Advertisement

3 Growth Companies With High Insider Ownership Growing Revenues At 14%

Simply Wall St

Reviewed by Simply Wall St

In the face of recent market volatility, characterized by cautious Federal Reserve commentary and political uncertainties, investors are increasingly focused on finding resilient growth opportunities. Amid these conditions, companies with high insider ownership and robust revenue growth can offer a compelling investment profile, as they often align management interests with shareholders while demonstrating strong financial performance.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 23.9% | 37.6% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| On Holding (NYSE:ONON) | 19.1% | 29.4% |

| Pharma Mar (BME:PHM) | 11.8% | 56.2% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.4% | 66.3% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's dive into some prime choices out of the screener.

Jilin OLED Material Tech (SHSE:688378)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jilin OLED Material Tech Co., Ltd. focuses on the research, development, production, and sale of organic electroluminescent materials and equipment for China's new display industry, with a market cap of CN¥4.69 billion.

Operations: Jilin OLED Material Tech Co., Ltd. generates revenue through its activities in the research, development, production, and sale of organic electroluminescent materials and equipment for the new display industry in China.

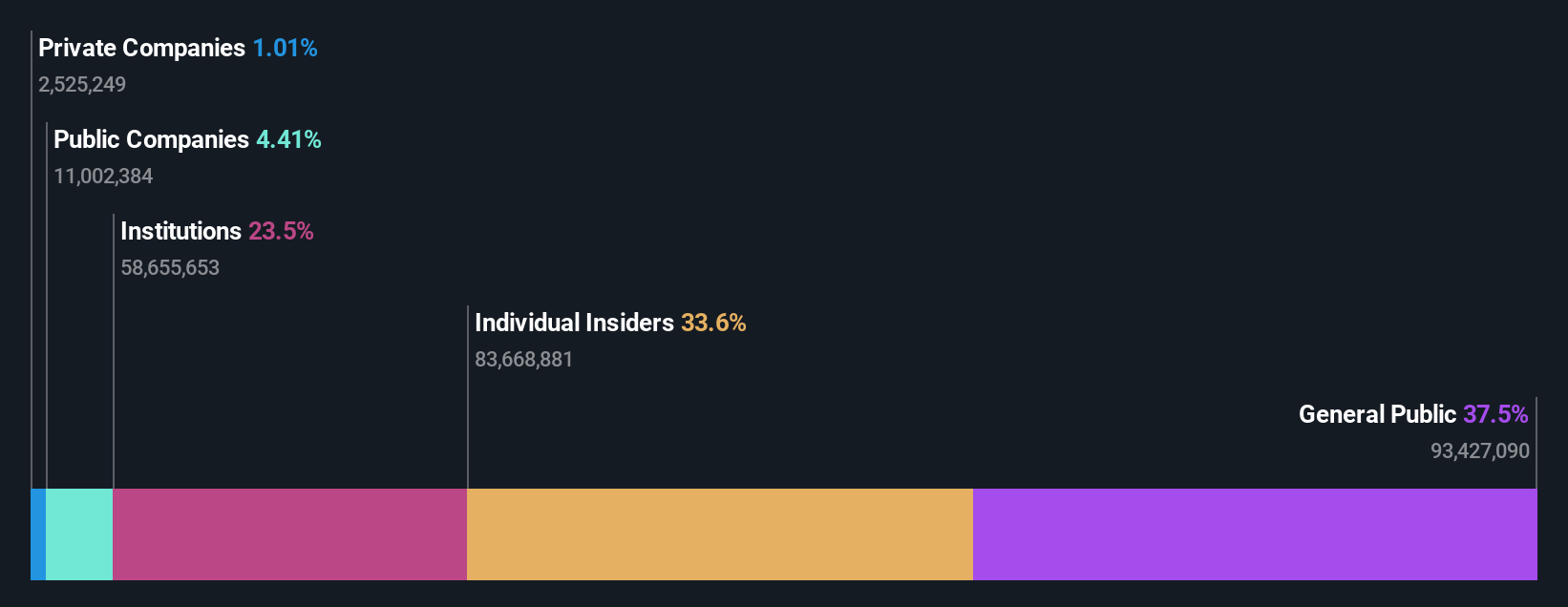

Insider Ownership: 32.6%

Revenue Growth Forecast: 45.1% p.a.

