Advertisement

The market seemed underwhelmed by the solid earnings posted by Citic Press Corporation (SZSE:300788) recently. Along with the solid headline numbers, we think that investors have some reasons for optimism.

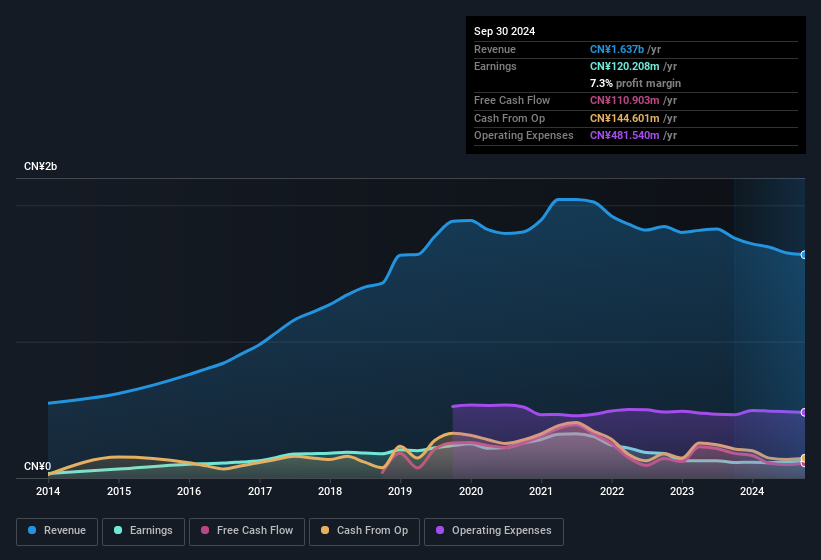

Check out our latest analysis for Citic Press

How Do Unusual Items Influence Profit?

Importantly, our data indicates that Citic Press' profit was reduced by CN¥27m, due to unusual items, over the last year. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Citic Press to produce a higher profit next year, all else being equal.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Citic Press' Profit Performance

Unusual items (expenses) detracted from Citic Press' earnings over the last year, but we might see an improvement next year. Because of this, we think Citic Press' earnings potential is at least as good as it seems, and maybe even better! And on top of that, its earnings per share increased by 6.5% in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. If you'd like to know more about Citic Press as a business, it's important to be aware of any risks it's facing. To that end, you should learn about the 2 warning signs we've spotted with Citic Press (including 1 which is a bit concerning).

This note has only looked at a single factor that sheds light on the nature of Citic Press' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300788

Citic Press

Engages in the book publishing and distribution, knowledge service, and cultural consumption businesses in China and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.1% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|22.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.6% undervalued

RO

Community Contributor