- Philippines

- /

- Infrastructure

- /

- PSE:ICT

Top Growth Companies With Insider Ownership In October 2024

Reviewed by Simply Wall St

As global markets navigate a mix of economic signals, with the S&P 500 Index advancing and European Central Bank rate cuts stirring expectations, investors are keenly observing sectors like utilities and real estate for growth opportunities. In this environment, companies with high insider ownership often attract attention due to their potential alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 41.9% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| Arctech Solar Holding (SHSE:688408) | 37.8% | 29.8% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

Let's review some notable picks from our screened stocks.

International Container Terminal Services (PSE:ICT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Container Terminal Services, Inc. and its subsidiaries develop, manage, and operate container ports and terminals for the container shipping industry across Asia, Europe, the Middle East, Africa, and the Americas with a market capitalization of approximately ₱831.83 billion.

Operations: The company's revenue is primarily derived from Cargo Handling and Related Services, amounting to $2.55 billion.

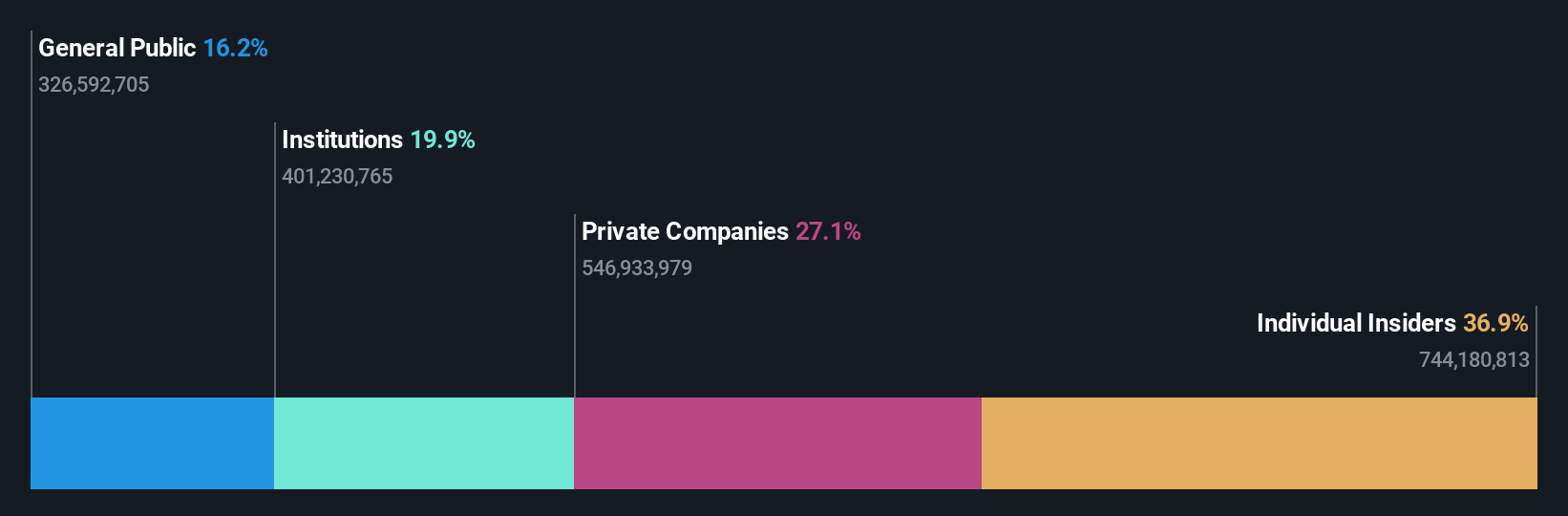

Insider Ownership: 36.6%

Earnings Growth Forecast: 15.4% p.a.

International Container Terminal Services is expanding with a US$800 million investment in Batangas, enhancing its role in global trade. Recent earnings showed notable growth, with Q2 revenue at US$714.11 million and net income at US$210.67 million. While insider buying has been minimal recently, the company's earnings are forecast to grow faster than the Philippine market, supported by a very high projected return on equity of 44.4% within three years despite high debt levels.

- Take a closer look at International Container Terminal Services' potential here in our earnings growth report.

- Our valuation report unveils the possibility International Container Terminal Services' shares may be trading at a premium.

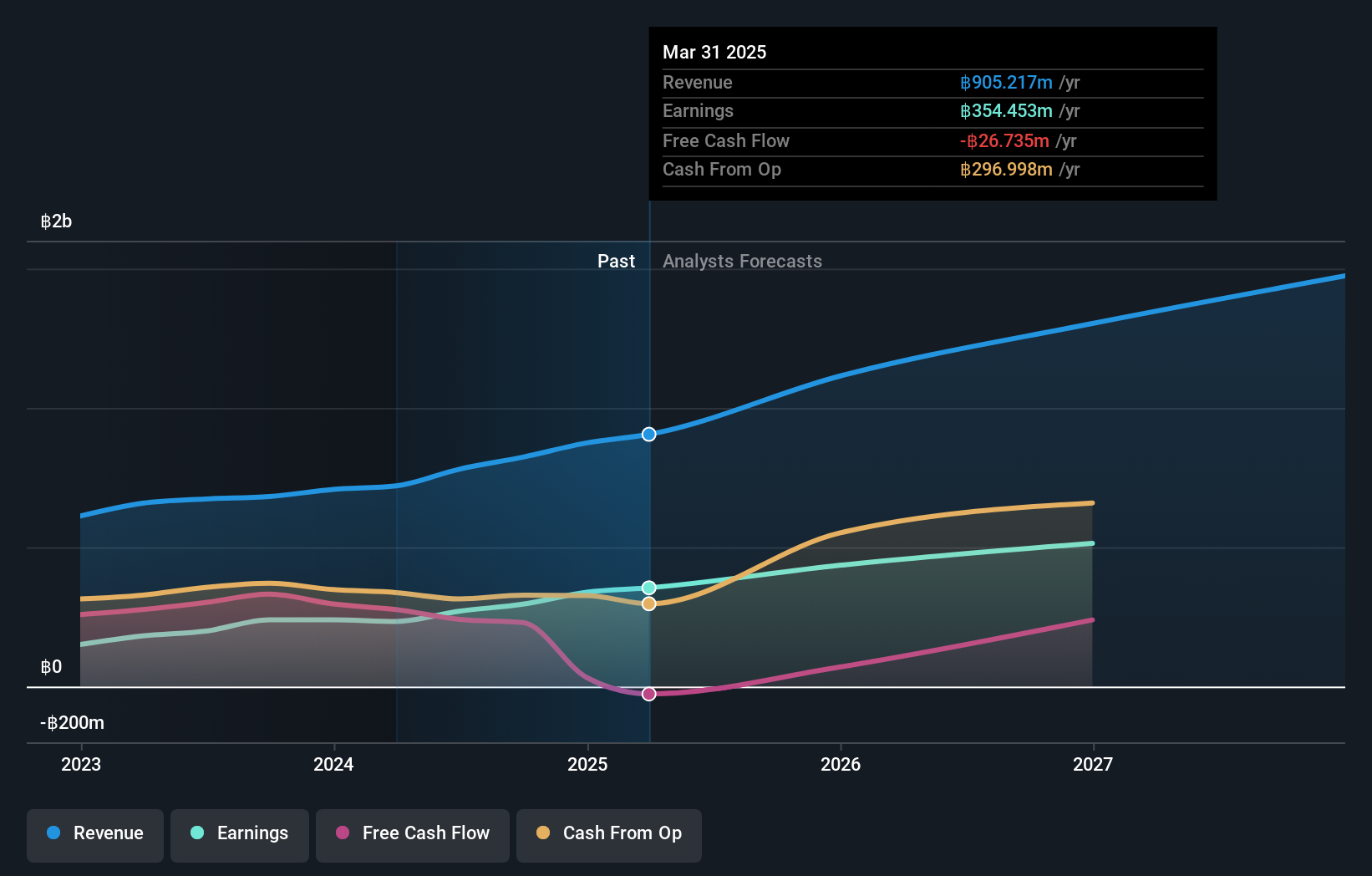

Medeze Group (SET:MEDEZE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Medeze Group Public Company Limited provides stem cell, NK cell, and follicle hair banking services in Thailand with a market cap of THB12.92 billion.

Operations: The company's revenue segments include THB135.49 million from Natural Killer Cells - Testing Services, THB416.22 million from Stem Cells Sample Collection Services - Placenta, THB70.82 million from Cord Blood collection, THB5.59 million from Hair Follicle collection, and THB139.76 million from Adipose Tissue collection services, along with THB10.59 million in product sales.

Insider Ownership: 26.1%

Earnings Growth Forecast: 25% p.a.

Medeze Group's recent IPO raised THB 2.41 billion, reflecting strong investor interest despite its shares being highly illiquid. The company's earnings are projected to grow significantly at 25% annually, outpacing the Thai market's growth rate of 14.8%. Recent financial results show robust growth with revenue increasing from THB 161.26 million to THB 221.7 million in Q2 year-over-year and net income rising from THB 50.25 million to THB 86.87 million, indicating solid performance momentum.

- Navigate through the intricacies of Medeze Group with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Medeze Group shares in the market.

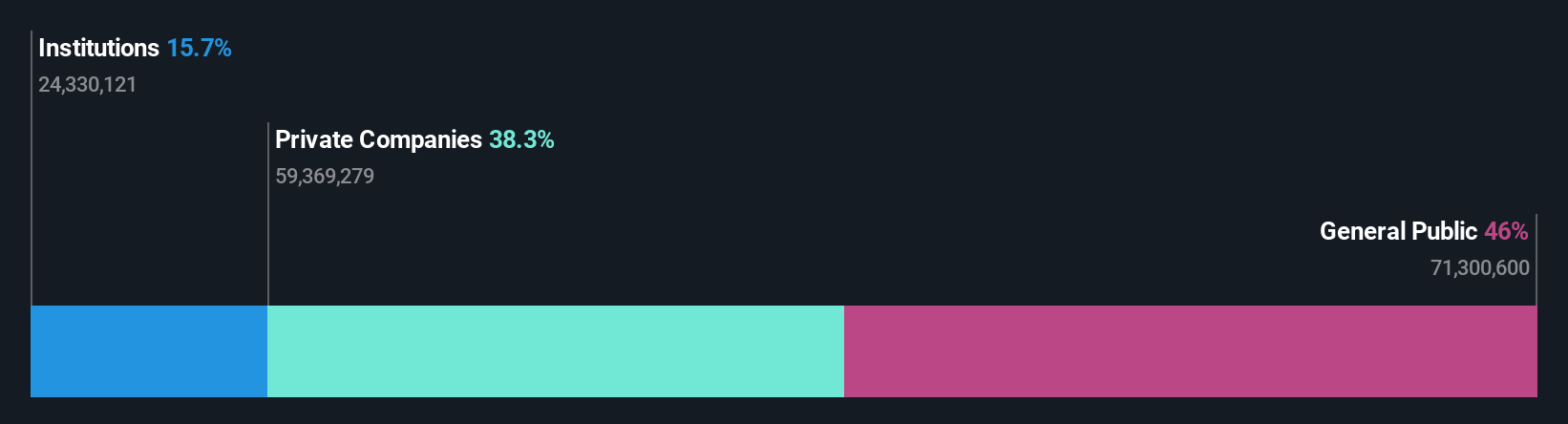

Western Regions Tourism DevelopmentLtd (SZSE:300859)

Simply Wall St Growth Rating: ★★★★★★

Overview: Western Regions Tourism Development Co., Ltd offers tourism and travel services in China with a market cap of CN¥5.75 billion.

Operations: The company generates revenue primarily from its tourism catering services, amounting to CN¥313.94 million.

Insider Ownership: 13.9%

Earnings Growth Forecast: 39.2% p.a.

Western Regions Tourism Development Ltd. demonstrates strong growth potential with forecasted earnings and revenue growth rates of 39.19% and 31.7% annually, respectively, both surpassing market averages. Despite an unstable dividend history and recent volatility in share price, the company shows resilience with a significant past earnings increase of 148.5%. Recent half-year results indicate modest sales growth to CNY 100.03 million, though net income slightly declined to CNY 29.37 million year-over-year.

- Click here to discover the nuances of Western Regions Tourism DevelopmentLtd with our detailed analytical future growth report.

- The valuation report we've compiled suggests that Western Regions Tourism DevelopmentLtd's current price could be inflated.

Where To Now?

- Access the full spectrum of 1484 Fast Growing Companies With High Insider Ownership by clicking on this link.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About PSE:ICT

International Container Terminal Services

Develops, manages, and operates container ports and terminals for container shipping industry and cargo owners in Asia, Europe, the Middle East, Africa, and the Americas.

Reasonable growth potential average dividend payer.