- Switzerland

- /

- Basic Materials

- /

- SWX:AMRZ

Assessing Amrize (SWX:AMRZ) Valuation Following the Recent Surge in Investor Interest

Reviewed by Simply Wall St

Price-to-Earnings of 25.6x: Is it justified?

Based on the current price-to-earnings (P/E) ratio, Amrize is trading at 25.6 times its earnings. This is higher than both its peer average of 24.2 and the European Basic Materials industry average of 15.2. This suggests that the market is placing a premium on Amrize relative to its sector.

The P/E ratio is a commonly used measure to assess whether a company's shares are over or undervalued compared to earnings. A higher ratio can be justified if investors expect greater profit growth or superior quality of earnings relative to competitors. For Amrize, this may reflect optimism about the company’s future prospects or a belief in the quality of its recent results.

Paying a premium on earnings means that the market is already pricing in positive expectations for Amrize, perhaps due to its growth rates or improvements in profitability. However, with earnings growth only moderately higher than peers, the justification for such a high multiple may be open to debate.

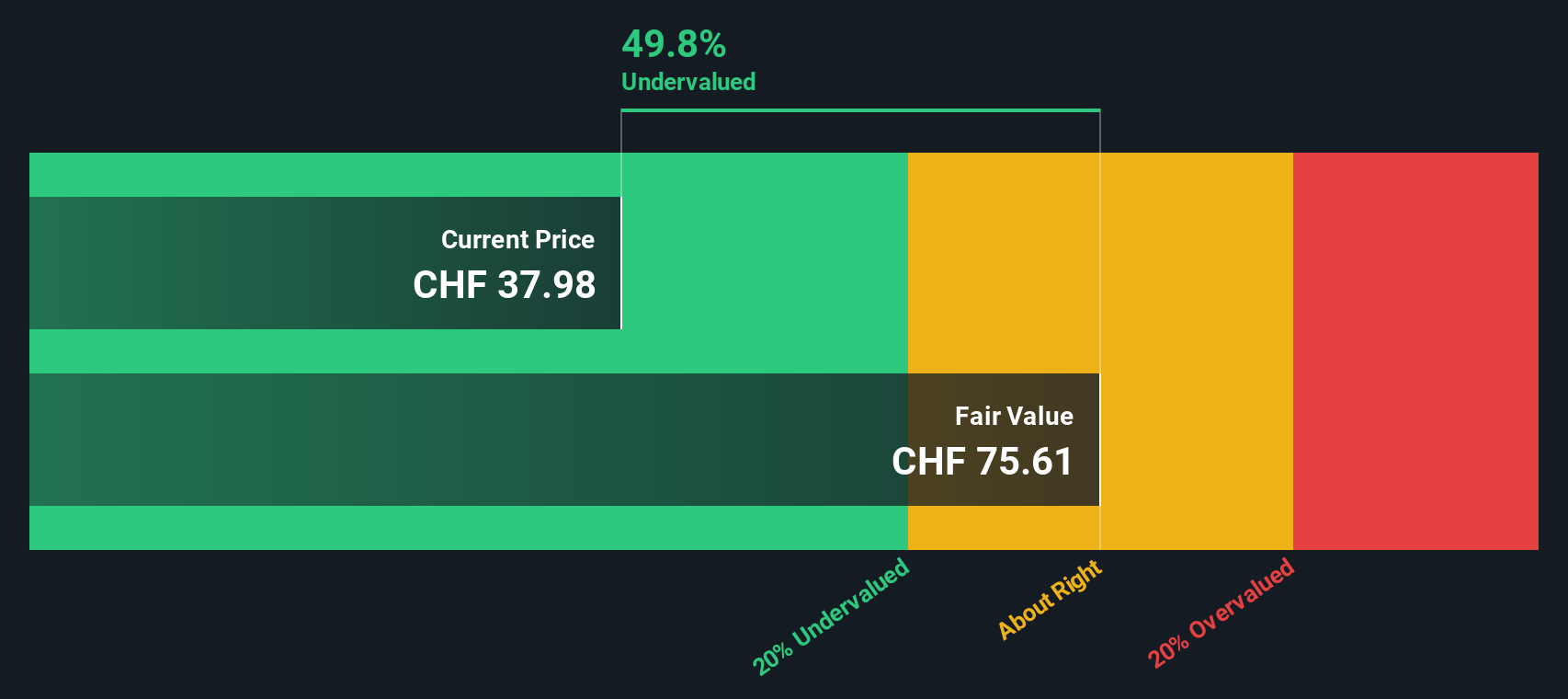

Result: Fair Value of $43.52 (OVERVALUED)

See our latest analysis for Amrize.However, slower-than-expected revenue growth or a reversal in earnings momentum could quickly dampen the current optimism surrounding Amrize’s valuation.

Find out about the key risks to this Amrize narrative.Another View: Discounted Cash Flow Model Tells a Different Story

While the earlier approach suggests Amrize is trading at a premium based on its earnings, our DCF model paints a much more optimistic picture and points to significant undervaluation. How can these methods be so far apart?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Amrize Narrative

If you have a different perspective or want to investigate the numbers on your own, you can develop your own narrative in just a few minutes. Do it your way

A great starting point for your Amrize research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Make your next move count with Simply Wall Street’s tailored screeners. These opportunities can set your portfolio apart and connect you with tomorrow’s market leaders.

- Unlock value by targeting companies trading below their potential using our tool for undervalued stocks based on cash flows and set yourself up for smart buy opportunities.

- Seek powerful long-term income by scanning stocks that deliver strong yields. Check out our gateway to dividend stocks with yields > 3% for steady returns.

- Stay ahead of the technological curve by following the newest breakthroughs. Our resource for AI penny stocks can spotlight emerging leaders in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About SWX:AMRZ

Amrize

Engages in the provision of various building solutions for infrastructure, commercial, and residential construction markets in North America.

Proven track record with adequate balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Cheap if able to sustain revenue, and a potential bargain if able to turn store openings into revenue growth

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)