- China

- /

- Electrical

- /

- SZSE:300048

What You Can Learn From Hiconics Eco-energy Technology Co., Ltd.'s (SZSE:300048) P/S

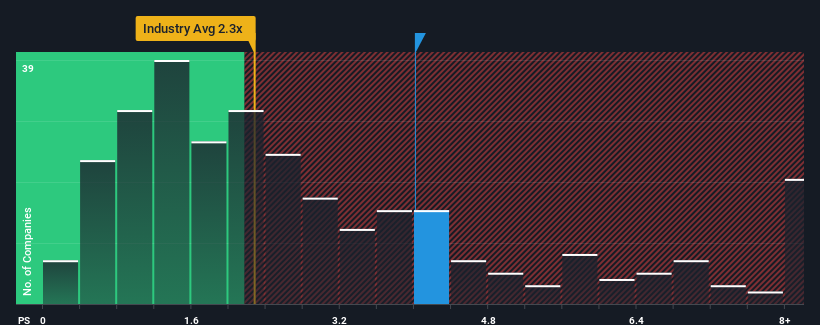

When you see that almost half of the companies in the Electrical industry in China have price-to-sales ratios (or "P/S") below 2.3x, Hiconics Eco-energy Technology Co., Ltd. (SZSE:300048) looks to be giving off some sell signals with its 4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Hiconics Eco-energy Technology

How Has Hiconics Eco-energy Technology Performed Recently?

Recent times haven't been great for Hiconics Eco-energy Technology as its revenue has been rising slower than most other companies. It might be that many expect the uninspiring revenue performance to recover significantly, which has kept the P/S ratio from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Hiconics Eco-energy Technology's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

Hiconics Eco-energy Technology's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 15% last year. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 96% over the next year. That's shaping up to be materially higher than the 23% growth forecast for the broader industry.

With this in mind, it's not hard to understand why Hiconics Eco-energy Technology's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Hiconics Eco-energy Technology maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Electrical industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Hiconics Eco-energy Technology with six simple checks.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Hiconics Eco-energy Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300048

Hiconics Eco-energy Technology

Engages in the industrial control, residential energy storage, and distributed PV EPC businesses in China and internationally.

Flawless balance sheet with high growth potential.