November 2024's Top Growth Companies With Strong Insider Confidence

Reviewed by Simply Wall St

In a week marked by a flurry of earnings reports and economic data, global markets experienced volatility, with major indices like the Nasdaq Composite and S&P MidCap 400 reaching record highs before retreating. Amidst this backdrop, growth stocks have generally underperformed compared to value shares, highlighting the importance of insider confidence as a potential indicator of resilience in uncertain times. Companies with high insider ownership may signal strong belief in their long-term prospects, making them noteworthy considerations for investors navigating today's complex market environment.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Laopu Gold (SEHK:6181) | 36.4% | 33% |

| Medley (TSE:4480) | 34% | 30.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Let's take a closer look at a couple of our picks from the screened companies.

Bittium Oyj (HLSE:BITTI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bittium Oyj offers communications and connectivity solutions, healthcare technology products and services, and biosignal measuring and monitoring in Finland, Germany, and the United States with a market cap of €250.53 million.

Operations: Bittium Oyj generates revenue through its offerings in communications and connectivity solutions, healthcare technology products and services, and biosignal measuring and monitoring across Finland, Germany, and the United States.

Insider Ownership: 12.6%

Earnings Growth Forecast: 40.9% p.a.

Bittium Oyj has shown a turnaround in profitability, reporting a net income of EUR 1.7 million for the first nine months of 2024, compared to a loss last year. The company expects significant earnings growth at 40.9% annually, outpacing the Finnish market's average. Despite its volatile share price, Bittium's revenue is forecasted to grow faster than the market rate at 12.5% per year, with insider ownership potentially aligning management interests with shareholders'.

- Click here to discover the nuances of Bittium Oyj with our detailed analytical future growth report.

- According our valuation report, there's an indication that Bittium Oyj's share price might be on the expensive side.

