The Canadian market, much like its global counterparts, has been navigating the implications of a decisive U.S. election outcome that removed a significant source of uncertainty and spurred an impressive post-election rally. In this environment, dividend stocks on the TSX can offer stability and income potential, making them an attractive option for investors looking to balance growth with reliable returns amidst shifting economic policies.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 7.08% | ★★★★★★ |

| Acadian Timber (TSX:ADN) | 6.54% | ★★★★★★ |

| Power Corporation of Canada (TSX:POW) | 4.83% | ★★★★★☆ |

| Enghouse Systems (TSX:ENGH) | 3.41% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.72% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.40% | ★★★★★☆ |

| IGM Financial (TSX:IGM) | 5.07% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 3.89% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.29% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 4.05% | ★★★★★☆ |

Click here to see the full list of 28 stocks from our Top TSX Dividend Stocks screener.

Let's uncover some gems from our specialized screener.

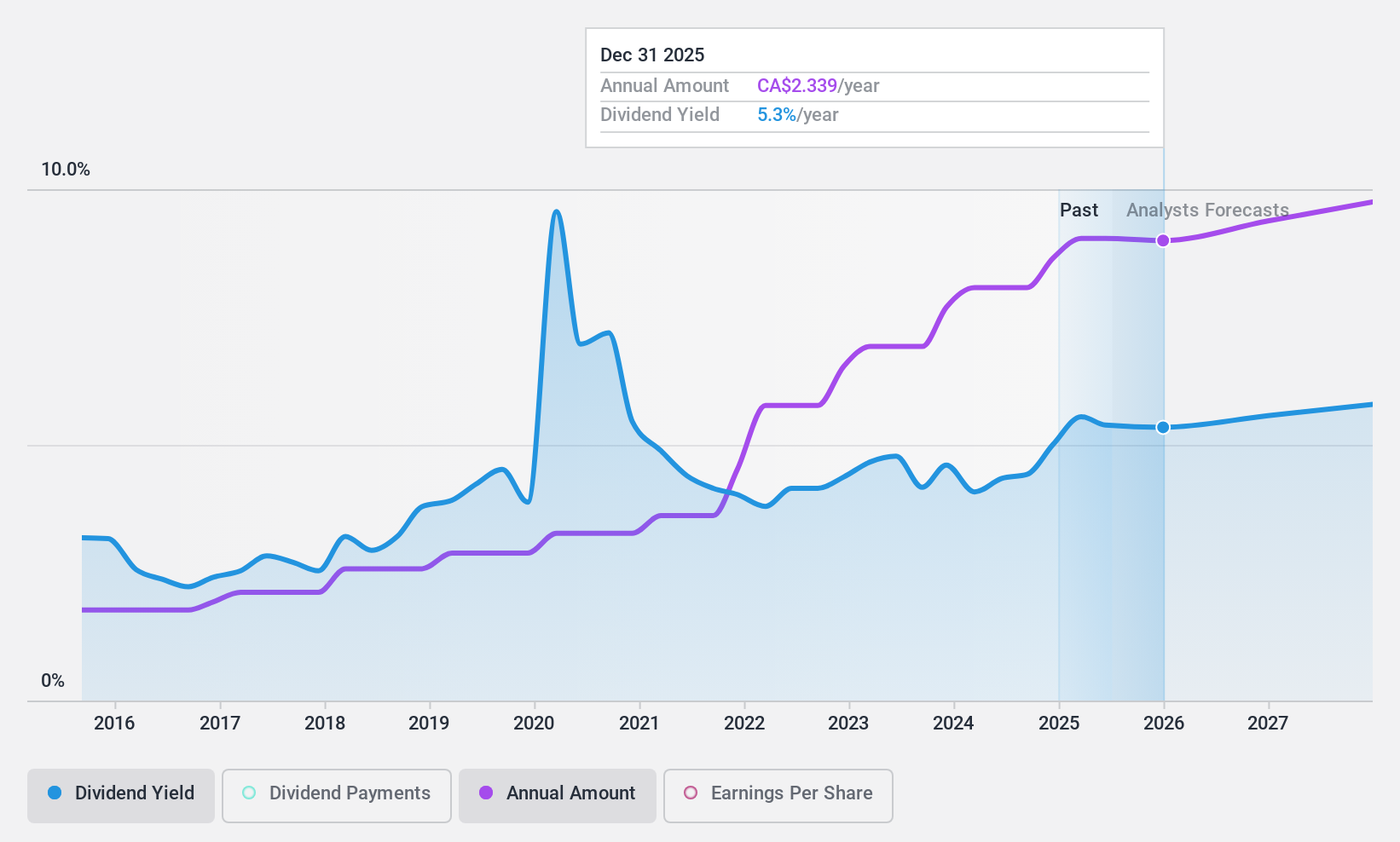

Centerra Gold (TSX:CG)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Centerra Gold Inc. is a gold mining company involved in the acquisition, exploration, development, and operation of gold and copper properties across North America, Turkey, and internationally with a market cap of CA$1.90 billion.

Operations: Centerra Gold Inc.'s revenue is primarily derived from its Öksüt segment ($559.44 million), Molybdenum operations ($232.42 million), and Mount Milligan mine ($460.21 million).

Dividend Yield: 3.2%

Centerra Gold's dividend payments have been volatile over the last decade, though they have increased overall. The current dividend yield is lower compared to top-tier Canadian payers. Despite this, the payout ratio remains sustainable at 43.7% of earnings and 20.9% of cash flows, indicating solid coverage. Recent financial results show a return to profitability with net income for nine months at US$132.89 million, supported by a share buyback plan enhancing shareholder value further.

- Unlock comprehensive insights into our analysis of Centerra Gold stock in this dividend report.

- Our valuation report unveils the possibility Centerra Gold's shares may be trading at a discount.

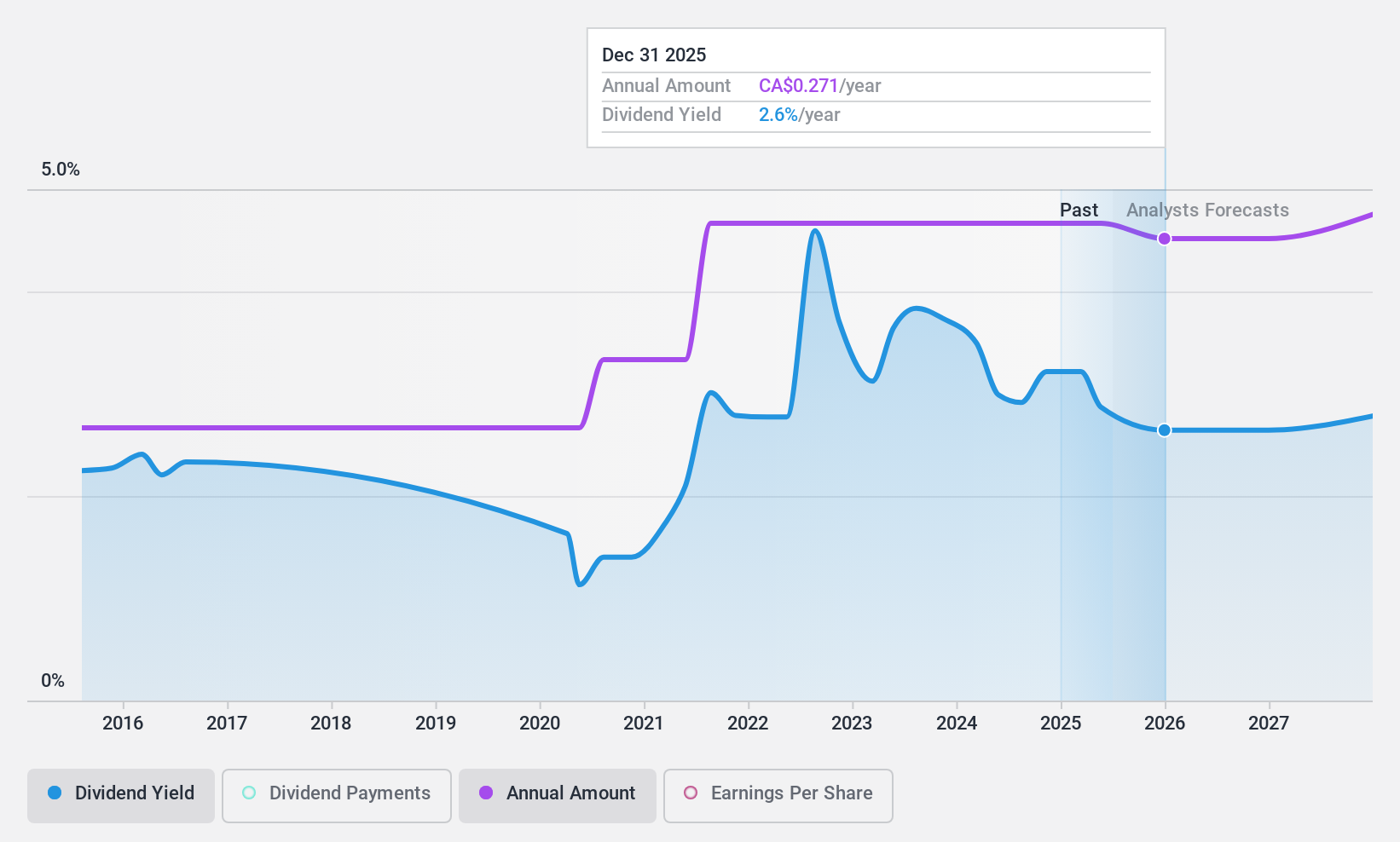

Canadian Natural Resources (TSX:CNQ)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Canadian Natural Resources Limited engages in the acquisition, exploration, development, production, marketing, and sale of crude oil, natural gas, and natural gas liquids (NGLs), with a market cap of approximately CA$100.37 billion.

Operations: Canadian Natural Resources Limited generates revenue from several segments, including Oil Sands Mining and Upgrading (CA$16.30 billion), Exploration and Production - North America (CA$17.21 billion), Exploration and Production - North Sea (CA$537 million), Exploration and Production - Offshore Africa (CA$557 million), and Midstream and Refining (CA$937 million).

Dividend Yield: 4.4%

Canadian Natural Resources has consistently increased its dividends over the past decade, recently raising the quarterly dividend by 7% to C$0.5625 per share. Despite a lower yield compared to top-tier Canadian payers, the dividend is well-covered with a payout ratio of 58.4% and cash payout ratio of 45.6%. The company reported stable earnings and revenue for Q3 2024, alongside an active share buyback program totaling C$2.33 billion this year, supporting shareholder returns.

- Dive into the specifics of Canadian Natural Resources here with our thorough dividend report.

- Our comprehensive valuation report raises the possibility that Canadian Natural Resources is priced lower than what may be justified by its financials.

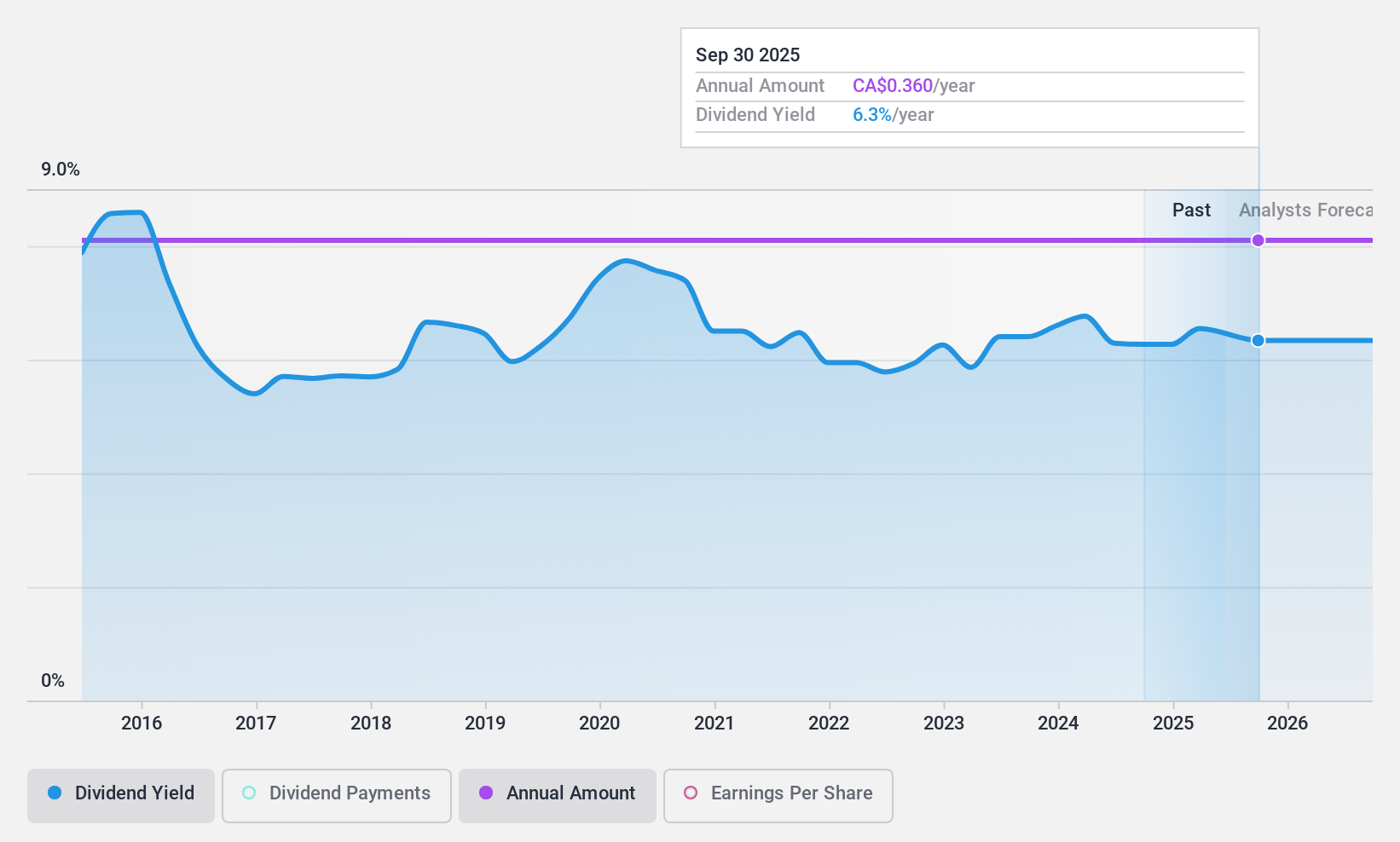

Rogers Sugar (TSX:RSI)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Rogers Sugar Inc. is involved in refining, packaging, marketing, and distributing sugar and maple products across Canada, the United States, Europe, and internationally, with a market cap of CA$720.17 million.

Operations: Rogers Sugar Inc.'s revenue is comprised of CA$981.45 million from sugar and CA$225.32 million from maple products.

Dividend Yield: 6.4%

Rogers Sugar's dividend yield of 6.37% ranks in the top 25% among Canadian payers, yet its sustainability is questionable as dividends are not covered by free cash flows and have been unreliable over the past decade. Although trading at a significant discount to estimated fair value, debt coverage remains an issue with operating cash flow insufficient to cover it. The company became profitable this year, but dividend growth has stalled for ten years.

- Delve into the full analysis dividend report here for a deeper understanding of Rogers Sugar.

- Insights from our recent valuation report point to the potential undervaluation of Rogers Sugar shares in the market.

Summing It All Up

- Embark on your investment journey to our 28 Top TSX Dividend Stocks selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:RSI

Rogers Sugar

Engages in refining, packaging, marketing, and distribution of sugar, maple, and related products in Canada, the United States, Europe, and internationally.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Community Narratives