Advertisement

- Australia

- /

- Infrastructure

- /

- ASX:TCL

Here's Why We Think Transurban Group (ASX:TCL) Might Deserve Your Attention Today

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Transurban Group (ASX:TCL). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Transurban Group with the means to add long-term value to shareholders.

See our latest analysis for Transurban Group

How Fast Is Transurban Group Growing Its Earnings Per Share?

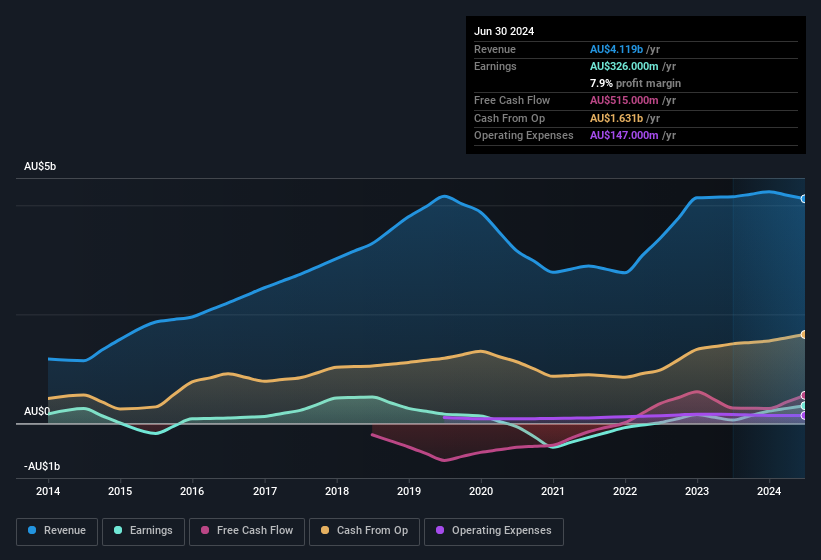

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. Which is why EPS growth is looked upon so favourably. Commendations have to be given in seeing that Transurban Group grew its EPS from AU$0.021 to AU$0.11, in one short year. Even though that growth rate may not be repeated, that looks like a breakout improvement.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. While revenue is looking a bit flat, the good news is EBIT margins improved by 3.5 percentage points to 27%, in the last twelve months. Which is a great look for the company.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Transurban Group's future profits.

Are Transurban Group Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We haven't seen any insiders selling Transurban Group shares, in the last year. Add in the fact that Gary Lennon, the Independent Non-Executive Director of the company, paid AU$53k for shares at around AU$13.17 each. Purchases like this can help the investors understand the views of the management team; in which case they see some potential in Transurban Group.

Recent insider purchases of Transurban Group stock is not the only way management has kept the interests of the general public shareholders in mind. Namely, Transurban Group has a very reasonable level of CEO pay. Our analysis has discovered that the median total compensation for the CEOs of companies like Transurban Group, with market caps over AU$12b, is about AU$6.7m.

The Transurban Group CEO received AU$3.9m in compensation for the year ending June 2024. That comes in below the average for similar sized companies and seems pretty reasonable. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Should You Add Transurban Group To Your Watchlist?

Transurban Group's earnings have taken off in quite an impressive fashion. The company can also boast of insider buying, and reasonable remuneration for the CEO. It could be that Transurban Group is at an inflection point, given the EPS growth. If these have piqued your interest, then this stock surely warrants a spot on your watchlist. You should always think about risks though. Case in point, we've spotted 2 warning signs for Transurban Group you should be aware of.

Keen growth investors love to see insider activity. Thankfully, Transurban Group isn't the only one. You can see a a curated list of Australian companies which have exhibited consistent growth accompanied by high insider ownership.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Transurban Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:TCL

Transurban Group

Engages in the development, operation, management, and maintenance of toll road networks.

Moderate growth potential low.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|35.4% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.3% undervalued

MI

Community Contributor