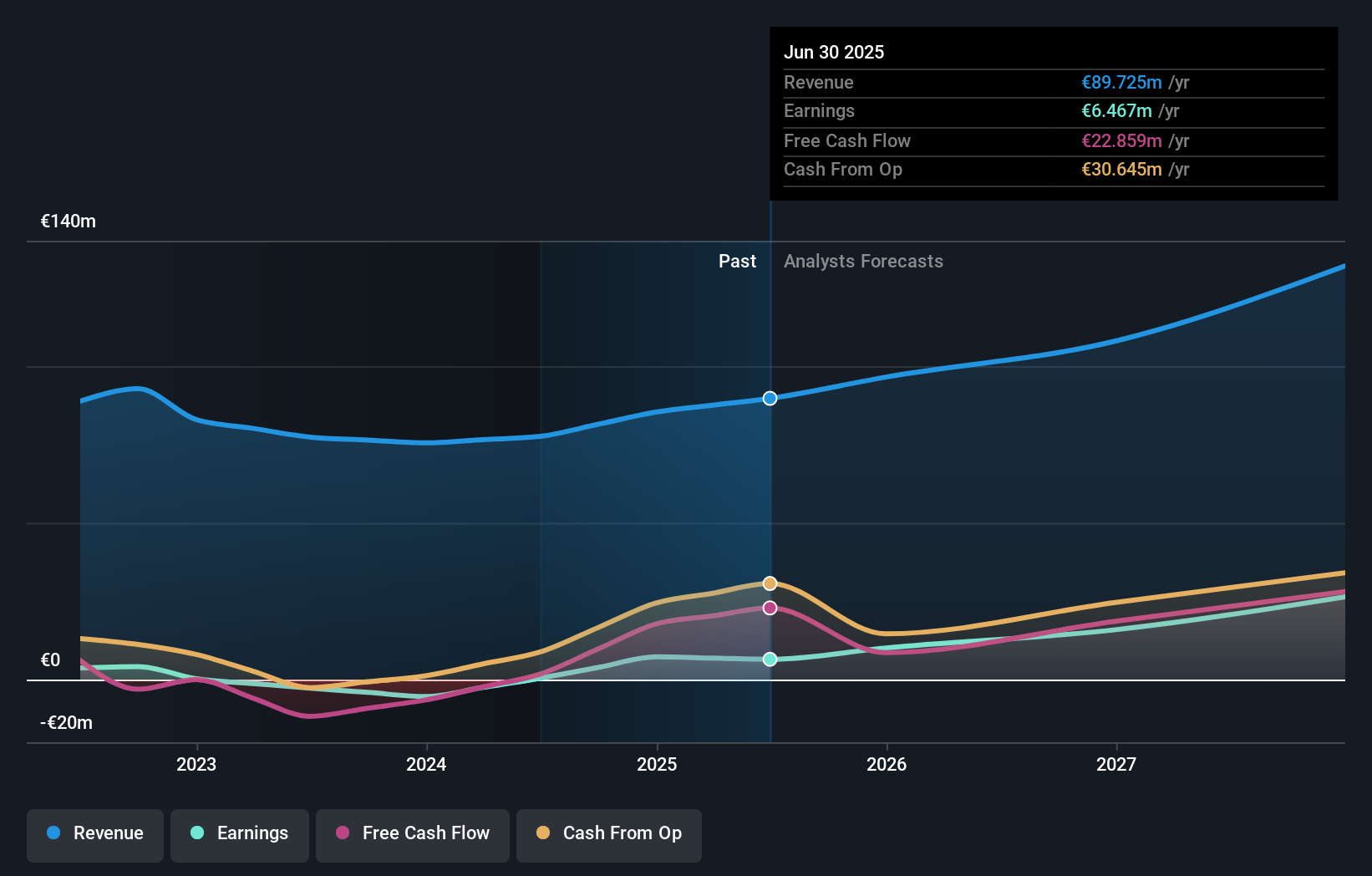

Dongyue Group (SEHK:189)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dongyue Group Limited is an investment holding company that operates in the manufacturing, distribution, and sale of polymers, organic silicone, refrigerants, dichloromethane, PVC, liquid alkali, and other products both in the People's Republic of China and internationally; it has a market capitalization of approximately HK$11.45 billion.

Operations: The company's revenue segments consist of CN¥4.31 billion from polymers, CN¥5.53 billion from refrigerants, CN¥5.12 billion from organic silicon, and CN¥1.12 billion from dichloromethane PVC and liquid alkali.

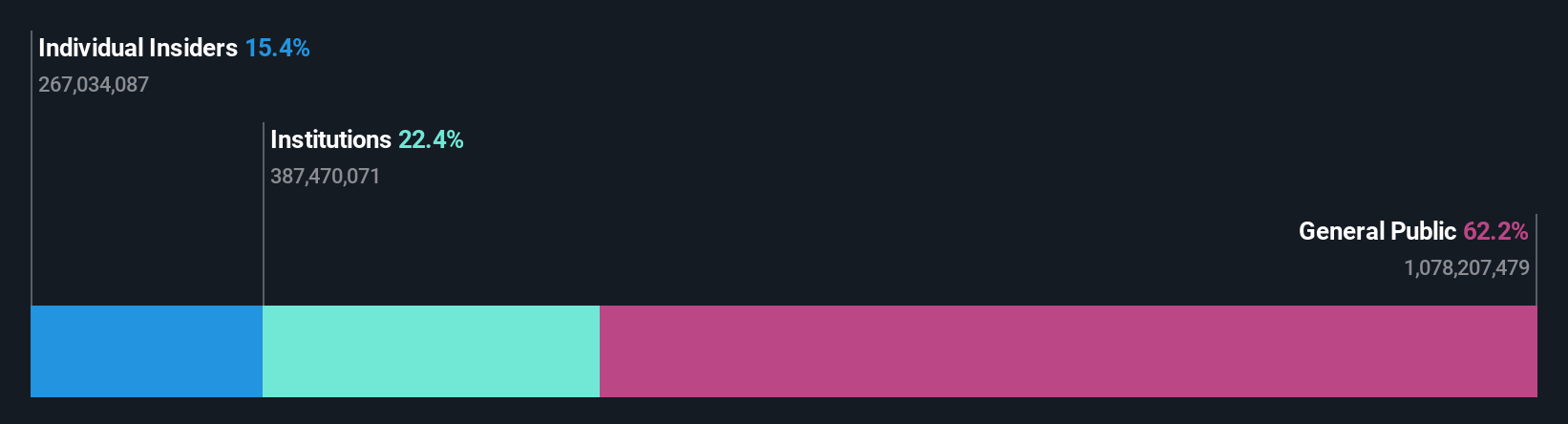

Insider Ownership: 15.4%

Earnings Growth Forecast: 42.6% p.a.

Dongyue Group's revenue is projected to grow at 10.5% annually, surpassing the Hong Kong market average of 7.7%. Earnings are expected to increase significantly at 42.6% per year, although profit margins have declined from last year. Recent financial results show a modest rise in net income and earnings per share for the first half of 2024. Despite an auditor change, the company maintains audit quality without impacting its financial statement preparation.

- Dive into the specifics of Dongyue Group here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Dongyue Group is trading beyond its estimated value.

Tongyu Heavy Industry (SZSE:300185)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Tongyu Heavy Industry Co., Ltd. specializes in the research, development, manufacture, and sale of forgings and castings, with a market cap of CN¥11.30 billion.

Operations: The company's revenue primarily comes from General Equipment Manufacturing, amounting to CN¥5.14 billion.

Insider Ownership: 10.1%

Earnings Growth Forecast: 104.2% p.a.

Tongyu Heavy Industry's revenue is forecast to grow at 23% annually, outpacing the Chinese market average of 14%, with earnings projected to increase significantly by over 100% per year. Despite this growth potential, recent financial results show a decline in both revenue and net income compared to last year. The company's shares are highly volatile and trade at a substantial discount to estimated fair value, while interest payments remain poorly covered by earnings.

- Click to explore a detailed breakdown of our findings in Tongyu Heavy Industry's earnings growth report.

- Insights from our recent valuation report point to the potential undervaluation of Tongyu Heavy Industry shares in the market.

Key Takeaways

- Discover the full array of 1534 Fast Growing Companies With High Insider Ownership right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Bittium Oyj, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Bittium Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About HLSE:BITTI

Bittium Oyj

Provides solutions for communications and connectivity, healthcare technology products and services, and biosignal measuring and monitoring in Finland, Germany, and the United States.

Flawless balance sheet with moderate growth potential.