Advertisement

Is China South Publishing & Media Group Co., Ltd's (SHSE:601098) Recent Stock Performance Influenced By Its Financials In Any Way?

China South Publishing & Media Group's (SHSE:601098) stock is up by 9.0% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to investigate if the company's decent financials had a hand to play in the recent price move. In this article, we decided to focus on China South Publishing & Media Group's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for China South Publishing & Media Group

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for China South Publishing & Media Group is:

11% = CN¥1.7b ÷ CN¥16b (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. So, this means that for every CN¥1 of its shareholder's investments, the company generates a profit of CN¥0.11.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

China South Publishing & Media Group's Earnings Growth And 11% ROE

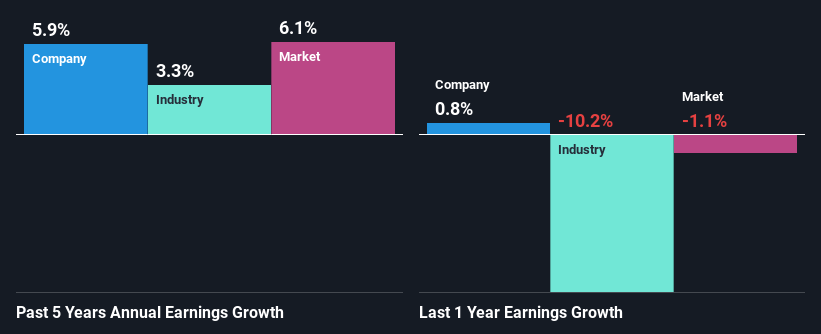

When you first look at it, China South Publishing & Media Group's ROE doesn't look that attractive. However, the fact that the company's ROE is higher than the average industry ROE of 6.5%, is definitely interesting. This probably goes some way in explaining China South Publishing & Media Group's moderate 5.9% growth over the past five years amongst other factors. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. So there might well be other reasons for the earnings to grow. Such as- high earnings retention or the company belonging to a high growth industry.

Next, on comparing with the industry net income growth, we found that China South Publishing & Media Group's growth is quite high when compared to the industry average growth of 3.3% in the same period, which is great to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about China South Publishing & Media Group's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is China South Publishing & Media Group Making Efficient Use Of Its Profits?

While China South Publishing & Media Group has a three-year median payout ratio of 74% (which means it retains 26% of profits), the company has still seen a fair bit of earnings growth in the past, meaning that its high payout ratio hasn't hampered its ability to grow.

Besides, China South Publishing & Media Group has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Summary

In total, it does look like China South Publishing & Media Group has some positive aspects to its business. Especially the substantial growth in earnings backed by a decent ROE. Despite the company reinvesting only a small portion of its profits, it still has managed to grow its earnings so that is appreciable. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601098

China South Publishing & Media Group

Engages in publishing, printing, distribution, media, and financing businesses in China.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor