Risks To Shareholder Returns Are Elevated At These Prices For Telstra Group Limited (ASX:TLS)

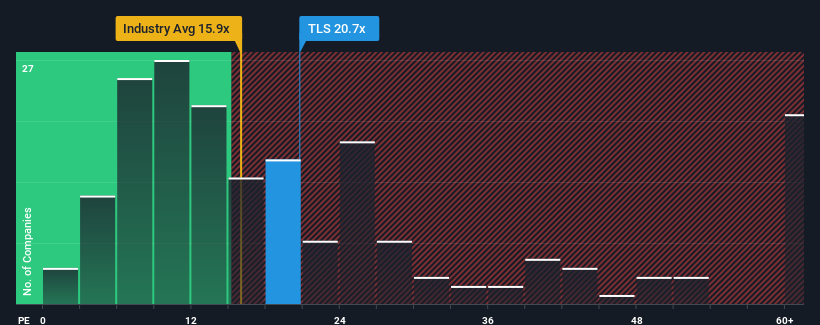

It's not a stretch to say that Telstra Group Limited's (ASX:TLS) price-to-earnings (or "P/E") ratio of 20.7x right now seems quite "middle-of-the-road" compared to the market in Australia, where the median P/E ratio is around 20x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Telstra Group certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is moderate because investors think the company's earnings will be less resilient moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Telstra Group

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Telstra Group would need to produce growth that's similar to the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 10% last year. EPS has also lifted 18% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 7.6% each year during the coming three years according to the analysts following the company. That's shaping up to be materially lower than the 17% per annum growth forecast for the broader market.

With this information, we find it interesting that Telstra Group is trading at a fairly similar P/E to the market. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

What We Can Learn From Telstra Group's P/E?

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Telstra Group currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Before you take the next step, you should know about the 2 warning signs for Telstra Group that we have uncovered.

If these risks are making you reconsider your opinion on Telstra Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Telstra Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:TLS

Telstra Group

Engages in the provision of telecommunications and information services to businesses, government, and individuals in Australia and internationally.

Mediocre balance sheet low.

Similar Companies

Market Insights

Community Narratives