- Hong Kong

- /

- Real Estate

- /

- SEHK:1821

3 Asian Stocks With High Insider Ownership And 85% Earnings Growth

Reviewed by Simply Wall St

As global markets grapple with trade policy uncertainties and inflation concerns, the Asian market remains a focal point for investors seeking growth opportunities. In this environment, stocks with high insider ownership and strong earnings growth potential stand out as attractive options, offering a combination of alignment between management and shareholders alongside robust financial performance.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Quick Intelligent EquipmentLtd (SHSE:603203) | 34.2% | 35.6% |

| Laopu Gold (SEHK:6181) | 36.4% | 43.7% |

| PharmaResearch (KOSDAQ:A214450) | 38.6% | 26.4% |

| Global Tax Free (KOSDAQ:A204620) | 20.4% | 89.3% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 125.9% |

| Fulin Precision (SZSE:300432) | 13.6% | 78.6% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 60.9% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

Here's a peek at a few of the choices from the screener.

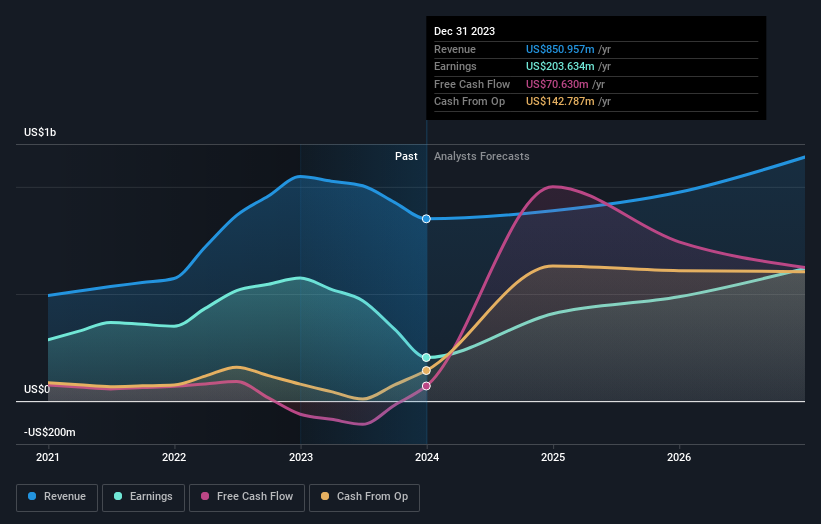

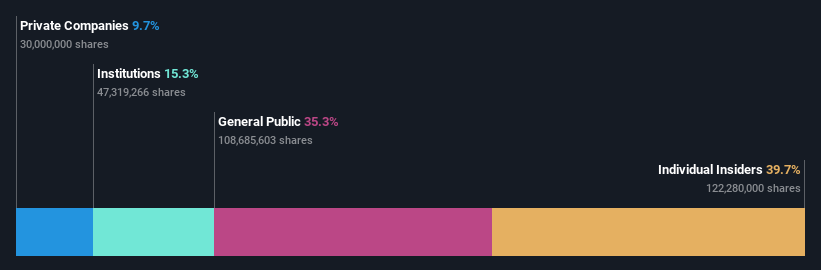

ESR Group (SEHK:1821)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ESR Group Limited operates in logistics real estate development, leasing, and management across various regions including Hong Kong, China, Japan, South Korea, Australia, New Zealand, Southeast Asia, India, Europe and internationally with a market cap of approximately HK$52.73 billion.

Operations: The company's revenue segments include Fund Management at $627.98 million and New Economy Development at $113.33 million, while the Investment segment shows a negative revenue of -$106.44 million.

Insider Ownership: 13%

Earnings Growth Forecast: 85.9% p.a.

ESR Group is positioned for substantial growth in Asia, with earnings forecasted to grow 85.9% annually and expected revenue growth of 15.8%, outpacing the Hong Kong market average. Despite trading at 20.4% below its estimated fair value, concerns arise from interest payments not being well covered by earnings and a low return on equity forecast of 5.1%. Recent board changes include Mr. Lim's retirement and Mr. McDonald's expanded role in the Nomination Committee, indicating active governance adjustments.

- Click here and access our complete growth analysis report to understand the dynamics of ESR Group.

- Insights from our recent valuation report point to the potential overvaluation of ESR Group shares in the market.

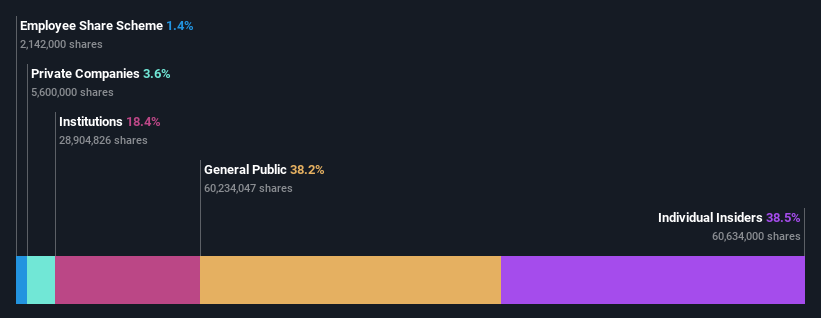

Wencan Group (SHSE:603348)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Wencan Group Co., Ltd. specializes in the R&D, production, and sale of automotive aluminum alloy precision die castings both in China and internationally, with a market cap of CN¥8.31 billion.

Operations: Wencan Group Co., Ltd. generates its revenue through the research, development, production, and sale of automotive aluminum alloy precision die castings in both domestic and international markets.

Insider Ownership: 38.4%

Earnings Growth Forecast: 65.6% p.a.

Wencan Group is positioned for growth in Asia, with earnings expected to grow significantly at 65.6% annually, outpacing the Chinese market average. Despite trading 74.2% below its estimated fair value, concerns include a low return on equity forecast of 10.3% and past shareholder dilution. Revenue growth is projected at 17.7%, exceeding the market's average but below high-growth benchmarks. The dividend yield of 1.14% is not well-covered by free cash flows, reflecting potential financial constraints.

- Click to explore a detailed breakdown of our findings in Wencan Group's earnings growth report.

- In light of our recent valuation report, it seems possible that Wencan Group is trading beyond its estimated value.

Suzhou Recodeal Interconnect SystemLtd (SHSE:688800)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Suzhou Recodeal Interconnect System Co., Ltd is engaged in the development, production, and sale of connection systems and microwave components globally, with a market cap of CN¥9.14 billion.

Operations: Revenue segments for Suzhou Recodeal Interconnect System Co., Ltd include the development, production, and sale of connection systems and microwave components on a global scale.

Insider Ownership: 38.5%

Earnings Growth Forecast: 29.9% p.a.

Suzhou Recodeal Interconnect System Ltd demonstrates strong growth potential, with earnings projected to increase significantly at 29.9% annually, surpassing the Chinese market average. Recent earnings results show a notable rise in sales to CNY 2.41 billion and net income to CNY 172.94 million for 2024. However, the company's return on equity is forecasted to be modest at 12.7%, and its share price has been highly volatile recently, which may pose risks for investors seeking stability.

- Unlock comprehensive insights into our analysis of Suzhou Recodeal Interconnect SystemLtd stock in this growth report.

- Our expertly prepared valuation report Suzhou Recodeal Interconnect SystemLtd implies its share price may be too high.

Key Takeaways

- Gain an insight into the universe of 635 Fast Growing Asian Companies With High Insider Ownership by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade ESR Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if ESR Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1821

ESR Group

Engages in the logistics real estate development, leasing, and management activities in Hong Kong, China, Japan, South Korea, Australia, New Zealand, Southeast Asia, India, Europe, and internationally.

Reasonable growth potential and slightly overvalued.

Market Insights

Community Narratives