Advertisement

- Czech Republic

- /

- Aerospace & Defense

- /

- SEP:CZG

Colt CZ Group SE's (SEP:CZG) Financials Are Too Obscure To Link With Current Share Price Momentum: What's In Store For the Stock?

Colt CZ Group (SEP:CZG) has had a great run on the share market with its stock up by a significant 7.5% over the last month. But the company's key financial indicators appear to be differing across the board and that makes us question whether or not the company's current share price momentum can be maintained. Specifically, we decided to study Colt CZ Group's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How Is ROE Calculated?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Colt CZ Group is:

6.1% = Kč1.3b ÷ Kč21b (Based on the trailing twelve months to March 2025).

The 'return' is the profit over the last twelve months. That means that for every CZK1 worth of shareholders' equity, the company generated CZK0.06 in profit.

View our latest analysis for Colt CZ Group

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Colt CZ Group's Earnings Growth And 6.1% ROE

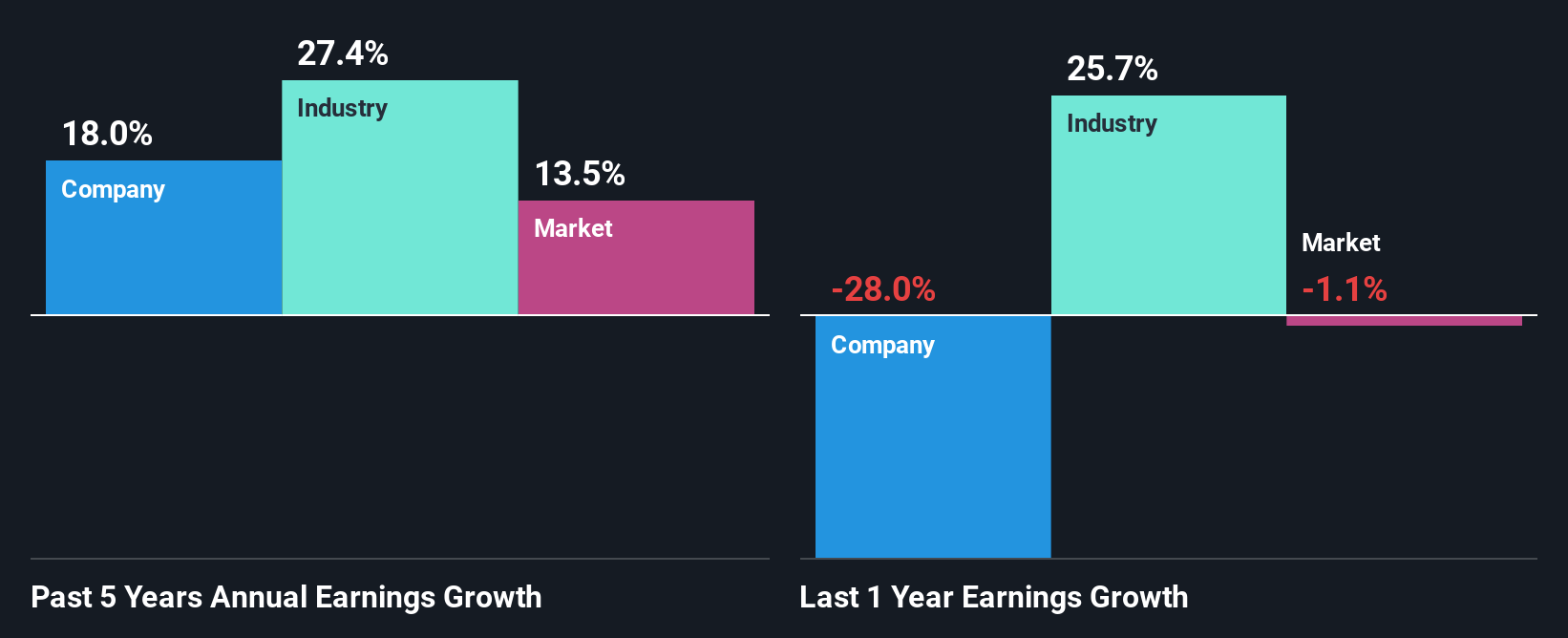

At first glance, Colt CZ Group's ROE doesn't look very promising. A quick further study shows that the company's ROE doesn't compare favorably to the industry average of 13% either. Colt CZ Group was still able to see a decent net income growth of 18% over the past five years. So, the growth in the company's earnings could probably have been caused by other variables. For instance, the company has a low payout ratio or is being managed efficiently.

Next, on comparing with the industry net income growth, we found that Colt CZ Group's reported growth was lower than the industry growth of 27% over the last few years, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Has the market priced in the future outlook for CZG? You can find out in our latest intrinsic value infographic research report.

Is Colt CZ Group Efficiently Re-investing Its Profits?

Colt CZ Group has a significant three-year median payout ratio of 63%, meaning that it is left with only 37% to reinvest into its business. This implies that the company has been able to achieve decent earnings growth despite returning most of its profits to shareholders.

Additionally, Colt CZ Group has paid dividends over a period of four years which means that the company is pretty serious about sharing its profits with shareholders. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 68% of its profits over the next three years. Still, forecasts suggest that Colt CZ Group's future ROE will rise to 14% even though the the company's payout ratio is not expected to change by much.

Conclusion

On the whole, we feel that the performance shown by Colt CZ Group can be open to many interpretations. Although the company has shown a fair bit of growth in earnings, the reinvestment rate is low. Meaning, the earnings growth number could have been significantly higher had the company been retaining more of its profits and reinvesting that at a higher rate of return. We also studied the latest analyst forecasts and found that the company's earnings growth is expected be similar to its current growth rate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEP:CZG

Colt CZ Group

Engages in the production and sale of firearms, ammunition products, and tactical accessories in the Czech Republic, Canada the United States, rest of Europe, Africa, Asia, and internationally.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor