- China

- /

- General Merchandise and Department Stores

- /

- SHSE:600814

Hangzhou Jiebai Group Joins 3 Undiscovered Gems For Your Portfolio

Reviewed by Simply Wall St

As global markets navigate a cautious economic landscape marked by interest rate adjustments and political uncertainties, small-cap stocks have experienced heightened volatility, with indices like the S&P 600 reflecting this trend. In such an environment, identifying promising yet under-the-radar companies can offer potential opportunities for portfolio diversification and growth. A good stock in these conditions often combines strong fundamentals with resilience to broader market fluctuations, making it a valuable addition to any investor's watchlist.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sun | 14.28% | 5.73% | 64.26% | ★★★★★★ |

| Caisse Régionale de Crédit Agricole Mutuel Brie Picardie Société coopérative | 34.89% | 3.23% | 3.61% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Top Union Electronics | 1.25% | 6.67% | 17.52% | ★★★★★★ |

| Yulie Sekuritas Indonesia | NA | 18.62% | 9.58% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Chita Kogyo | 8.34% | 2.84% | 8.49% | ★★★★★☆ |

| Union Coop | NA | -4.69% | -14.06% | ★★★★☆☆ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

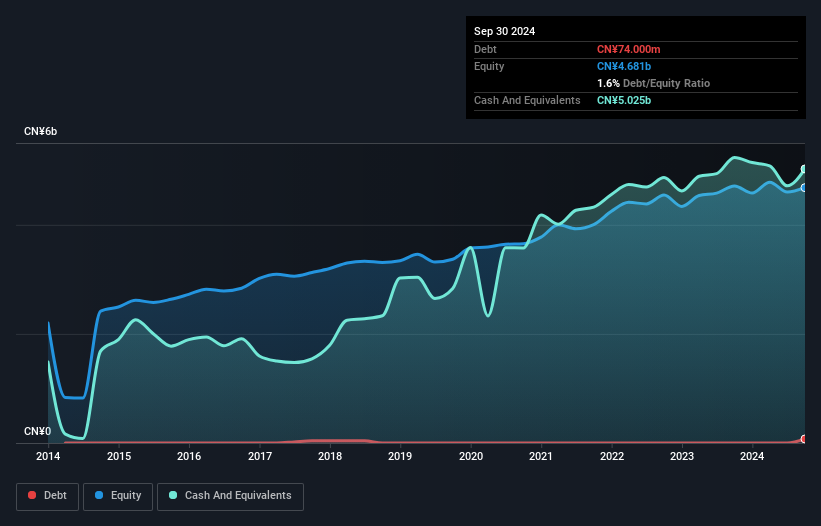

Hangzhou Jiebai Group (SHSE:600814)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hangzhou Jiebai Group Co., Limited operates department stores and shopping centers in China, with a market cap of CN¥5.81 billion.

Operations: The primary revenue streams for Hangzhou Jiebai Group are derived from its department stores and shopping centers. The company's financial performance is influenced by the cost structure associated with these operations.

Hangzhou Jiebai Group, a relatively small player in the retail sector, has shown mixed performance recently. The company reported sales of CNY 1.32 billion for the first nine months of 2024, down from CNY 1.55 billion last year, while net income slipped to CNY 239 million from CNY 253 million. Despite these challenges, it trades at a significant discount to its estimated fair value and maintains high-quality earnings with more cash than debt on its balance sheet. Negative earnings growth of -3.8% contrasts with industry averages but suggests potential for recovery if conditions improve.

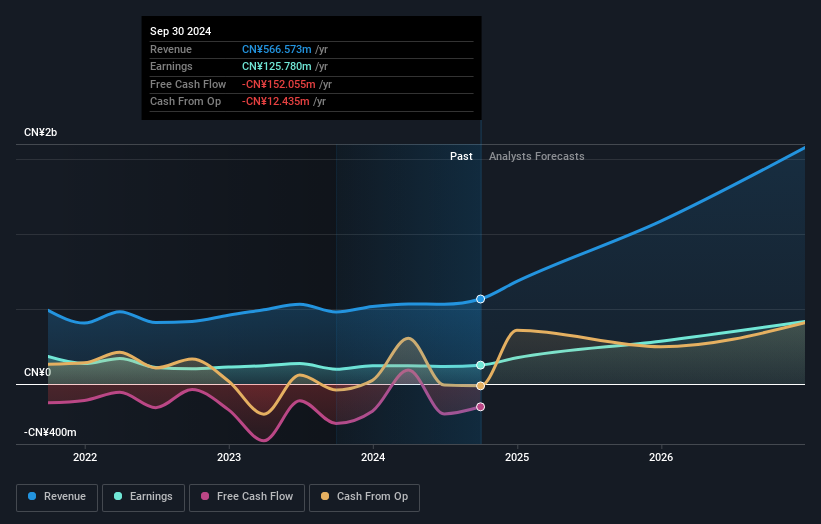

Jilin OLED Material Tech (SHSE:688378)

Simply Wall St Value Rating: ★★★★★☆

Overview: Jilin OLED Material Tech Co., Ltd. focuses on the research, development, production, and sale of organic electroluminescent materials and equipment for the new display industry in China, with a market cap of CN¥4.69 billion.

Operations: Jilin OLED Material Tech generates revenue primarily through the sale of organic electroluminescent materials and equipment. The company's financial performance is influenced by its cost structure, which impacts its profitability. Notably, it has experienced fluctuations in net profit margin over recent periods.

Jilin OLED Material Tech, a notable player in the electronic sector, has demonstrated robust performance with earnings surging 27.2% over the past year, outpacing the industry's modest 1.9% growth. The company reported sales of CN¥463.79 million for the first nine months of 2024, up from CN¥414.5 million last year, and net income increased to CN¥101.25 million from CN¥97.74 million. Despite a volatile share price recently, Jilin's debt-to-equity ratio has impressively decreased from 12.4% to 3.3% over five years, reflecting prudent financial management amidst its competitive pricing with a P/E ratio of 39x against an industry average of 47x.

- Click here and access our complete health analysis report to understand the dynamics of Jilin OLED Material Tech.

Learn about Jilin OLED Material Tech's historical performance.

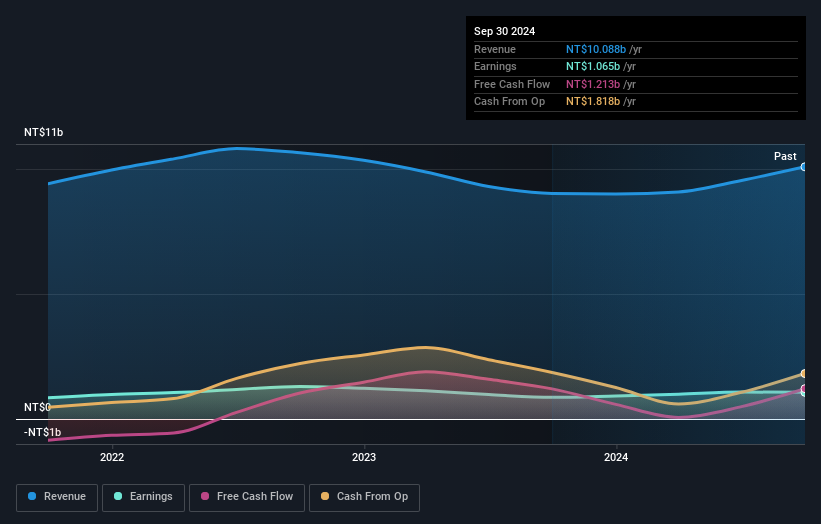

Lelon Electronics (TWSE:2472)

Simply Wall St Value Rating: ★★★★★★

Overview: Lelon Electronics Corp. is engaged in the development, manufacturing, marketing, trading, and sales of electrolytic capacitors globally with a market capitalization of approximately NT$13.46 billion.

Operations: Lelon Electronics generates revenue primarily from its LELON Department, contributing NT$6.29 billion, and the Li Dun Department, adding NT$4.15 billion.

Lelon Electronics, a small yet promising player in the electronics industry, has been making strides with its impressive earnings growth of 23.2% over the past year, outpacing the industry's 6.6%. The company's price-to-earnings ratio of 13.4x is notably lower than the TW market average of 21x, suggesting potential undervaluation. Over five years, Lelon's debt-to-equity ratio improved from 68.9% to a more manageable 20.1%, indicating sound financial management. Recent reports show third-quarter sales rising to TWD 2,791 million from TWD 2,244 million last year; however, net income slightly decreased to TWD 264 million from TWD 279 million previously.

- Dive into the specifics of Lelon Electronics here with our thorough health report.

Evaluate Lelon Electronics' historical performance by accessing our past performance report.

Turning Ideas Into Actions

- Unlock more gems! Our Undiscovered Gems With Strong Fundamentals screener has unearthed 4629 more companies for you to explore.Click here to unveil our expertly curated list of 4632 Undiscovered Gems With Strong Fundamentals.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Jiebai Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600814

Hangzhou Jiebai Group

Operates department stores and shopping centers in China.

Excellent balance sheet, good value and pays a dividend.