3 Growth Companies With High Insider Ownership Growing Revenue Over 21%

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by inflation concerns and political uncertainties, investors are keeping a close eye on growth stocks, which have recently underperformed compared to value stocks. Despite these challenges, companies with high insider ownership can offer unique advantages, as their leaders often have significant stakes in the business's success.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 23.8% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Medley (TSE:4480) | 34% | 27.2% |

| Pharma Mar (BME:PHM) | 11.9% | 56.2% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 110.9% |

| Findi (ASX:FND) | 34.8% | 112.9% |

We'll examine a selection from our screener results.

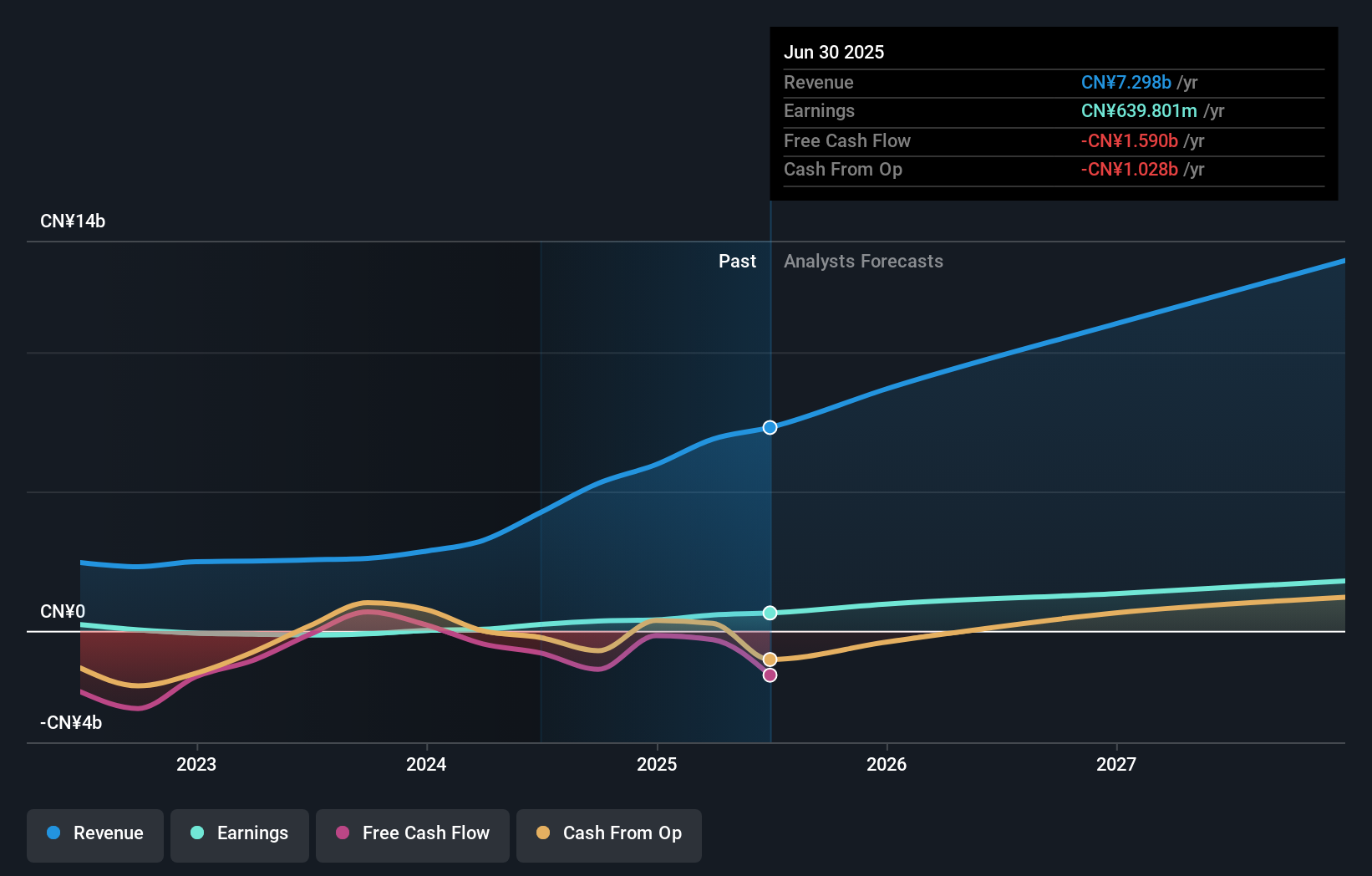

Smartsens Technology (Shanghai) (SHSE:688213)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Smartsens Technology (Shanghai) Co., Ltd. (SHSE:688213) operates in the semiconductor industry, focusing on the design and development of CMOS image sensors, with a market cap of CN¥29.26 billion.

Operations: The company generates revenue primarily from its Semiconductor Integrated Circuit Chips segment, amounting to CN¥5.29 billion.

Insider Ownership: 24.4%

Revenue Growth Forecast: 27.1% p.a.

Smartsens Technology (Shanghai) demonstrates strong growth potential with forecasted annual earnings growth of 48.39% and revenue growth of 27.1%, both outpacing the Chinese market averages. The company recently became profitable, reporting CNY 273.24 million in net income for the first nine months of 2024, a significant turnaround from a loss last year. Despite low return on equity projections and debt concerns, recent share buybacks suggest confidence in its future prospects.

- Get an in-depth perspective on Smartsens Technology (Shanghai)'s performance by reading our analyst estimates report here.

- The valuation report we've compiled suggests that Smartsens Technology (Shanghai)'s current price could be inflated.

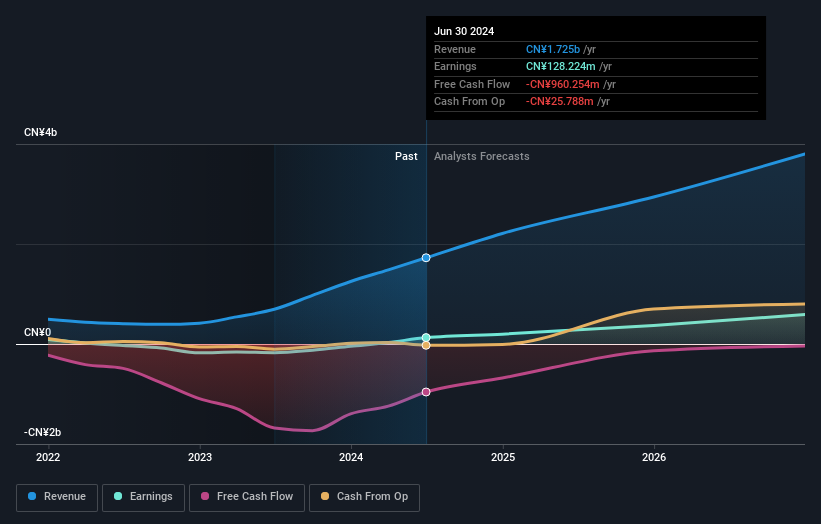

SICC (SHSE:688234)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SICC Co., Ltd. focuses on the research, development, production, and sale of silicon carbide semiconductor materials both in China and internationally, with a market cap of CN¥20.34 billion.

Operations: The company's revenue is primarily derived from its semiconductor material segment, totaling CN¥1.71 billion.

Insider Ownership: 30.2%

Revenue Growth Forecast: 23.4% p.a.

SICC Co., Ltd. showcases promising growth with revenue expected to increase 23.4% annually, surpassing the Chinese market average of 13.3%. The company turned profitable in 2024, reporting a net income of CNY 143.03 million for the first nine months, recovering from a loss last year. Earnings are projected to grow significantly at 32.24% per year, outpacing market expectations despite low future return on equity and no recent insider trading activity reported.

- Take a closer look at SICC's potential here in our earnings growth report.

- According our valuation report, there's an indication that SICC's share price might be on the expensive side.

Jiangsu Nata Opto-electronic Material (SZSE:300346)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jiangsu Nata Opto-electronic Material Co., Ltd. operates in the optoelectronic materials industry and has a market cap of CN¥20.75 billion.

Operations: The company generates revenue from its semiconductor materials segment, amounting to CN¥1.60 billion.

Insider Ownership: 18%

Revenue Growth Forecast: 21.8% p.a.

Jiangsu Nata Opto-electronic Material demonstrates robust growth potential, with revenue projected to grow 21.8% annually, outpacing the Chinese market average of 13.3%. For the first nine months of 2024, the company reported a net income of CNY 265.61 million on sales of CNY 1.76 billion, reflecting year-over-year improvements. Despite shareholder dilution and low future return on equity forecasts, earnings are expected to increase significantly at 24.55% per year without recent insider trading activity noted.

- Click here to discover the nuances of Jiangsu Nata Opto-electronic Material with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of Jiangsu Nata Opto-electronic Material shares in the market.

Where To Now?

- Reveal the 1442 hidden gems among our Fast Growing Companies With High Insider Ownership screener with a single click here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300346

Jiangsu Nata Opto-electronic Material

Jiangsu Nata Opto-electronic Material Co., Ltd.

Reasonable growth potential with adequate balance sheet.