- China

- /

- Medical Equipment

- /

- SHSE:688253

Innovita Biological Technology Co., Ltd.'s (SHSE:688253) Subdued P/E Might Signal An Opportunity

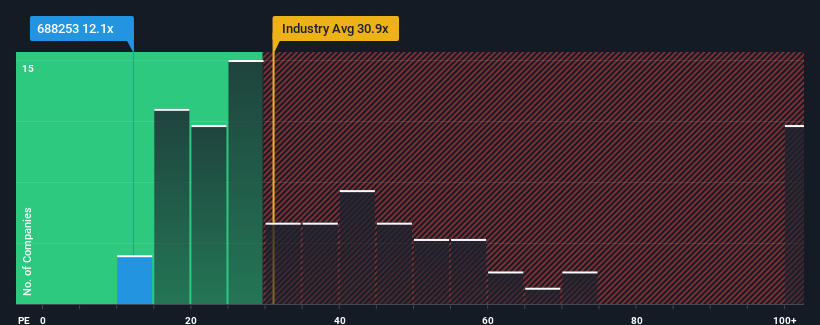

When close to half the companies in China have price-to-earnings ratios (or "P/E's") above 36x, you may consider Innovita Biological Technology Co., Ltd. (SHSE:688253) as a highly attractive investment with its 12.1x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Innovita Biological Technology has been doing quite well of late. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Innovita Biological Technology

Is There Any Growth For Innovita Biological Technology?

In order to justify its P/E ratio, Innovita Biological Technology would need to produce anemic growth that's substantially trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 180% last year. The strong recent performance means it was also able to grow EPS by 106% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the one analyst covering the company suggest earnings should grow by 50% over the next year. That's shaping up to be materially higher than the 38% growth forecast for the broader market.

With this information, we find it odd that Innovita Biological Technology is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Innovita Biological Technology currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Innovita Biological Technology with six simple checks.

You might be able to find a better investment than Innovita Biological Technology. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688253

Innovita Biological Technology

Engages in the research and development, manufacturing, marketing, and sales of POCT rapid diagnostic products.

Exceptional growth potential with flawless balance sheet.

Market Insights

Community Narratives