Jilin OLED Material Tech demonstrates strong growth potential, with earnings forecasted to grow at 49.93% annually, outpacing the CN market average. Despite volatile share prices recently, the company trades at a good value with a P/E ratio of 39x below industry average. Revenue for nine months ended September 2024 increased to CNY 463.79 million from CNY 414.5 million year-on-year, indicating solid performance despite low dividend coverage and no recent insider trading activity reported.

- Click here to discover the nuances of Jilin OLED Material Tech with our detailed analytical future growth report.

- Our valuation report unveils the possibility Jilin OLED Material Tech's shares may be trading at a discount.

Sichuan Shudao Equipment & TechnologyLtd (SZSE:300540)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sichuan Shudao Equipment & Technology Co., Ltd. operates in the equipment and technology sector with a market capitalization of CN¥3.85 billion.

Operations: The company generates revenue primarily from its General Equipment Manufacturing segment, totaling CN¥818.07 million.

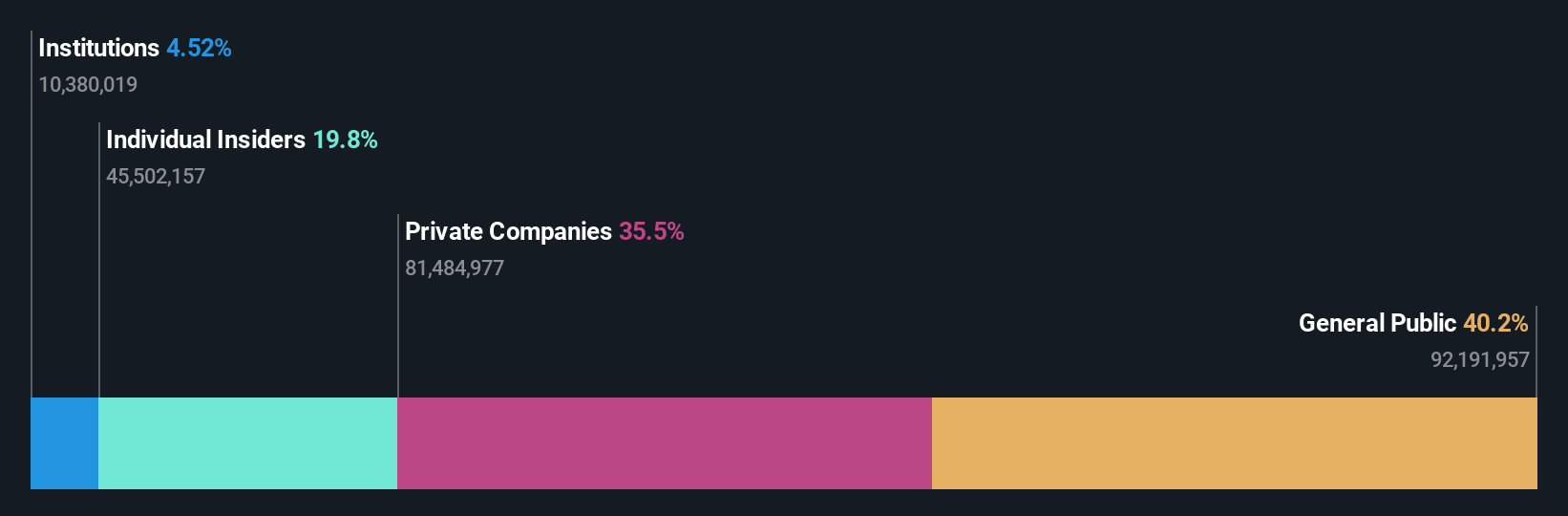

Insider Ownership: 19.8%

Revenue Growth Forecast: 14.2% p.a.

Sichuan Shudao Equipment & Technology Ltd. is poised for substantial earnings growth, with forecasts suggesting an annual increase of 41.94%, surpassing the CN market's 25.4% average. Despite a highly volatile share price recently, the company reported strong financial performance for the nine months ending September 2024, with revenue rising to CNY 496.7 million from CNY 346.98 million and net income increasing to CNY 23.19 million from CNY 13.87 million year-on-year, though its Return on Equity is expected to remain low at 8.1%.

- Delve into the full analysis future growth report here for a deeper understanding of Sichuan Shudao Equipment & TechnologyLtd.

- Our comprehensive valuation report raises the possibility that Sichuan Shudao Equipment & TechnologyLtd is priced higher than what may be justified by its financials.

JAPAN MATERIAL (TSE:6055)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: JAPAN MATERIAL Co., Ltd. operates in the electronics and graphics sectors in Japan with a market cap of approximately ¥172.73 billion.

Operations: The company generates revenue from its Electronics segment with ¥46.94 billion, Graphics Solution Business with ¥1.67 billion, and Solar Power Generation Business with ¥205 million.

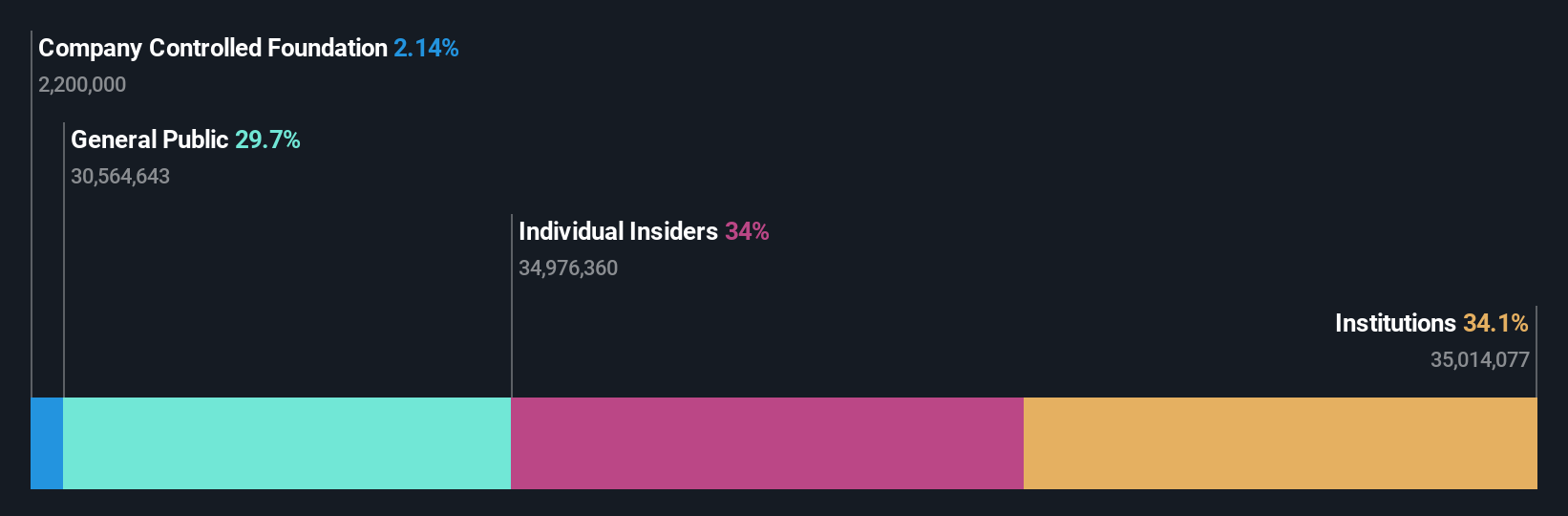

Insider Ownership: 35.3%

Revenue Growth Forecast: 14.1% p.a.

Japan Material's earnings are projected to grow significantly at 20.6% annually, outpacing the JP market average of 7.9%. The company's revenue is also expected to rise by 14.1% per year, faster than the market's 4.2%. Currently trading below its estimated fair value, Japan Material offers potential for appreciation despite a volatile share price and a forecasted low Return on Equity of 17.4% in three years.

- Get an in-depth perspective on JAPAN MATERIAL's performance by reading our analyst estimates report here.

- The analysis detailed in our JAPAN MATERIAL valuation report hints at an inflated share price compared to its estimated value.

Turning Ideas Into Actions

- Click here to access our complete index of 1512 Fast Growing Companies With High Insider Ownership.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300540

Sichuan Shudao Equipment & TechnologyLtd

Sichuan Shudao Equipment & Technology Co.,Ltd.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor