- Germany

- /

- Diversified Financial

- /

- XTRA:HYQ

Hypoport SE Beat Revenue Forecasts By 25%: Here's What Analysts Are Forecasting Next

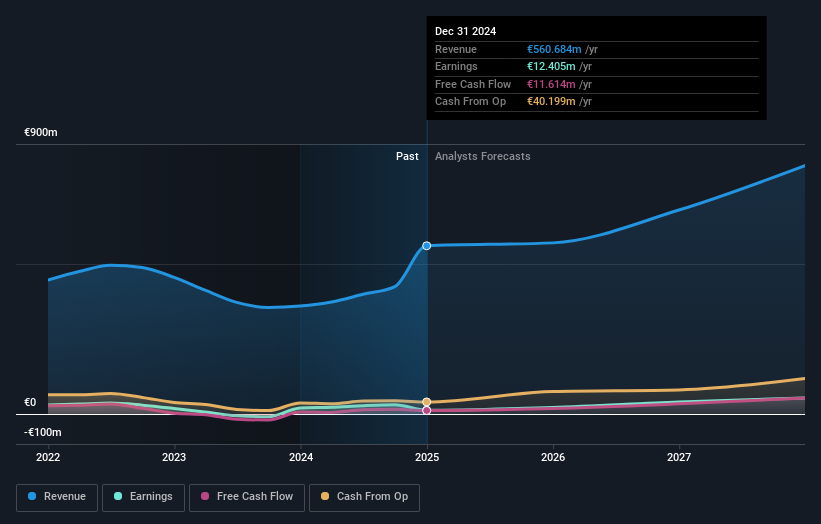

Hypoport SE (ETR:HYQ) just released its annual report and things are looking bullish. Performance was better than the analysts expected, with revenues of €561m coming in25% ahead of expectations, and statutory earnings per share (EPS) of €1.85 exceeding forecasts by 14%. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Following last week's earnings report, Hypoport's six analysts are forecasting 2025 revenues to be €570.4m, approximately in line with the last 12 months. Per-share earnings are expected to shoot up 93% to €3.58. Yet prior to the latest earnings, the analysts had been anticipated revenues of €552.7m and earnings per share (EPS) of €3.56 in 2025. There doesn't appear to have been a major change in sentiment following the results, other than the small increase to revenue estimates.

View our latest analysis for Hypoport

It may not be a surprise to see thatthe analysts have reconfirmed their price target of €258, implying that the uplift in revenue is not expected to greatly contribute to Hypoport's valuation in the near term. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Hypoport at €318 per share, while the most bearish prices it at €210. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Hypoport's past performance and to peers in the same industry. We would highlight that Hypoport's revenue growth is expected to slow, with the forecast 1.7% annualised growth rate until the end of 2025 being well below the historical 3.2% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 13% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Hypoport.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Fortunately, they also upgraded their revenue estimates, although our data indicates it is expected to perform worse than the wider industry. The consensus price target held steady at €258, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Hypoport analysts - going out to 2027, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 1 warning sign for Hypoport that you should be aware of.

If you're looking to trade Hypoport, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hypoport might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:HYQ

Hypoport

Develops, operates, and markets technology platforms for the credit, housing, and insurance industries in Germany.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives