- Canada

- /

- Oil and Gas

- /

- TSX:CNQ

Canadian Natural Resources (TSX:CNQ) Lifts Dividend By 4% To C$1

Reviewed by Simply Wall St

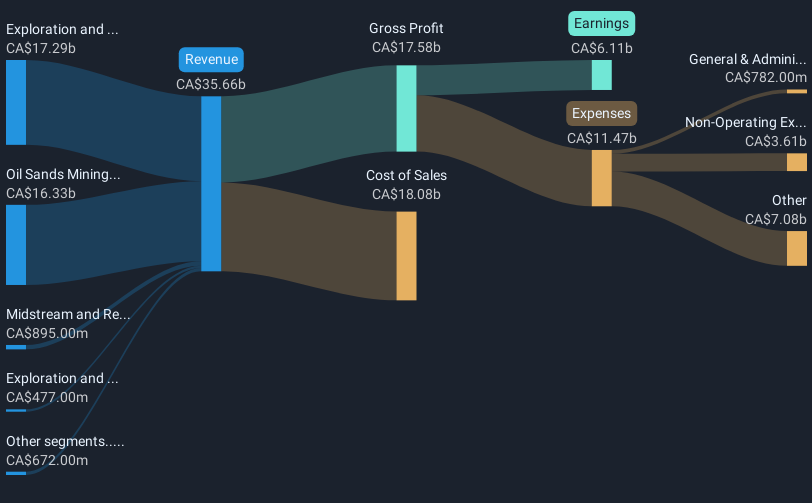

Canadian Natural Resources (TSX:CNQ) recently announced a 4% increase in its quarterly dividend, raising it to CAD 0.5875 per share, alongside reporting a decline in both quarterly and annual earnings compared to the previous year. During this period, the company's stock price remained relatively flat, contrasting significantly with the broader market turmoil, as the Dow and Nasdaq experienced steep declines following new tariffs announced by the U.S. administration. While the overall market faced pressure, Canadian Natural's operational aspects, such as steady production levels and a share buyback program, align more closely with stability amidst economic uncertainty.

The last five years have seen Canadian Natural Resources achieve a total shareholder return of 442.12%, showcasing substantial long-term gains. During this period, the company expanded its production capacity with key acquisitions like Chevron Canada Limited's Alberta assets, enhancing production by approximately 122,500 BOE/day in late 2024. Moreover, operational improvements at facilities such as Scotford and Horizon have bolstered production efficiency and net margins. The focus on cost reductions and reliability improvements has supported this upward trajectory in earnings and cash flow.

Despite a recent 2.65% share buyback, Canadian Natural Resources experienced a decline in earnings, as seen in Q4 2024 with net income dropping to CA$1.14 billion year-over-year. Importantly, the company's performance in the last year lagged behind broader markets, with stock returns underperforming both the Canadian Oil and Gas industry, which saw a 9.5% decline, and the Canadian market, which grew by 2.4%. However, these challenges have not overshadowed its long-term success.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CNQ

Canadian Natural Resources

Engages in the acquisition, exploration, development, production, marketing, and sale of crude oil, natural gas, and natural gas liquids (NGLs) in Western Canada, the United Kingdom sector of the North Sea, and Offshore Africa.

Established dividend payer and good value.

Similar Companies

Market Insights

Community Narratives