- Australia

- /

- Metals and Mining

- /

- ASX:BHP

What Does China’s Iron Ore Ban Mean for BHP Shares in 2025?

Reviewed by Bailey Pemberton

If you have been watching BHP Group lately, you are probably wrestling with the big question a lot of investors are asking right now: Is it time to jump in, hold tight, or cash out? With the stock recently closing at $43.11, and posting gains of 5.2% in the last 30 days and 7.9% so far this year, BHP’s momentum is tough to ignore. The 1-year return is a more modest 2.4%. Looking out a bit further, the 3-year return stands at 28.0%, while the 5-year return is 86.8%, which may encourage long-term investors.

Lately, BHP has faced headlines that attracted investor attention. Just last week, China’s state iron ore buyer pressed pause on all new iron ore deals with BHP due to a pricing dispute. This announcement drew widespread attention and may have concerned some investors. Still, the stock’s recent performance suggests that investors see potential growth or believe that the risks are already reflected in the price. Meanwhile, BHP continues to make news on the sustainability front and navigates legacy legal challenges, both of which contribute to the complex picture influencing its valuation and the confidence of shareholders.

It can be tempting to focus on short-term news and market swings, but a careful look at valuation often tells a deeper story. By breaking down BHP’s value score—an impressive 5 out of 6 on our checks for undervalued companies—it is clear that different valuation methods can provide varied perspectives, and that answering the question, “what’s the stock worth?” is more nuanced than it first appears. By the end, readers will have a better framework for evaluating what BHP is really worth.

Why BHP Group is lagging behind its peers

Approach 1: BHP Group Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting future free cash flows and discounting them back to today's dollars. This method aims to capture the present worth of all anticipated future cash generated by the business.

BHP Group's most recent annual free cash flow stands at $10.35 billion. Analysts forecast that over the coming decade, this figure will fluctuate but generally maintain strength, with Simply Wall St projecting free cash flow to reach $10.71 billion by 2035. The company is expected to see some ups and downs in annual cash generation, with analyst-driven estimates provided for the next five years and longer-term projections extrapolated from industry trends and company performance.

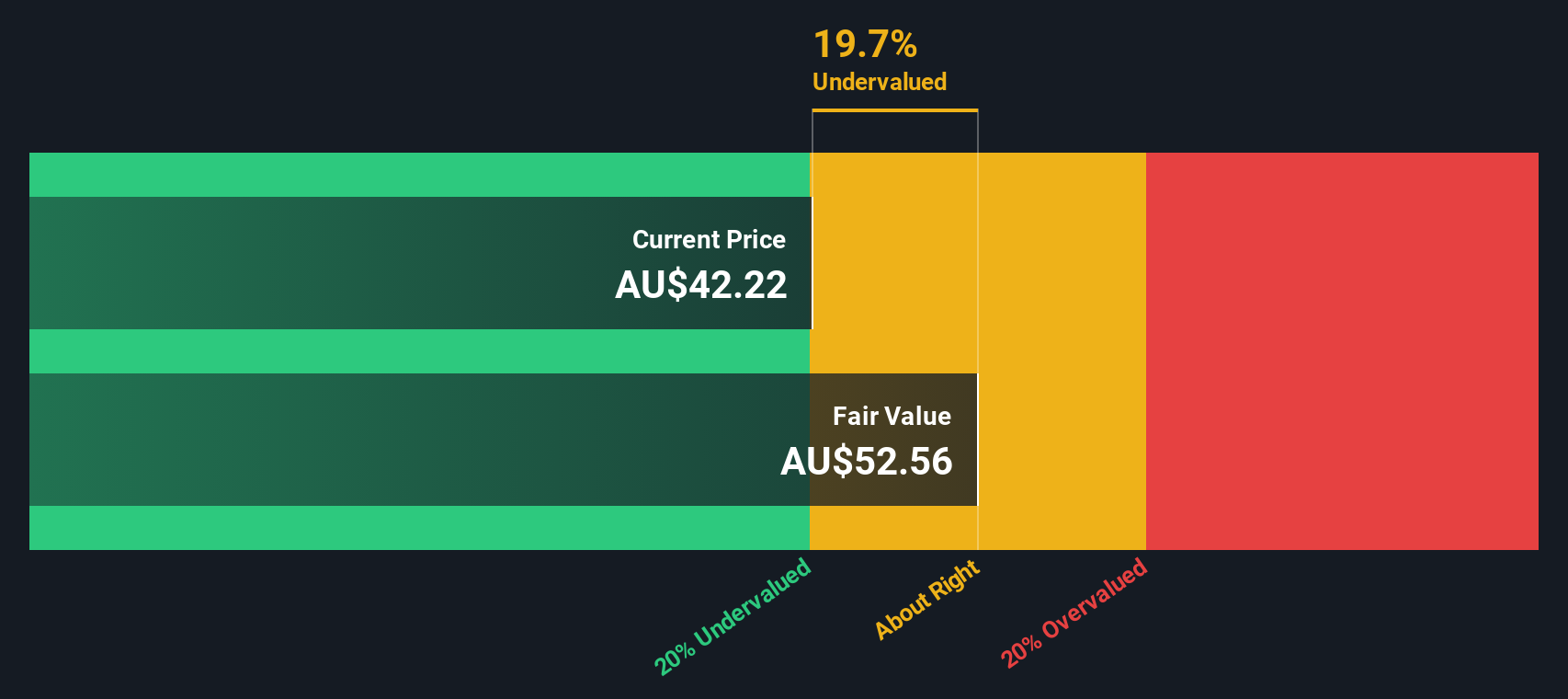

Using the DCF approach, BHP Group’s estimated fair value is $55.90 per share. Compared to the current share price of $43.11, this signals the stock is trading at a 22.9% discount to its intrinsic value. According to this key valuation metric, BHP Group appears significantly undervalued right now.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests BHP Group is undervalued by 22.9%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: BHP Group Price vs Earnings (PE)

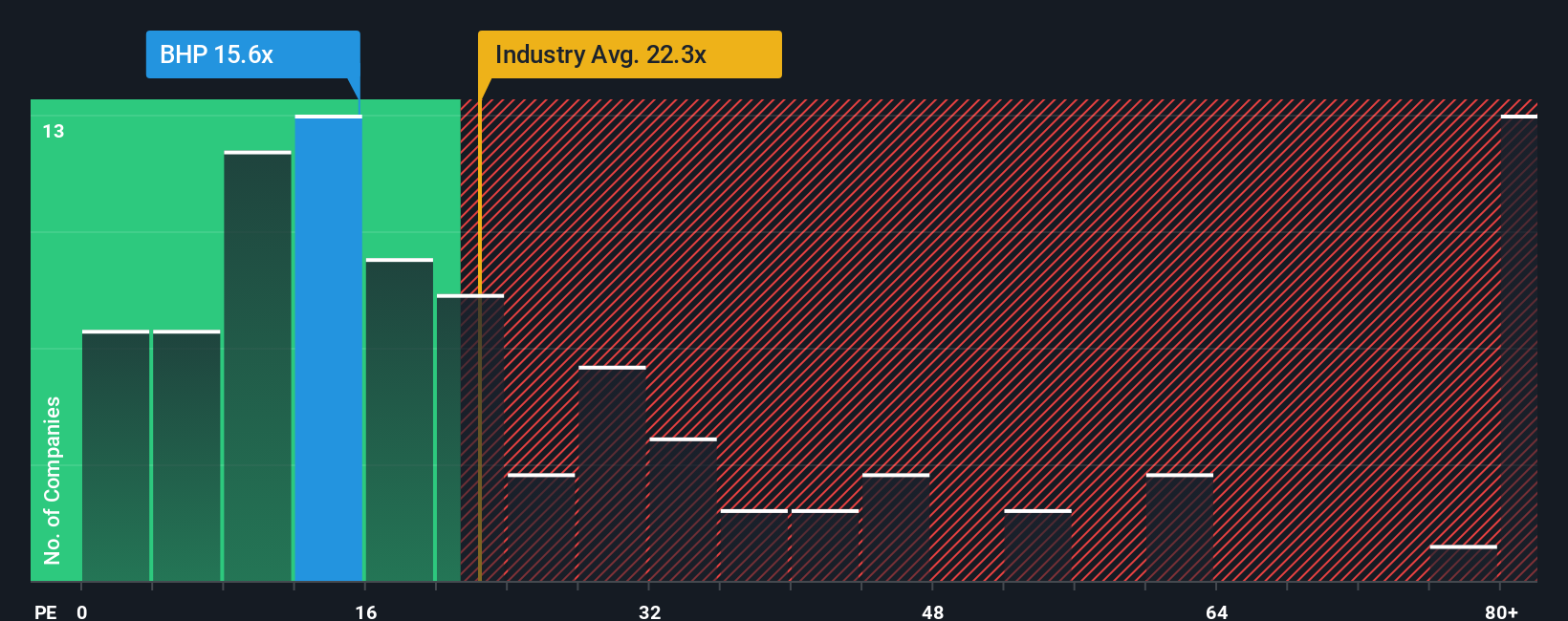

The price-to-earnings (PE) ratio is one of the most widely used ways to value a profitable company like BHP Group. This metric helps investors understand how much they are paying for each dollar of earnings. For established businesses with consistent profits, the PE ratio is particularly relevant, as it reflects market confidence in both the sustainability of current earnings and the future potential for growth.

However, a “normal” or “fair” PE ratio is not necessarily the same for every company. Higher growth expectations usually justify a higher PE, as investors are willing to pay a premium for future earnings. Risk factors, on the other hand, can pull the fair ratio down as they increase uncertainty around those future profits.

BHP Group's current PE ratio is 16.0x. This stands below the Metals and Mining industry average of 22.6x and the average of similar peers at 20.4x. Simply Wall St’s proprietary “Fair Ratio” for BHP, based on its growth outlook, profit margins, market cap, and unique risk profile, is calculated at 22.5x. The Fair Ratio goes deeper than a simple industry or peer comparison by considering the full context of the company’s fundamentals and future prospects.

Comparing BHP's actual PE of 16.0x to its Fair Ratio of 22.5x, the stock appears to be undervalued according to these metrics. This suggests the current market price may not fully reflect its earnings potential.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BHP Group Narrative

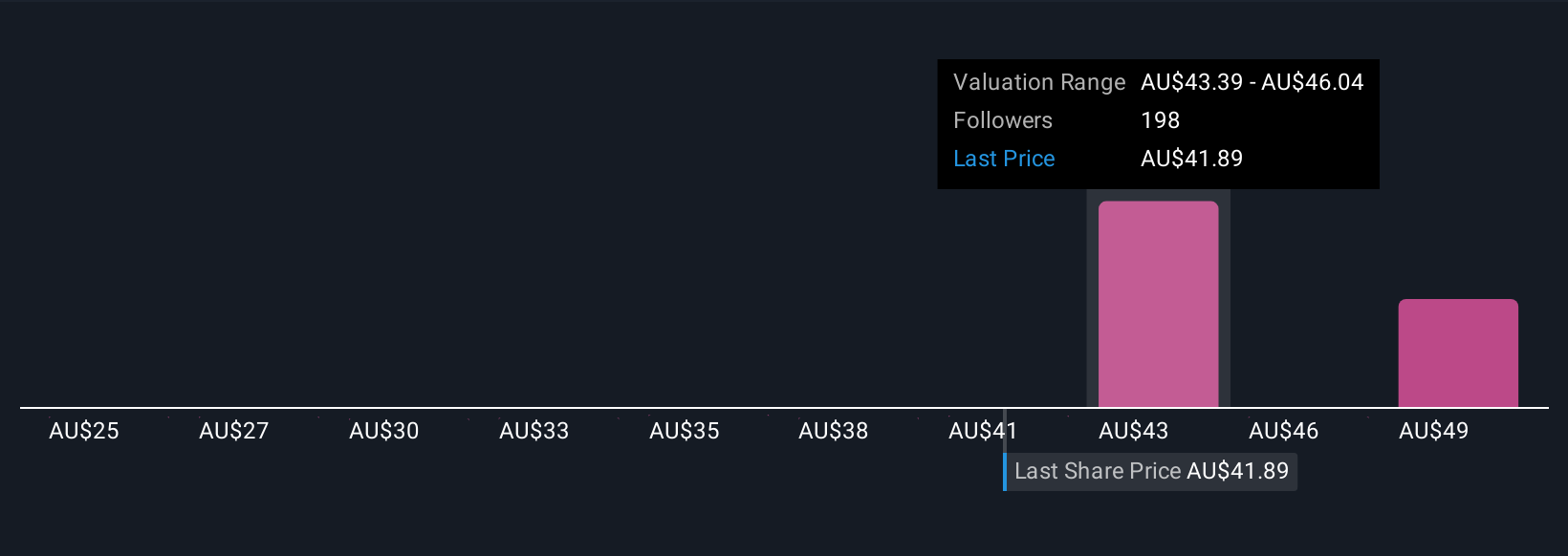

Earlier, we mentioned there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story about a company, built on your own expectations for its future, such as what you believe revenue, earnings, and margins will look like, rather than just relying on historical figures or consensus forecasts.

Narratives connect your perspective on how a company's story will unfold to specific financial assumptions and, ultimately, a fair value estimate. With Simply Wall St’s Narratives tool, used by millions of investors on the Community page, you can quickly craft or browse different outlooks for BHP Group.

This approach empowers you to decide when to buy, hold, or sell by directly comparing each Narrative’s Fair Value to the current share price. The best part is, Narratives update automatically as new information rolls in, so your investment thesis always stays current with news and earnings changes.

For example, while some investors set a higher fair value for BHP Group by forecasting strong demand for metals and resilient margins, others take a much more conservative view, factoring in risks like volatile iron ore prices and project execution challenges to arrive at a lower value. This proves that every investment decision is personal, and Narratives help you make it smarter.

Do you think there's more to the story for BHP Group? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if BHP Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:BHP

BHP Group

Operates as a resources company in Australia, Europe, China, Japan, India, South Korea, rest of Asia, North America, South America, and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion