Advertisement

- Canada

- /

- Renewable Energy

- /

- TSX:BEPC

Brookfield Renewable (TSE:BEPC) Posted Weak Earnings But There Is More To Worry About

Brookfield Renewable Corporation's (TSE:BEPC) weak earnings were disregarded by the market. While shares were up, we believe there are some factors in the earnings report that might cause investors some concerns.

See our latest analysis for Brookfield Renewable

The Power Of Non-Operating Revenue

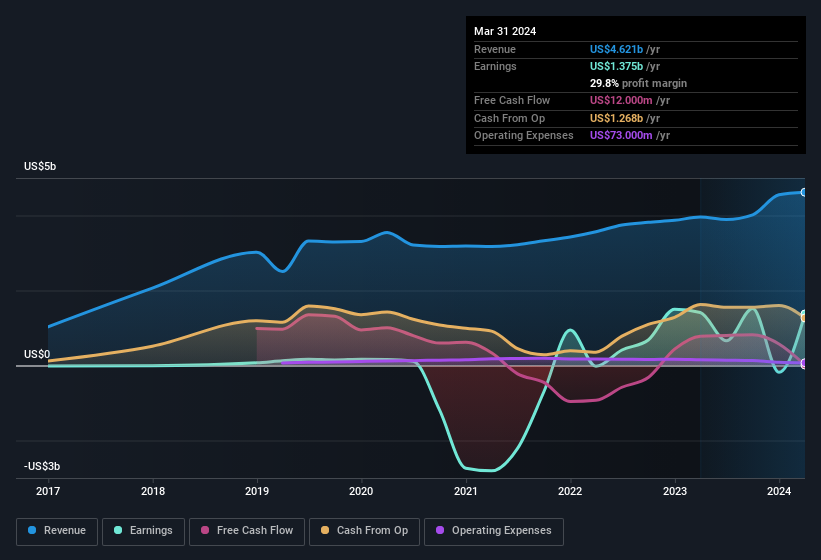

Most companies divide classify their revenue as either 'operating revenue', which comes from normal operations, and other revenue, which could include government grants, for example. Oftentimes, non-operating revenue spikes are not repeated, so it makes sense to be cautious where non-operating revenue has made a very large contribution to total profit. However, we note that when non-operating revenue increases suddenly, it will sometimes generate an unsustainable boost to profit. Notably, Brookfield Renewable had a significant increase in non-operating revenue over the last year. In fact, our data indicates that non-operating revenue increased from US$42.0m to US$595.0m. The high levels of non-operating revenue are problematic because if (and when) they do not repeat, then overall revenue (and profitability) of the firm will fall. In order to better understand a company's profit result, it can sometimes help to consider whether the result would be very different without a sudden increase in non-operating revenue.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

How Do Unusual Items Influence Profit?

As well as that spike in non-operating revenue, we should also consider the US$1.5b boost to profit coming from unusual items, over the last year. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. Brookfield Renewable had a rather significant contribution from unusual items relative to its profit to March 2024. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On Brookfield Renewable's Profit Performance

In the last year Brookfield Renewable's non-operating revenue really gave it a boost, but not in a way that is necessarily going to be sustained. And on top of that, it also saw an unusual item boost its profit, suggesting that next year might see a lower profit number, if these events are not repeated and everything else is equal. For all the reasons mentioned above, we think that, at a glance, Brookfield Renewable's statutory profits could be considered to be low quality, because they are likely to give investors an overly positive impression of the company. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Be aware that Brookfield Renewable is showing 5 warning signs in our investment analysis and 2 of those shouldn't be ignored...

Our examination of Brookfield Renewable has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Brookfield Renewable might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:BEPC

Brookfield Renewable

Owns and operates a portfolio of renewable power and sustainable solution assets.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor