- China

- /

- Medical Equipment

- /

- SHSE:600529

There Is A Reason Shandong Pharmaceutical Glass Co.Ltd's (SHSE:600529) Price Is Undemanding

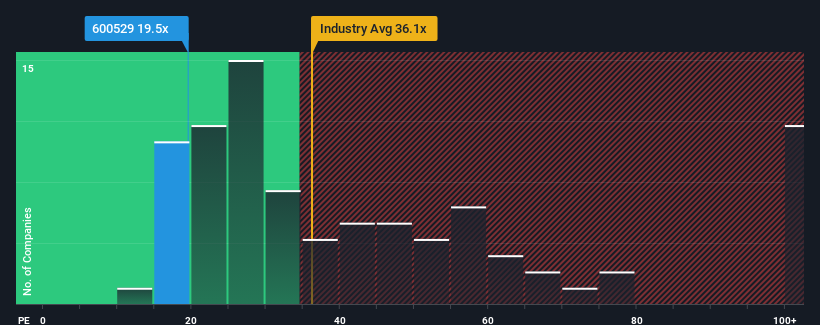

When close to half the companies in China have price-to-earnings ratios (or "P/E's") above 38x, you may consider Shandong Pharmaceutical Glass Co.Ltd (SHSE:600529) as an attractive investment with its 19.5x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Shandong Pharmaceutical GlassLtd certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for Shandong Pharmaceutical GlassLtd

Does Growth Match The Low P/E?

In order to justify its P/E ratio, Shandong Pharmaceutical GlassLtd would need to produce sluggish growth that's trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 18% last year. The latest three year period has also seen a 27% overall rise in EPS, aided extensively by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Shifting to the future, estimates from the eight analysts covering the company suggest earnings should grow by 27% over the next year. With the market predicted to deliver 38% growth , the company is positioned for a weaker earnings result.

With this information, we can see why Shandong Pharmaceutical GlassLtd is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Shandong Pharmaceutical GlassLtd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for Shandong Pharmaceutical GlassLtd with six simple checks.

Of course, you might also be able to find a better stock than Shandong Pharmaceutical GlassLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600529

Shandong Pharmaceutical GlassLtd

Manufactures and sells pharmaceutical glass packaging and butyl rubber series products in China.

Very undervalued with flawless balance sheet and pays a dividend.