Advertisement

Is It Time To Reassess Constellation Software (TSX:CSU) After A 49% Share Price Slide?

Reviewed by Bailey Pemberton

Before looking at models and ratios, the key question is whether Constellation Software's current share price still reflects its quality or if recent weakness has created a potential opportunity for you.

Over the last year, the stock has fallen 49.5%, with a 29.1% decline year to date, including 15.0% over the past month and 6.0% over the last week. This may signal shifting expectations and a different balance between risk and potential reward than many investors were pricing in previously.

Recent news coverage has focused on Constellation Software's role as a major acquirer in the software sector and its continued emphasis on capital allocation and portfolio management. This gives context to why investors pay close attention to changes in sentiment. Headlines around acquisition activity, integration execution and how management prioritizes cash use often sit in the background of price moves like those seen in recent months.

On Simply Wall St's valuation checks, Constellation Software currently records a 3 out of 6 value score. The next step is to unpack what different valuation approaches say about that score and then look at an even more helpful way to interpret valuation at the end of this article.

Find out why Constellation Software's -49.5% return over the last year is lagging behind its peers.

Approach 1: Constellation Software Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth today by projecting future cash flows and discounting them back to the present using a required rate of return.

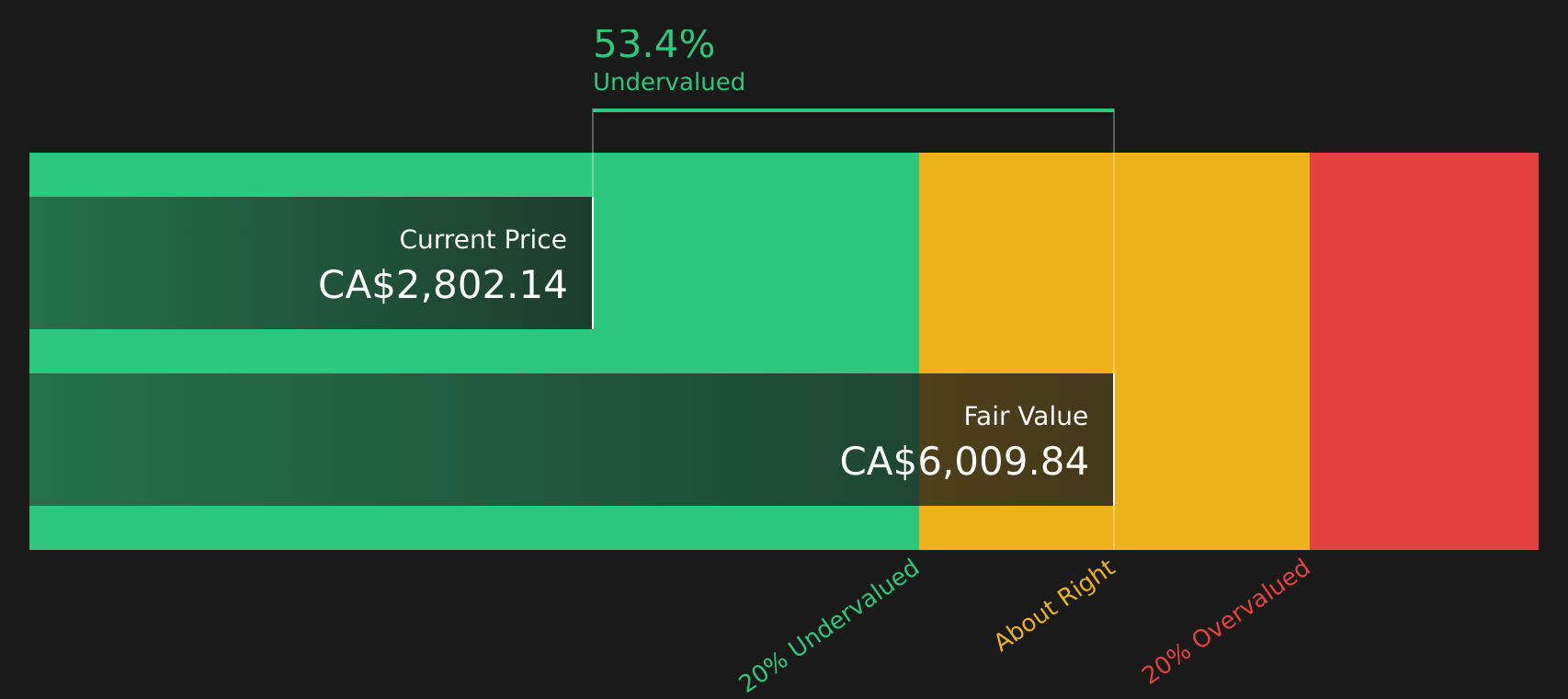

For Constellation Software, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow (FCF) is $2.66b. Analysts provide explicit forecasts out to 2027, with FCF for that year projected at $3.57b. Simply Wall St then extrapolates cash flows further out to 2035 using its own growth assumptions.

Over the next decade, the model includes a series of annual FCF projections in the billions of dollars, each discounted back to today. Adding these discounted cash flows together and including a terminal value results in an estimated intrinsic value of $5,374.87 per share.

Against the current share price, this implies a 57.3% discount, which points to Constellation Software trading well below this DCF estimate of fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Constellation Software is undervalued by 57.3%. Track this in your watchlist or portfolio, or discover 7 more high quality undervalued stocks.

Approach 2: Constellation Software Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you pay for each share to the earnings that support that price. It gives you a quick sense of how much the market is paying for each dollar of profit.

What counts as a "normal" P/E depends on how the market views a company’s growth prospects and risk. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk tends to point to a lower one.

Constellation Software currently trades on a P/E of 68.70x. That is above both the Software industry average of 23.01x and the peer average of 54.37x. Simply Wall St’s Fair Ratio for Constellation Software is 34.94x, which is its proprietary estimate of what the P/E might be given factors such as earnings growth, industry, profit margin, market cap and risk profile.

This Fair Ratio can be more helpful than a simple peer or industry comparison because it adjusts for company specific characteristics instead of assuming that all software stocks deserve similar multiples.

Comparing the current 68.70x P/E with the 34.94x Fair Ratio points to Constellation Software trading above this Fair Ratio estimate.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 2 top founder-led companies.

Upgrade Your Decision Making: Choose your Constellation Software Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives are introduced here as your way to attach a clear story about Constellation Software to specific assumptions on future revenue, earnings and margins, link that story to a forecast and Fair Value, and then compare that Fair Value with the current price inside Simply Wall St's Community page. Narratives are updated when new news or earnings arrive. One investor might build a bullish CSU view around a Fair Value near CA$5,325.57 and another might anchor a more cautious view near CA$3,477.92, and both sets of numbers sit side by side so you can quickly see which story, and which Fair Value versus Price relationship, feels closer to your own view before deciding what action, if any, makes sense for you.

Do you think there's more to the story for Constellation Software? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CSU

Constellation Software

Acquires, builds, and manages vertical market software businesses to develop mission-critical software solutions for public and private sector markets.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.563.5% undervalued

54 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.826.3% undervalued

22 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

16 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.6% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Aftermath Silver ·

Aftermath Silver, A 35% Insider-Aligned Silver Stock With a Giant Critical Metals Twist

Fair Value:CA$30.3797.8% undervalued

6 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

ES

Esteban on NVR ·

NVR 05-2026

Fair Value:US$3.76k72.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Capricor Therapeutics ·

The Exosome Pioneer: Why Capricor (CAPR) is Poised for an August FDA Breakthrough

Fair Value:US$5862.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.8% undervalued

87 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5448.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

16 likesusers have liked this narrative