Advertisement

- Australia

- /

- Retail REITs

- /

- ASX:DXC

Does APN Convenience Retail REIT (ASX:AQR) Deserve A Spot On Your Watchlist?

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. And in their study titled Who Falls Prey to the Wolf of Wall Street?' Leuz et. al. found that it is 'quite common' for investors to lose money by buying into 'pump and dump' schemes.

So if you're like me, you might be more interested in profitable, growing companies, like APN Convenience Retail REIT (ASX:AQR). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

Check out our latest analysis for APN Convenience Retail REIT

APN Convenience Retail REIT's Improving Profits

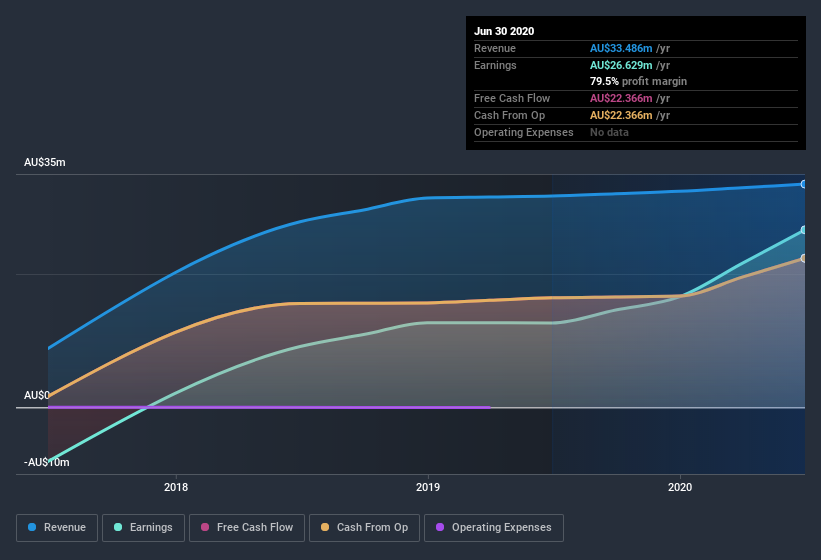

Over the last three years, APN Convenience Retail REIT has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. As a result, I'll zoom in on growth over the last year, instead. Like a firecracker arcing through the night sky, APN Convenience Retail REIT's EPS shot from AU$0.16 to AU$0.30, over the last year. Year on year growth of 86% is certainly a sight to behold.

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). While we note APN Convenience Retail REIT's EBIT margins were flat over the last year, revenue grew by a solid 5.7% to AU$33m. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of APN Convenience Retail REIT's forecast profits?

Are APN Convenience Retail REIT Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Not only did APN Convenience Retail REIT insiders refrain from selling stock during the year, but they also spent AU$81k buying it. That's nice to see, because it suggests insiders are optimistic. We also note that it was the Independent Non-Executive Chairman of APN Funds Management Limited, Geoffrey Brunsdon, who made the biggest single acquisition, paying AU$49k for shares at about AU$3.66 each.

On top of the insider buying, it's good to see that APN Convenience Retail REIT insiders have a valuable investment in the business. Indeed, they hold AU$18m worth of its stock. That's a lot of money, and no small incentive to work hard. Even though that's only about 4.5% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

Does APN Convenience Retail REIT Deserve A Spot On Your Watchlist?

APN Convenience Retail REIT's earnings per share growth have been levitating higher, like a mountain goat scaling the Alps. Just as heartening; insiders both own and are buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe APN Convenience Retail REIT deserves timely attention. Don't forget that there may still be risks. For instance, we've identified 3 warning signs for APN Convenience Retail REIT that you should be aware of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of APN Convenience Retail REIT, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

When trading APN Convenience Retail REIT or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:DXC

Dexus Convenience Retail REIT

Dexus Convenience Retail REIT (ASX code: DXC) is a listed Australian real estate investment trust which owns high quality Australian service stations and convenience retail assets.

Moderate growth potential with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor