- Australia

- /

- Metals and Mining

- /

- ASX:OBM

Three Undiscovered Gems in Australia with Strong Potential

Reviewed by Simply Wall St

Over the last 7 days, the Australian market has remained flat, yet it has experienced a significant 20% increase over the past year with earnings forecast to grow by 12% annually. In this dynamic environment, identifying stocks with strong potential often involves looking for companies that are not only underappreciated but also poised to benefit from future growth trends.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 9.94% | 6.48% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Hancock & Gore | NA | -70.20% | 38.14% | ★★★★★★ |

| Lycopodium | NA | 17.22% | 33.85% | ★★★★★★ |

| Red Hill Minerals | NA | 75.05% | 36.74% | ★★★★★★ |

| BSP Financial Group | 7.53% | 7.31% | 4.10% | ★★★★★☆ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| AMCIL | NA | 5.16% | 5.31% | ★★★★★☆ |

| Hearts and Minds Investments | 1.00% | 18.81% | 20.95% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Emerald Resources (ASX:EMR)

Simply Wall St Value Rating: ★★★★★☆

Overview: Emerald Resources NL is involved in the exploration and development of mineral reserves in Cambodia and Australia, with a market capitalization of A$2.90 billion.

Operations: Emerald Resources generates revenue primarily from mine operations, totaling A$366.04 million. The company's financial performance is highlighted by a net profit margin trend that offers insight into its profitability dynamics.

Emerald Resources, a dynamic player in the mining sector, has shown impressive financial health with earnings growing by 41.9% over the past year, outpacing the industry average of 1.6%. The company reported sales of A$371.07 million for the year ending June 2024, up from A$299.48 million previously, and net income rose to A$84.27 million from A$59.36 million a year ago. Despite shareholder dilution over the past year, its debt is well-covered by EBIT at 18.6x coverage and it holds more cash than total debt, indicating robust financial management amidst ongoing growth prospects in Cambodia and Australia projects.

- Delve into the full analysis health report here for a deeper understanding of Emerald Resources.

Gain insights into Emerald Resources' past trends and performance with our Past report.

