- Canada

- /

- Metals and Mining

- /

- TSX:OLA

3 TSX Growth Companies With High Insider Ownership Growing Earnings At 81%

Reviewed by Simply Wall St

The Canadian market has shown resilience, bolstered by easing monetary policies and strong household spending, which have supported economic growth and corporate profits. In this environment, companies with high insider ownership often signal confidence from those closest to the business, making them intriguing candidates for investors seeking growth opportunities.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Propel Holdings (TSX:PRL) | 36.9% | 37.6% |

| Allied Gold (TSX:AAUC) | 17.7% | 85% |

| Almonty Industries (TSX:AII) | 17.7% | 60.7% |

| Enterprise Group (TSX:E) | 39.8% | 50.7% |

| VersaBank (TSX:VBNK) | 13.3% | 30.4% |

| Aya Gold & Silver (TSX:AYA) | 10.2% | 94.3% |

| Ivanhoe Mines (TSX:IVN) | 12.5% | 43.2% |

| Aritzia (TSX:ATZ) | 18.9% | 59.7% |

| Profound Medical (TSX:PRN) | 12.2% | 57.4% |

| CHAR Technologies (TSXV:YES) | 10.7% | 58.3% |

We're going to check out a few of the best picks from our screener tool.

North American Construction Group (TSX:NOA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: North American Construction Group Ltd. offers mining and heavy civil construction services to the resource development and industrial construction sectors in Australia, Canada, and the United States, with a market cap of CA$753.84 million.

Operations: North American Construction Group Ltd. generates revenue through its mining and heavy civil construction services provided to the resource development and industrial construction sectors across Australia, Canada, and the United States.

Insider Ownership: 11.6%

Earnings Growth Forecast: 36.4% p.a.

North American Construction Group demonstrates substantial insider ownership, with insiders buying more shares than selling recently. Despite the company's high debt level, its earnings are expected to grow significantly at 36.4% per year over the next three years, outpacing the Canadian market average of 16%. Recent financial results show a rise in quarterly sales to C$286.86 million but a decline in profit margins from 8.2% to 4.8%.

- Dive into the specifics of North American Construction Group here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that North American Construction Group is priced lower than what may be justified by its financials.

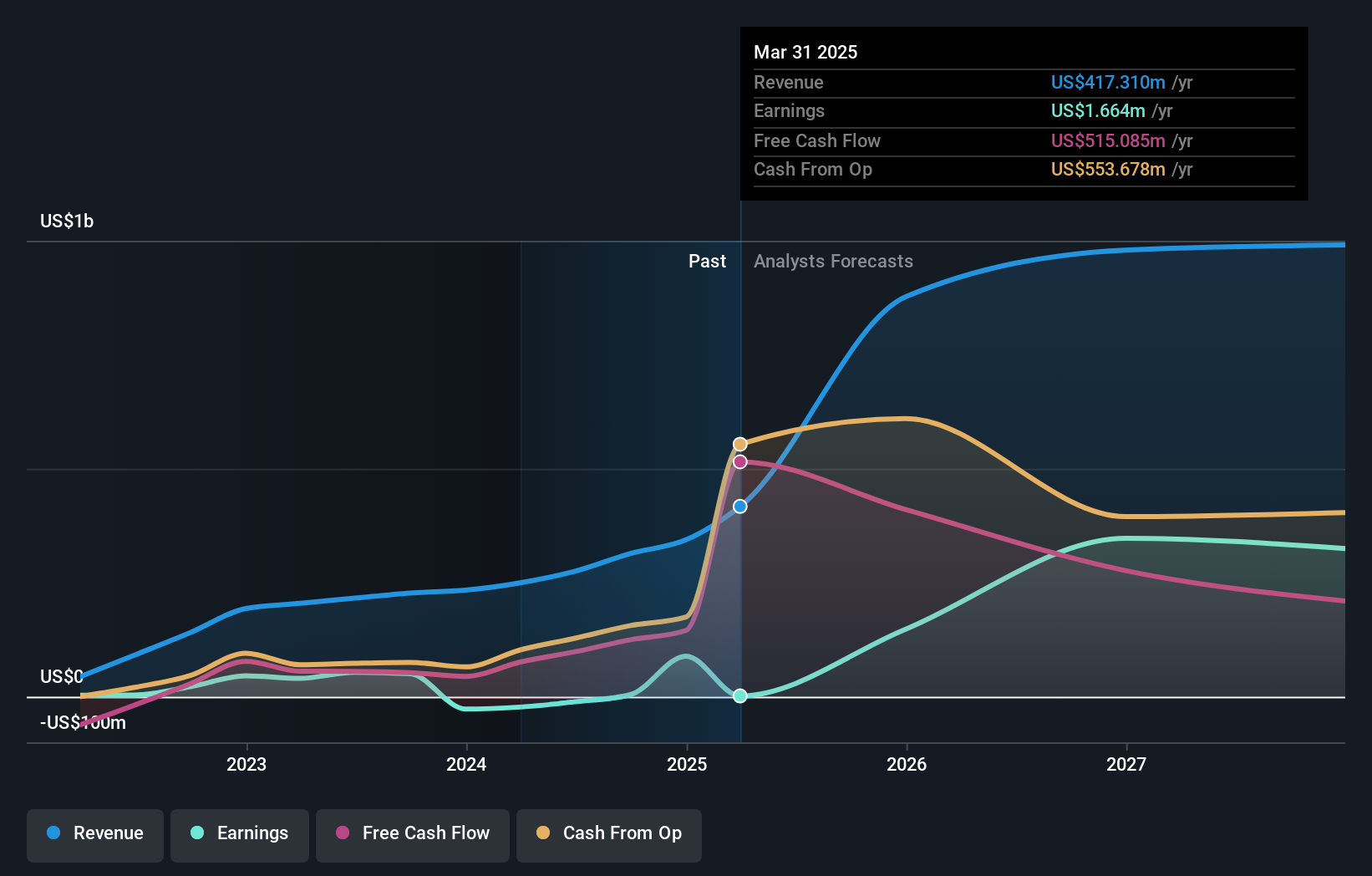

Orla Mining (TSX:OLA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Orla Mining Ltd. is engaged in the acquisition, exploration, development, and exploitation of mineral properties with a market cap of CA$2.22 billion.

Operations: The company generates revenue primarily from the evaluation and exploration of mineral exploration properties, amounting to $314.10 million.

Insider Ownership: 11.5%

Earnings Growth Forecast: 45.4% p.a.

Orla Mining's earnings and revenue are projected to grow significantly, surpassing Canadian market averages. The company's recent acquisition of the Musselwhite Gold Mine is expected to enhance production and cash flow without upfront equity dilution. Despite past shareholder dilution and labor issues at Camino Rojo, Orla remains debt-free with substantial insider ownership. Recent financial results show increased sales and net income, reflecting strong operational performance amid strategic expansions.

- Click here to discover the nuances of Orla Mining with our detailed analytical future growth report.

- According our valuation report, there's an indication that Orla Mining's share price might be on the cheaper side.

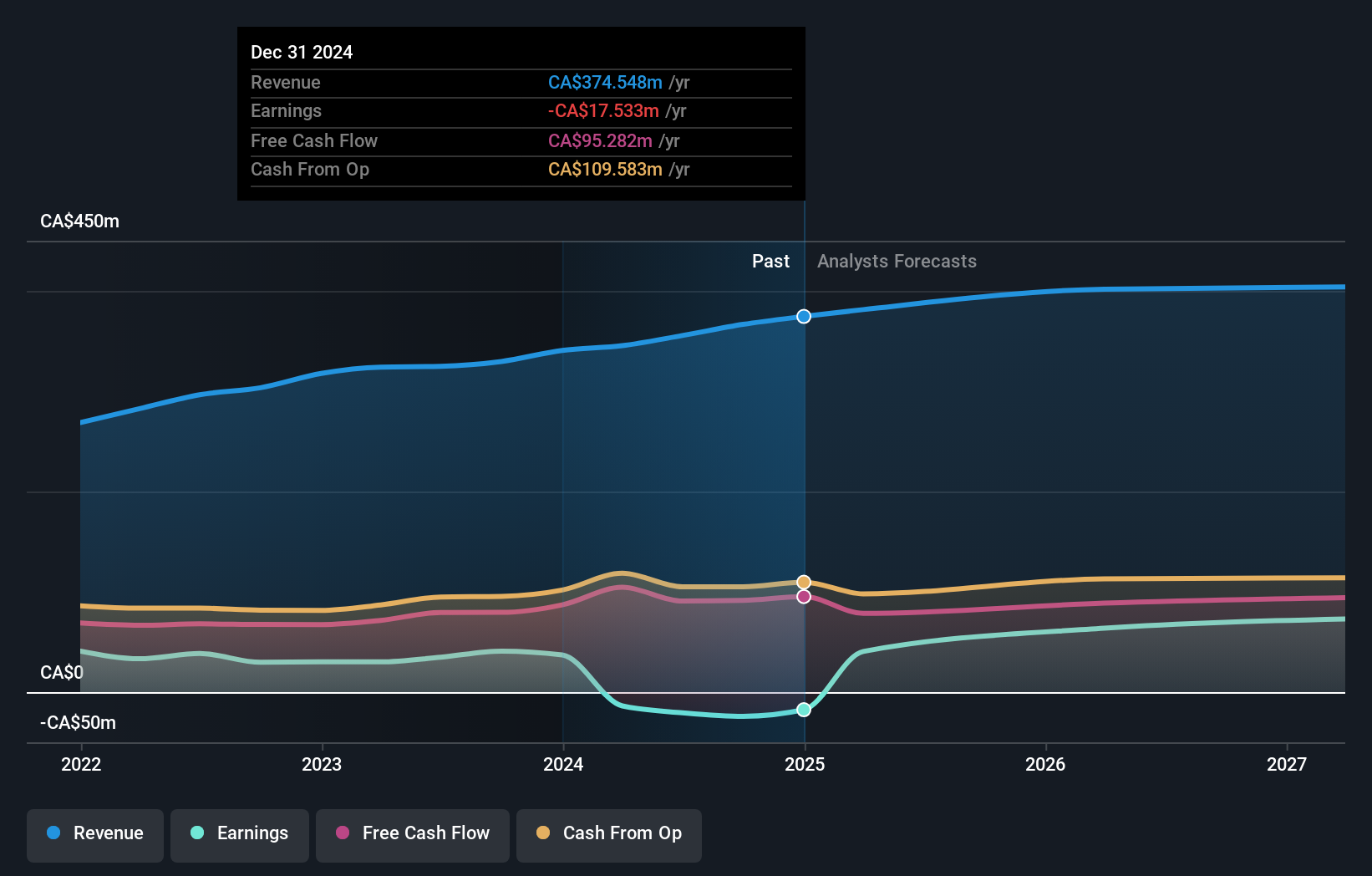

Stingray Group (TSX:RAY.A)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Stingray Group Inc. is a global music, media, and technology company with a market cap of CA$536.63 million.

Operations: The company's revenue is derived from two main segments: Radio, contributing CA$129.80 million, and Broadcasting and Commercial Music, accounting for CA$236.80 million.

Insider Ownership: 25.7%

Earnings Growth Forecast: 81.5% p.a.

Stingray Group's recent initiatives, including launching new streaming TV channels and a strategic partnership with BYD for in-car karaoke, highlight its innovative growth strategies. Despite slower revenue growth forecasts compared to the Canadian market, Stingray is expected to achieve profitability within three years. However, high debt levels and insider selling could be concerns. The company's recent earnings showed increased sales but decreased net income, reflecting mixed financial performance amid expansion efforts.

- Take a closer look at Stingray Group's potential here in our earnings growth report.

- Our expertly prepared valuation report Stingray Group implies its share price may be lower than expected.

Next Steps

- Click here to access our complete index of 37 Fast Growing TSX Companies With High Insider Ownership.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:OLA

Orla Mining

Acquires, explores, develops, and exploits mineral properties.

Exceptional growth potential with excellent balance sheet.

Market Insights

Community Narratives