- Australia

- /

- Metals and Mining

- /

- ASX:LYC

Lynas Rare Earths Limited's (ASX:LYC) CEO Looks Like They Deserve Their Pay Packet

The performance at Lynas Rare Earths Limited (ASX:LYC) has been quite strong recently and CEO Amanda Lacaze has played a role in it. Shareholders will have this at the front of their minds in the upcoming AGM on 28 November 2021. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. Here is our take on why we think CEO compensation is not extravagant.

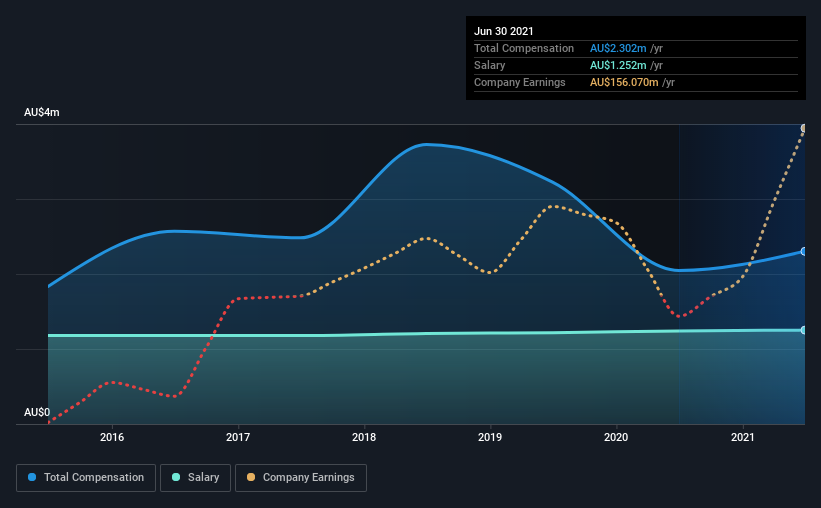

See our latest analysis for Lynas Rare Earths

How Does Total Compensation For Amanda Lacaze Compare With Other Companies In The Industry?

According to our data, Lynas Rare Earths Limited has a market capitalization of AU$7.7b, and paid its CEO total annual compensation worth AU$2.3m over the year to June 2021. Notably, that's an increase of 12% over the year before. Notably, the salary which is AU$1.25m, represents a considerable chunk of the total compensation being paid.

On examining similar-sized companies in the industry with market capitalizations between AU$5.5b and AU$17b, we discovered that the median CEO total compensation of that group was AU$2.7m. From this we gather that Amanda Lacaze is paid around the median for CEOs in the industry. Moreover, Amanda Lacaze also holds AU$29m worth of Lynas Rare Earths stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | AU$1.3m | AU$1.2m | 54% |

| Other | AU$1.1m | AU$806k | 46% |

| Total Compensation | AU$2.3m | AU$2.0m | 100% |

Talking in terms of the industry, salary represented approximately 59% of total compensation out of all the companies we analyzed, while other remuneration made up 41% of the pie. There isn't a significant difference between Lynas Rare Earths and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Lynas Rare Earths Limited's Growth

Lynas Rare Earths Limited's earnings per share (EPS) grew 25% per year over the last three years. Its revenue is up 60% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. Most shareholders would be pleased to see strong revenue growth combined with EPS growth. This combo suggests a fast growing business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Lynas Rare Earths Limited Been A Good Investment?

Most shareholders would probably be pleased with Lynas Rare Earths Limited for providing a total return of 313% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Some shareholders will probably be more lenient on CEO compensation in the upcoming AGM given the pleasing performance of the company recently. However, despite the strong growth in earnings and share price growth, the focus for shareholders would be how the company plans to steer the company towards sustainable profitability in the near future.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Lynas Rare Earths that you should be aware of before investing.

Switching gears from Lynas Rare Earths, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:LYC

Lynas Rare Earths

Engages in the exploration, development, mining, extraction, and processing of rare earth minerals in Australia and Malaysia.

Flawless balance sheet with high growth potential.