETR:COP) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for CompuGroup Medical SE KGaA

What Is CompuGroup Medical SE KGaA's Debt?

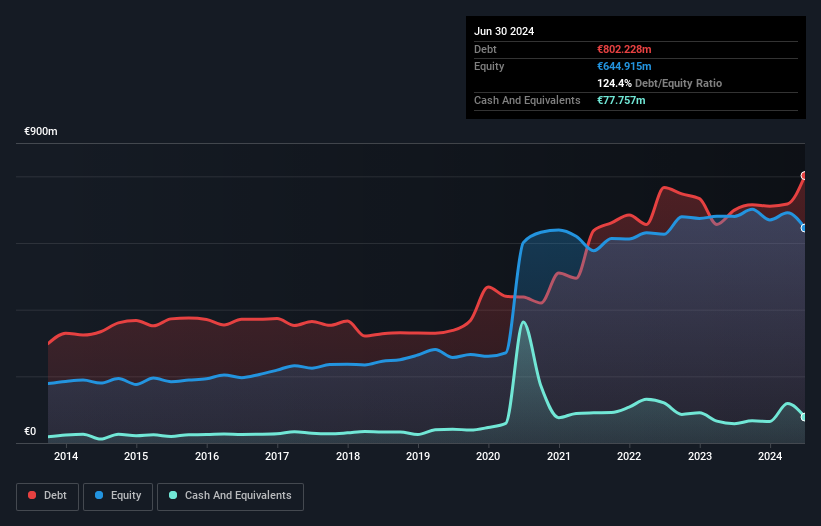

You can click the graphic below for the historical numbers, but it shows that as of June 2024 CompuGroup Medical SE KGaA had €802.2m of debt, an increase on €698.8m, over one year. However, it also had €77.8m in cash, and so its net debt is €724.5m.

How Strong Is CompuGroup Medical SE KGaA's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that CompuGroup Medical SE KGaA had liabilities of €395.5m due within 12 months and liabilities of €933.5m due beyond that. Offsetting these obligations, it had cash of €77.8m as well as receivables valued at €242.1m due within 12 months. So it has liabilities totalling €1.01b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of €826.7m, we think shareholders really should watch CompuGroup Medical SE KGaA's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

CompuGroup Medical SE KGaA has a debt to EBITDA ratio of 4.9 and its EBIT covered its interest expense 3.6 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Worse, CompuGroup Medical SE KGaA's EBIT was down 32% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if CompuGroup Medical SE KGaA can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, CompuGroup Medical SE KGaA recorded free cash flow worth 72% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

We'd go so far as to say CompuGroup Medical SE KGaA's EBIT growth rate was disappointing. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. We should also note that Healthcare Services industry companies like CompuGroup Medical SE KGaA commonly do use debt without problems. Overall, we think it's fair to say that CompuGroup Medical SE KGaA has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for CompuGroup Medical SE KGaA you should be aware of, and 1 of them shouldn't be ignored.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:COP

CompuGroup Medical SE KGaA

Provides e-health services in Germany, Western and Eastern Europe, North America, and internationally.

Slight risk with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor