Advertisement

- China

- /

- Electrical

- /

- SZSE:301121

Chongqing VDL Electronics Co., Ltd. (SZSE:301121) Stock Rockets 31% As Investors Are Less Pessimistic Than Expected

The Chongqing VDL Electronics Co., Ltd. (SZSE:301121) share price has done very well over the last month, posting an excellent gain of 31%. The annual gain comes to 134% following the latest surge, making investors sit up and take notice.

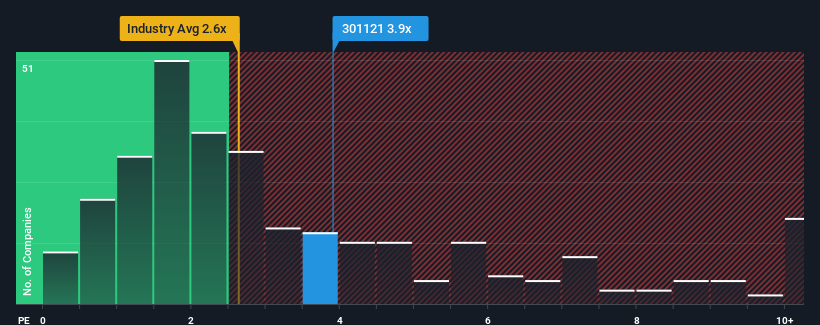

After such a large jump in price, given close to half the companies operating in China's Electrical industry have price-to-sales ratios (or "P/S") below 2.6x, you may consider Chongqing VDL Electronics as a stock to potentially avoid with its 3.9x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

View our latest analysis for Chongqing VDL Electronics

How Chongqing VDL Electronics Has Been Performing

The revenue growth achieved at Chongqing VDL Electronics over the last year would be more than acceptable for most companies. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for Chongqing VDL Electronics, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Chongqing VDL Electronics' Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Chongqing VDL Electronics' to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 24% last year. Pleasingly, revenue has also lifted 42% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 25% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in mind, we find it worrying that Chongqing VDL Electronics' P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

What We Can Learn From Chongqing VDL Electronics' P/S?

Chongqing VDL Electronics shares have taken a big step in a northerly direction, but its P/S is elevated as a result. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

The fact that Chongqing VDL Electronics currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

It is also worth noting that we have found 3 warning signs for Chongqing VDL Electronics (1 doesn't sit too well with us!) that you need to take into consideration.

If these risks are making you reconsider your opinion on Chongqing VDL Electronics, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301121

Chongqing VDL Electronics

Engages research and development, design, production, and sale of consumer rechargeable lithium-ion battery products in China.

Excellent balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|56.1% undervalued

AX

Community Contributor