- Australia

- /

- Metals and Mining

- /

- ASX:WGX

Has Westgold’s 102% 2025 Surge Already Priced In Its Growth Potential?

Reviewed by Bailey Pemberton

- If you are wondering whether Westgold Resources still offers good value after its big run, or if the gold has already been mined out of the share price, you are in the right place.

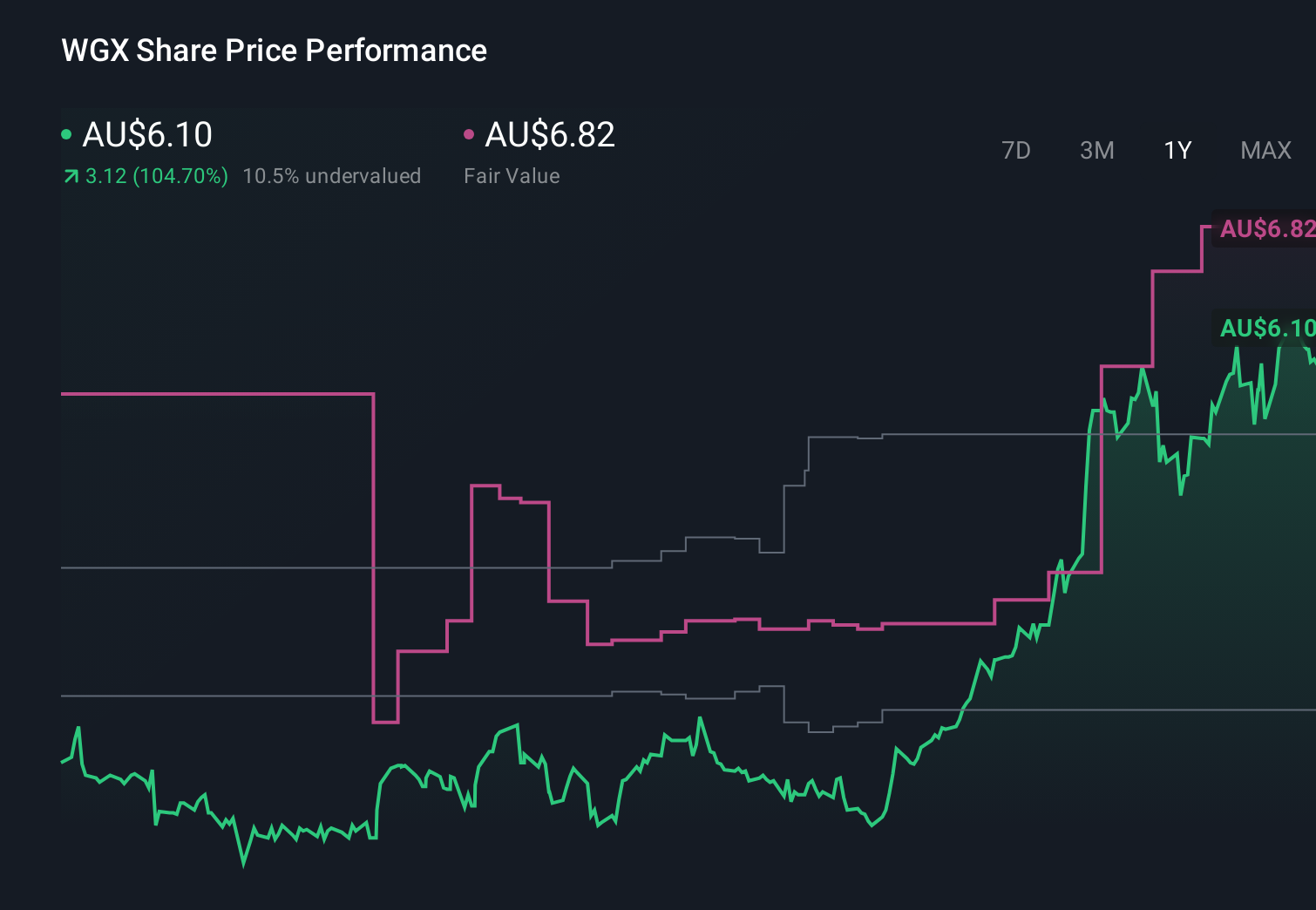

- The stock is up 3.4% over the last week, 2.6% over the past month, and an eye catching 102.1% year to date. This builds on an 86.9% 1 year gain and a 594.7% rise over 3 years.

- Much of this momentum has been driven by stronger sentiment toward Australian gold producers and Westgold's continued focus on improving operational efficiencies across its portfolio of mines. Investors are clearly re rating the business as execution improves and gold prices stay supportive. This raises the question of whether the current share price fully reflects these shifts.

- On our metrics Westgold scores a solid 5/6 valuation score, suggesting it screens as undervalued on most of our checks. Next we will break down what that means across different valuation methods and hint at an even richer way to think about value by the end of this piece.

Approach 1: Westgold Resources Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company is worth by taking the cash it is expected to generate in the future and discounting those cash flows back into today’s A$ terms. For Westgold Resources, Simply Wall St uses a 2 Stage Free Cash Flow to Equity model built on analyst forecasts and then extends the trend further out.

Westgold’s latest twelve month free cash flow is slightly negative at around A$4.4 million, but analysts expect a sharp turnaround, projecting free cash flow to reach about A$1.8 billion by 2035. The path there includes A$644.7 million in 2026, rising to just over A$1.0 billion by 2028, with later years extrapolated from these forecasts rather than directly provided by analysts.

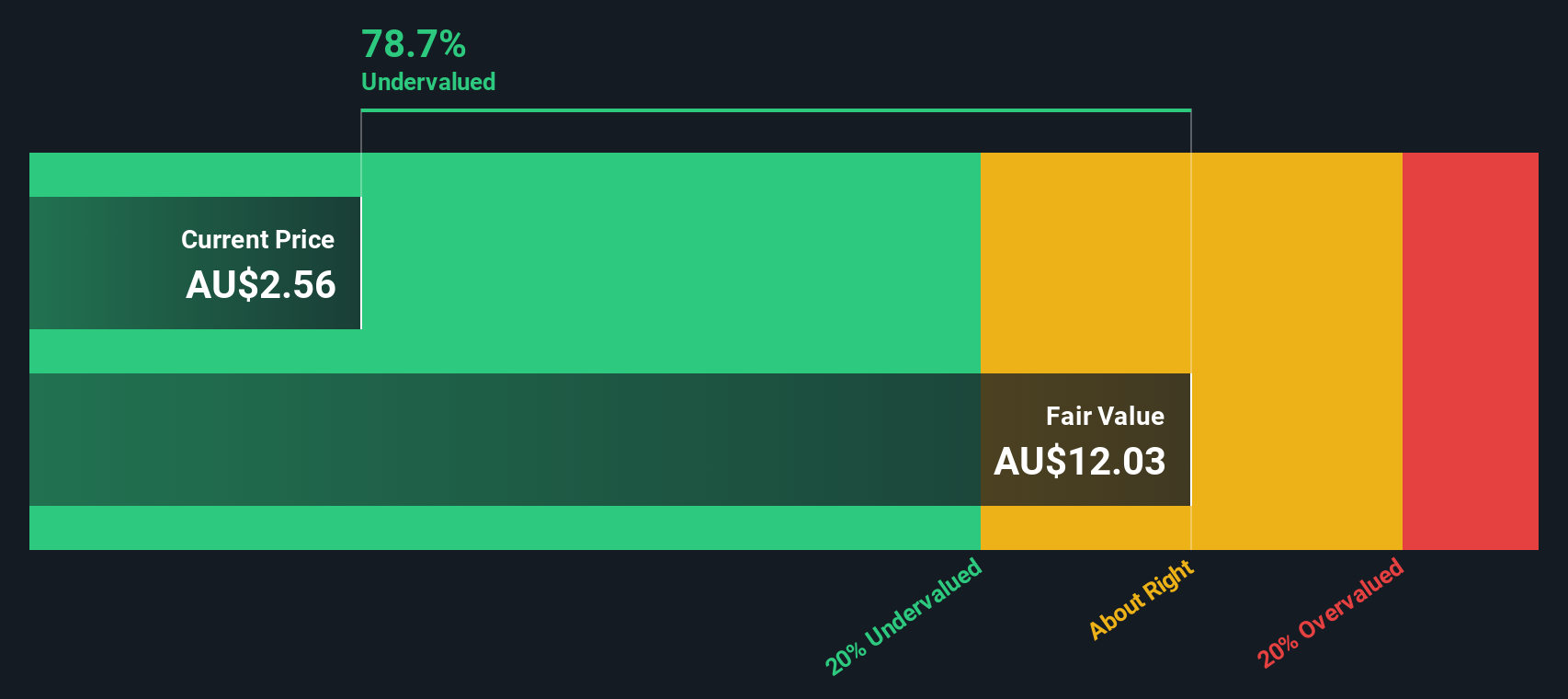

When these projected cash flows are discounted to today and combined with an estimate for cash flows beyond year ten, the model arrives at an intrinsic value of roughly A$30.24 per share. With the DCF implying an 80.7% discount to the current share price, Westgold appears materially undervalued on this cash flow view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Westgold Resources is undervalued by 80.7%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

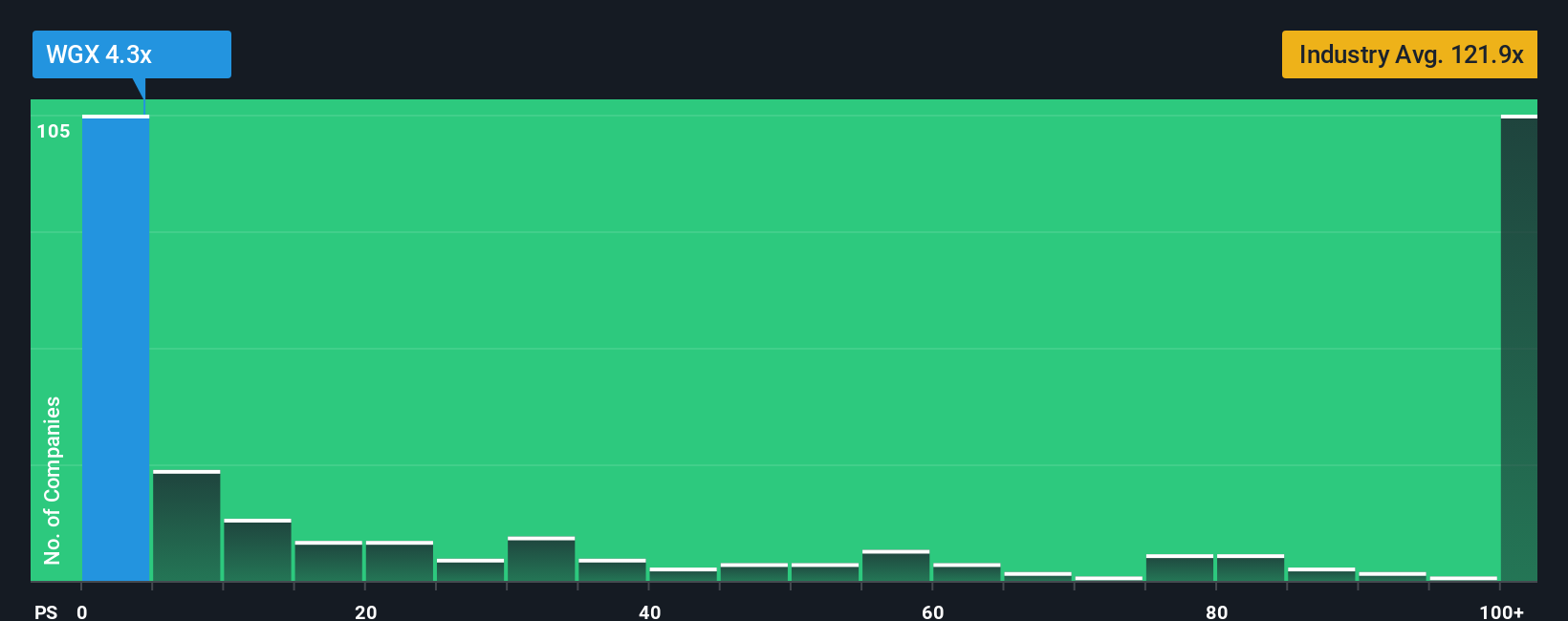

Approach 2: Westgold Resources Price vs Sales

For companies that are already generating meaningful revenue, the price to sales, or P S, ratio is a useful way to gauge value because it focuses on how much investors are paying for each dollar of current sales, without getting distorted by short term swings in profit.

In general, higher expected growth and lower business risk can justify a higher P S multiple. By contrast, slower growth or greater uncertainty usually calls for a lower, more conservative ratio. Against that backdrop, Westgold is currently trading on a P S of 4.06x, which is well below the Metals and Mining industry average of 121.56x and also below the 7.41x average of its closer peer group.

Simply Wall St’s Fair Ratio metric goes a step further by estimating what P S multiple would make sense for Westgold specifically, given its earnings growth outlook, margins, industry, market cap and risk profile. This is more tailored than a straight peer or industry comparison, which can be skewed by very different business models or risk levels. Westgold’s Fair Ratio is 2.45x, noticeably below its current 4.06x, which suggests the shares are trading above what our fundamentals based framework would support.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1456 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Westgold Resources Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Westgold’s story with a financial forecast and a fair value estimate, all within the Simply Wall St Community page used by millions of investors. You choose the assumptions for future revenue, earnings and margins. The Narrative turns those into a forecast and fair value that you can compare to today’s price to help you decide whether to buy, hold or sell. It automatically updates when new information such as production guidance or earnings is released. One investor might build a bullish Westgold Narrative that results in a fair value near A$6.82 based on strong production growth and expanding margins. Another, more cautious investor might lean closer to the low analyst target of A$3.76 if they think integration risks, cost inflation and lower grades will cap profitability, with both perspectives clearly expressed and quantified as living, up to date stories behind the numbers.

Do you think there's more to the story for Westgold Resources? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Westgold Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:WGX

Westgold Resources

Engages in the exploration, development, and operation of gold mines in Western Australia.

Exceptional growth potential and undervalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)