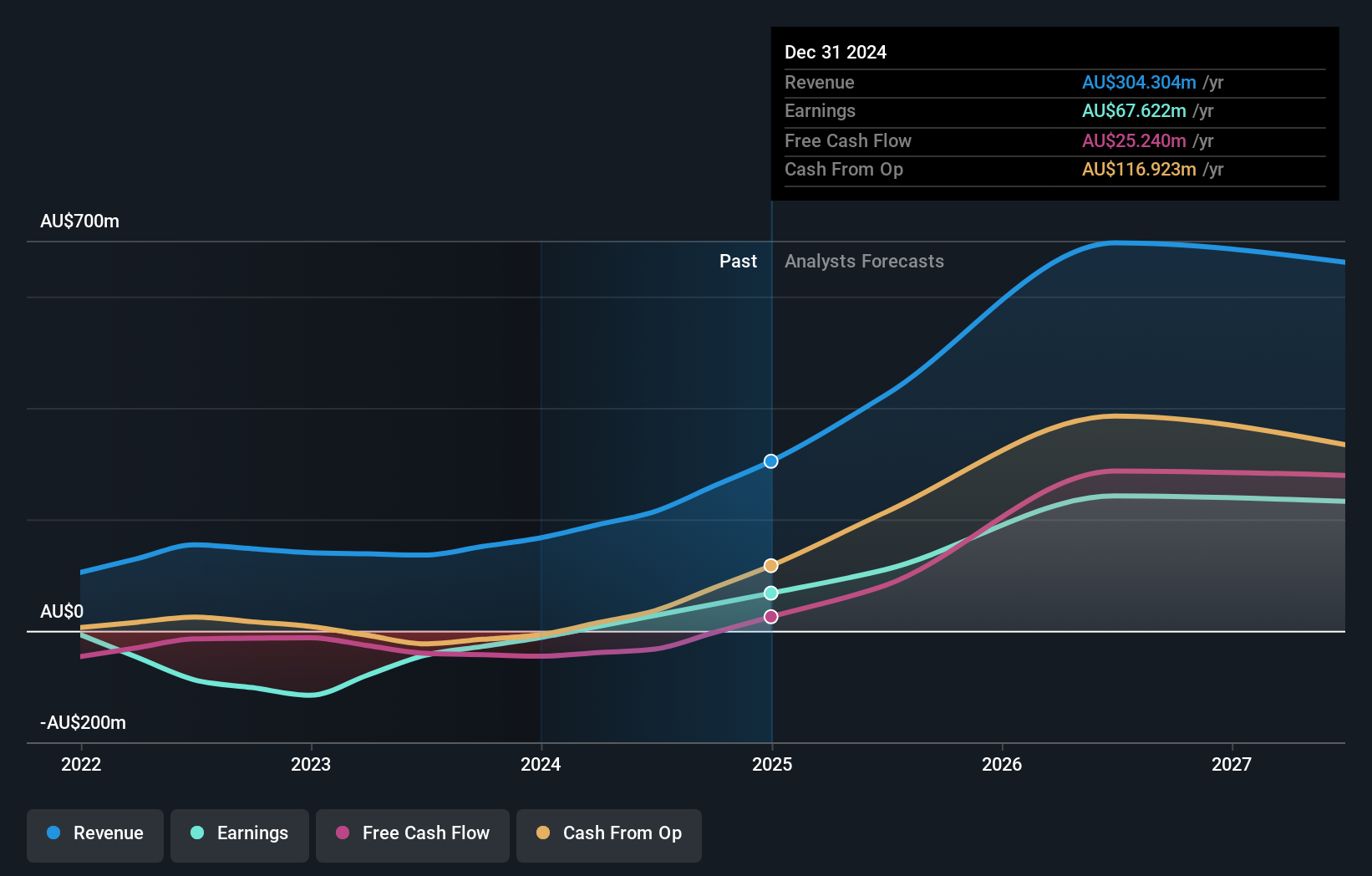

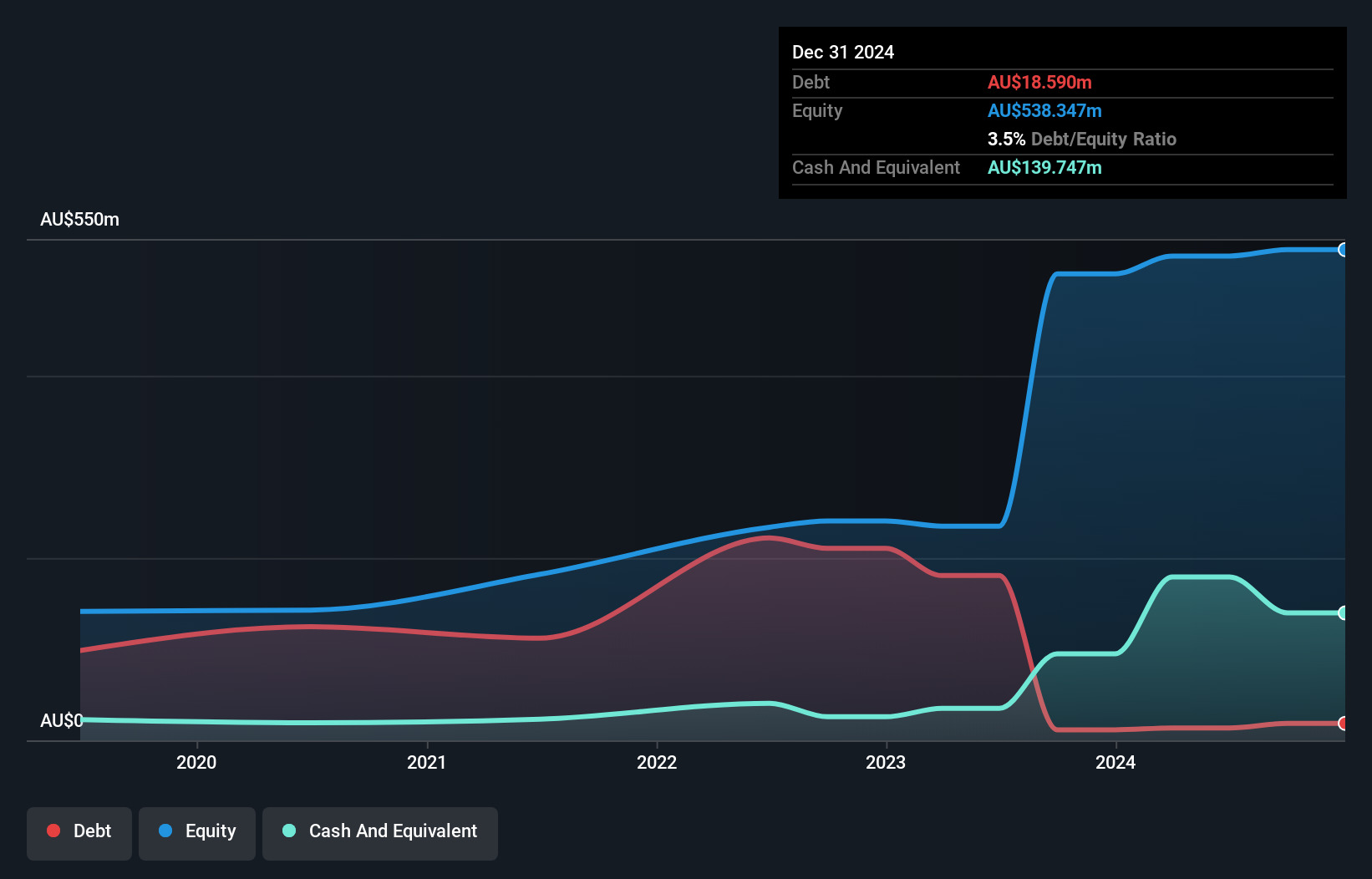

Ora Banda Mining (ASX:OBM)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Ora Banda Mining Limited is an Australian company focused on the exploration, operation, and development of mineral properties with a market capitalization of A$1.59 billion.

Operations: Ora Banda Mining generates its revenue primarily from gold mining, with reported earnings of A$214.24 million. The company's financial performance is influenced by its net profit margin trends.

Ora Banda Mining, a promising player in the Australian mining landscape, has recently turned profitable with net income reaching A$27.57 million for the year ending June 2024, a significant improvement from last year's A$44.13 million loss. The company reported sales of A$214.24 million, up from A$135.89 million previously, and basic earnings per share improved to A$0.0162 compared to a loss of A$0.0323 last year. Despite being dropped from the S&P/ASX Emerging Companies Index in September 2024, OBM's debt to equity ratio remains manageable at 4.1%, and its interest payments are well-covered by EBIT at 7.8x coverage.

- Click here to discover the nuances of Ora Banda Mining with our detailed analytical health report.

Assess Ora Banda Mining's past performance with our detailed historical performance reports.

Redox (ASX:RDX)

Simply Wall St Value Rating: ★★★★★★

Overview: Redox Limited is a company that supplies and distributes chemicals, ingredients, and raw materials across Australia, New Zealand, the United States, and internationally with a market capitalization of approximately A$1.93 billion.

Operations: Redox generates revenue primarily from its wholesale segment, specifically in drugs, amounting to A$1.14 billion.

Redox, an intriguing player in the Australian market, has shown a commendable performance with net income rising to A$90.24 million from A$80.73 million last year. Despite a dip in sales to A$1,137.33 million from A$1,257.52 million, the company remains profitable and maintains high-quality earnings. Its debt-to-equity ratio impressively dropped from 69.6% to 2.6% over five years, indicating stronger financial health now than before. With a price-to-earnings ratio of 21.4x below the industry average of 21.6x and positive free cash flow trends like reaching A$174.8 million recently, Redox appears well-positioned for continued stability and potential growth in its sector.

Key Takeaways

- Gain an insight into the universe of 56 ASX Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:OBM

Ora Banda Mining

Engages in the exploration, operation, and development of mineral properties in Australia.

Exceptional growth potential with adequate balance sheet.