Equitable Group Inc. (TSE:EQB) Released Earnings Last Week And Analysts Lifted Their Price Target To CA$137

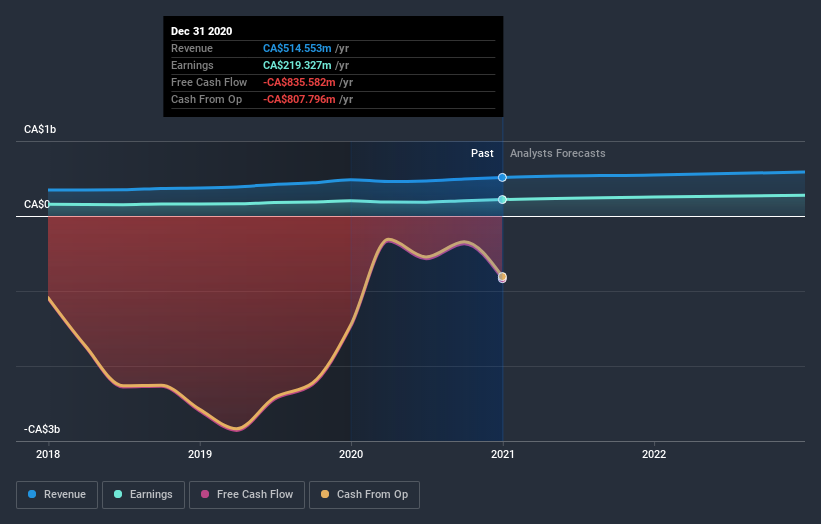

Equitable Group Inc. (TSE:EQB) just released its latest annual results and things are looking bullish. Results were good overall, with revenues beating analyst predictions by 3.7% to hit CA$515m. Statutory earnings per share (EPS) came in at CA$12.95, some 3.1% above whatthe analysts had expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Equitable Group

Taking into account the latest results, the most recent consensus for Equitable Group from seven analysts is for revenues of CA$547.9m in 2021 which, if met, would be an okay 6.5% increase on its sales over the past 12 months. Per-share earnings are expected to expand 10% to CA$14.36. Yet prior to the latest earnings, the analysts had been anticipated revenues of CA$547.6m and earnings per share (EPS) of CA$14.18 in 2021. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

With the analysts reconfirming their revenue and earnings forecasts, it's surprising to see that the price target rose 12% to CA$137. It looks as though they previously had some doubts over whether the business would live up to their expectations. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Equitable Group analyst has a price target of CA$138 per share, while the most pessimistic values it at CA$104. Still, with such a tight range of estimates, it suggeststhe analysts have a pretty good idea of what they think the company is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Equitable Group's past performance and to peers in the same industry. We would highlight that Equitable Group's revenue growth is expected to slow, with forecast 6.5% increase next year well below the historical 13%p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 1.2% next year. Even after the forecast slowdown in growth, it seems obvious that Equitable Group is also expected to grow faster than the wider industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Equitable Group going out to 2022, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 2 warning signs for Equitable Group that you should be aware of.

If you’re looking to trade Equitable Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EQB might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:EQB

EQB

Through its subsidiary, Equitable Bank, provides personal and commercial banking services to retail and commercial customers in Canada.

High growth potential established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Cheap if able to sustain revenue, and a potential bargain if able to turn store openings into revenue growth

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)