3 Growth Companies With High Insider Ownership And Up To 88% Earnings Growth

Reviewed by Simply Wall St

As global markets show resilience with U.S. indexes nearing record highs and broad-based gains across sectors, investors are keenly observing the interplay of geopolitical tensions and economic indicators like jobless claims and home sales. In such an environment, companies with strong insider ownership often signal confidence in their growth potential, making them attractive prospects for those seeking to capitalize on market opportunities.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 31.1% | 43.2% |

| SKS Technologies Group (ASX:SKS) | 32.4% | 24.8% |

| On Holding (NYSE:ONON) | 19.1% | 29.6% |

| Pharma Mar (BME:PHM) | 11.8% | 56.9% |

| Medley (TSE:4480) | 34% | 31.7% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 103.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.7% | 95% |

| Alkami Technology (NasdaqGS:ALKT) | 11% | 98.6% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

Let's explore several standout options from the results in the screener.

Zhejiang Starry PharmaceuticalLtd (SHSE:603520)

Simply Wall St Growth Rating: ★★★★★☆

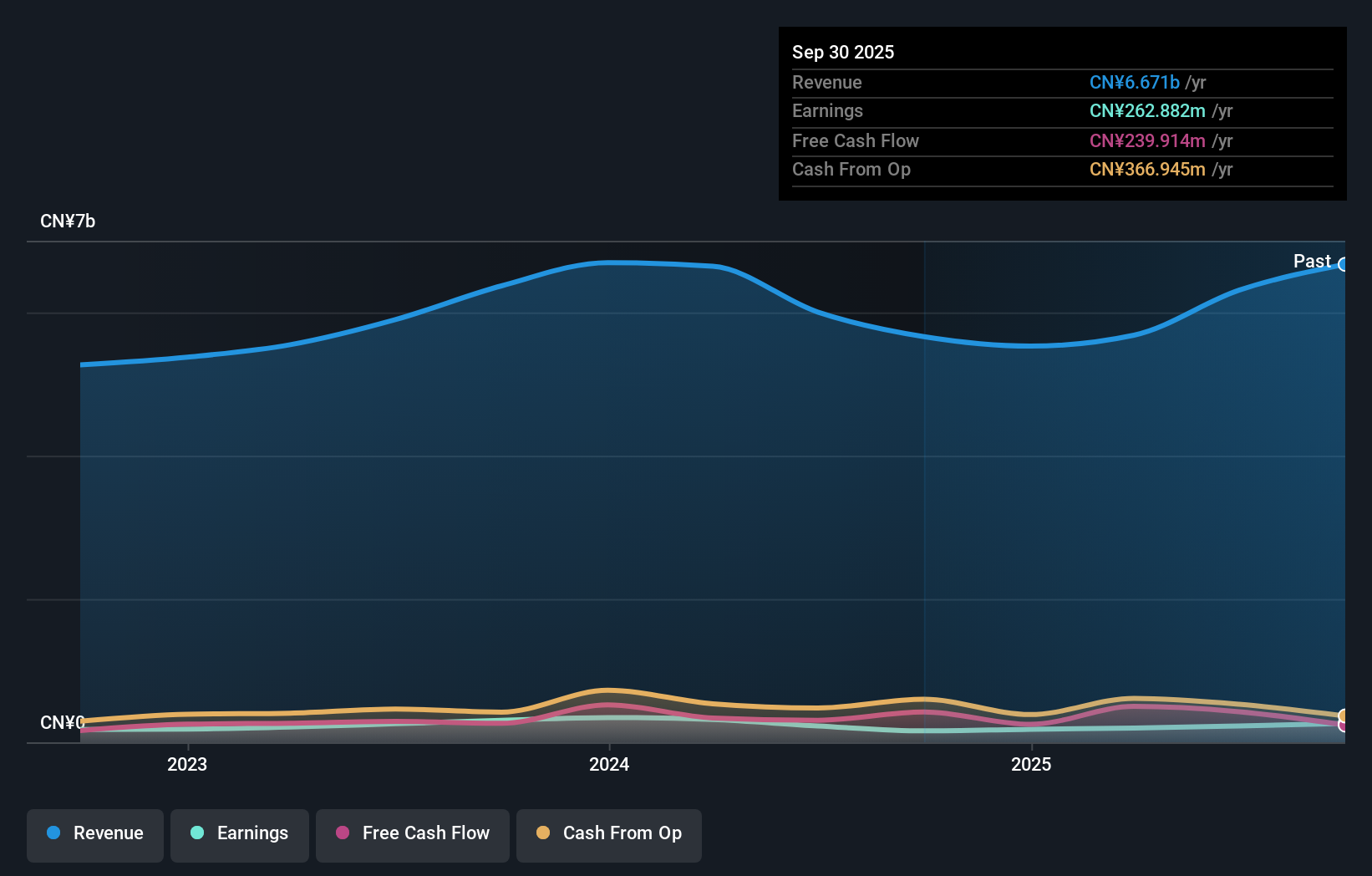

Overview: Zhejiang Starry Pharmaceutical Co., Ltd. is involved in the research, development, production, and sale of X-CT non-ionic contrast agents and fluoroquinolones drugs and intermediates both in China and internationally, with a market cap of CN¥4.18 billion.

Operations: The company generates revenue through the production and sale of X-CT non-ionic contrast agents and fluoroquinolones drugs and intermediates in both domestic and international markets.

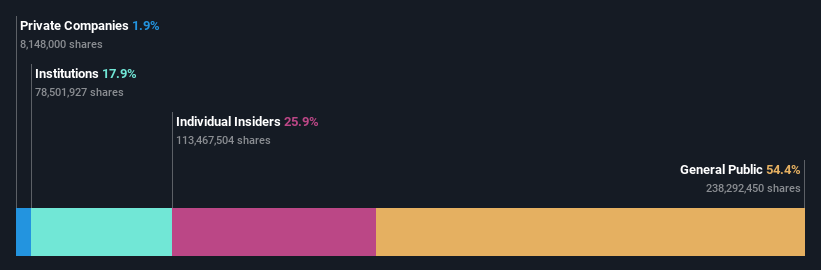

Insider Ownership: 25.9%

Earnings Growth Forecast: 88.7% p.a.

Zhejiang Starry Pharmaceutical Ltd. is positioned for significant growth, with earnings projected to rise 88.7% annually, outpacing the Chinese market. Despite recent shareholder dilution and low return on equity forecasts, the company's revenue is expected to grow at 22.8% per year, surpassing industry averages. Recent insider transactions include Ni Lianhui's acquisition of a 5.02% stake for CNY 160 million, indicating confidence in future prospects despite current financial challenges such as unsustainable dividends and interest coverage issues.

- Get an in-depth perspective on Zhejiang Starry PharmaceuticalLtd's performance by reading our analyst estimates report here.

- Our expertly prepared valuation report Zhejiang Starry PharmaceuticalLtd implies its share price may be lower than expected.

Xiamen Jihong Technology (SZSE:002803)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Xiamen Jihong Technology Co., Ltd. operates in the cross-border social e-commerce sector in Southeast Asia, with a market cap of CN¥5.76 billion.

Operations: The company's revenue segments include cross-border social e-commerce operations in Southeast Asia.

Insider Ownership: 35%

Earnings Growth Forecast: 38.1% p.a.

Xiamen Jihong Technology is poised for growth, with earnings expected to increase by 38.1% annually, surpassing the Chinese market's average. Despite a drop in net profit margin from last year and lower sales figures, the company plans a share buyback of up to CNY 100 million to enhance employee incentives and support long-term development. The stock is considered undervalued, trading significantly below its estimated fair value, although dividend sustainability remains uncertain.

- Dive into the specifics of Xiamen Jihong Technology here with our thorough growth forecast report.

- Upon reviewing our latest valuation report, Xiamen Jihong Technology's share price might be too pessimistic.

Jiangsu Kuangshun Photosensitivity New-Material Stock (SZSE:300537)

Simply Wall St Growth Rating: ★★★★★☆

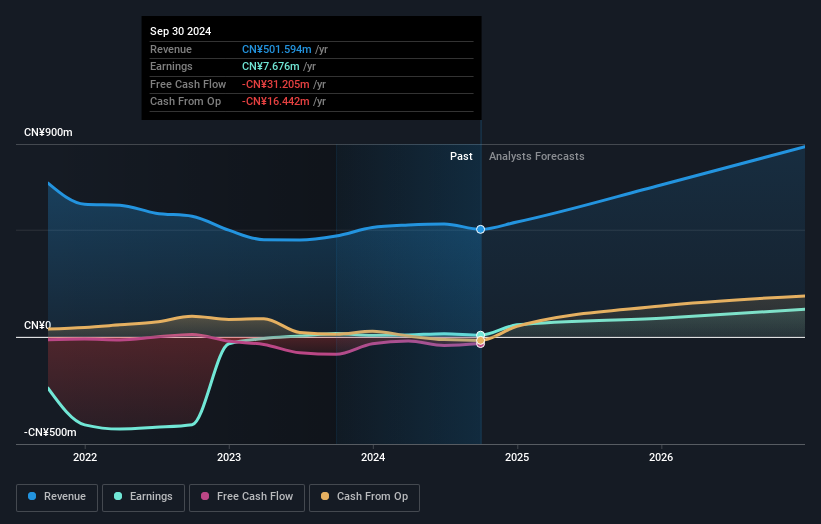

Overview: Jiangsu Kuangshun Photosensitivity New-Material Stock Co., Ltd. operates in the photosensitive materials industry with a market cap of CN¥4.24 billion.

Operations: The company generates revenue from the fine chemicals industry, amounting to CN¥501.59 million.

Insider Ownership: 37.5%

Earnings Growth Forecast: 67.9% p.a.

Jiangsu Kuangshun Photosensitivity New-Material is projected to experience significant earnings growth of 67.9% annually, outpacing the Chinese market. Despite a volatile share price and decreased profit margins from last year, the company's revenue is expected to grow at 26.2% per year, exceeding both market and high-growth benchmarks. Recent financial results show stable net income with slight improvements over last year, while upcoming shareholder actions include stock repurchase plans and capital amendments.

- Click here to discover the nuances of Jiangsu Kuangshun Photosensitivity New-Material Stock with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of Jiangsu Kuangshun Photosensitivity New-Material Stock shares in the market.

Taking Advantage

- Navigate through the entire inventory of 1529 Fast Growing Companies With High Insider Ownership here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002803

Xiamen Jihong Technology

Engages in the cross-border social e-commerce business in China.

Flawless balance sheet with high growth potential.