- Australia

- /

- Metals and Mining

- /

- ASX:AMI

ASX Growth Companies With High Insider Ownership For February 2025

Reviewed by Simply Wall St

As the Australian market braces for the Reserve Bank's first interest rate decision of the year, investor sentiment remains cautious, with ASX 200 futures pointing to a lower open amid global economic uncertainties. In such a climate, growth companies with high insider ownership can offer a unique appeal; they often signal confidence from those closest to the business and may provide resilience against broader market fluctuations.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Medallion Metals (ASX:MM8) | 13.8% | 67.5% |

| Acrux (ASX:ACR) | 14.6% | 91.8% |

| Emerald Resources (ASX:EMR) | 18.1% | 34.7% |

| Newfield Resources (ASX:NWF) | 31.5% | 72.1% |

| AVA Risk Group (ASX:AVA) | 15.8% | 77.3% |

| Pointerra (ASX:3DP) | 23.8% | 126.4% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Let's dive into some prime choices out of the screener.

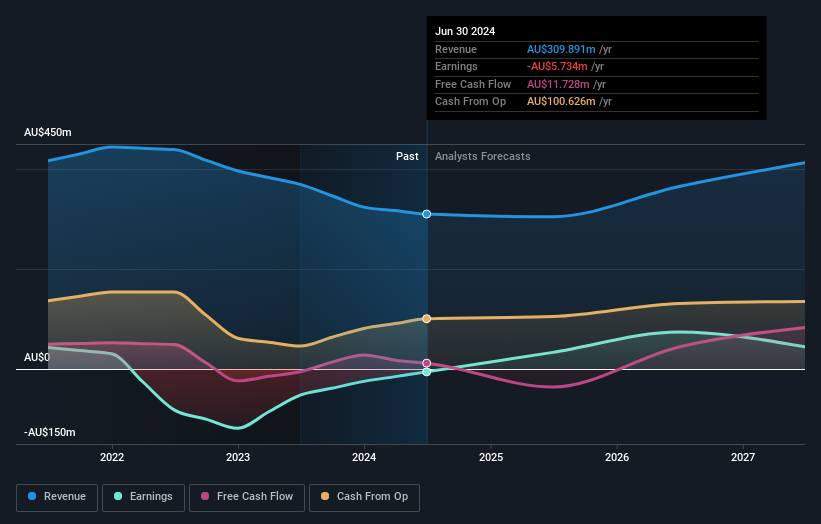

Aurelia Metals (ASX:AMI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Aurelia Metals Limited is an Australian company involved in the exploration and production of mineral properties, with a market capitalization of A$405.98 million.

Operations: The company's revenue is derived from its operations at the Peak Mine (A$207.34 million), Dargues Mine (A$102.36 million), and Hera Mine (A$0.20 million).

Insider Ownership: 23.2%

Revenue Growth Forecast: 10.6% p.a.

Aurelia Metals is trading significantly below its estimated fair value, suggesting potential undervaluation. The company is expected to achieve profitability within three years, with revenue growth projected at 10.6% annually, outpacing the Australian market average of 5.9%. Despite a low forecasted return on equity of 9.6%, insider ownership remains a positive indicator for alignment with shareholder interests. Upcoming Q2 2025 earnings results on January 29 may provide further insights into its financial trajectory.

- Click to explore a detailed breakdown of our findings in Aurelia Metals' earnings growth report.

- The analysis detailed in our Aurelia Metals valuation report hints at an deflated share price compared to its estimated value.

PolyNovo (ASX:PNV)

Simply Wall St Growth Rating: ★★★★★☆

Overview: PolyNovo Limited designs, manufactures, and sells biodegradable medical devices in the United States, Australia, New Zealand, and internationally with a market cap of A$1.32 billion.

Operations: The company generates revenue of A$103.23 million from the development, manufacturing, and commercialization of the NovoSorb technology.

Insider Ownership: 10.2%

Revenue Growth Forecast: 17.7% p.a.

PolyNovo's earnings are forecast to grow significantly at 38.2% annually, outpacing the Australian market's 12%. Despite revenue growth projections of 17.7% being below the desired threshold of 20%, they still surpass the market average of 5.9%. Insider activity shows more shares bought than sold recently, though not in substantial volumes. Trading at a notable discount to its estimated fair value, PolyNovo reported a promising A$59.9 million in revenue for H1 FY2025, up 22.8% year-over-year.

- Unlock comprehensive insights into our analysis of PolyNovo stock in this growth report.

- According our valuation report, there's an indication that PolyNovo's share price might be on the expensive side.

PWR Holdings (ASX:PWH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PWR Holdings Limited specializes in the design, prototyping, production, testing, validation, and sale of cooling products and solutions across various international markets with a market cap of A$841.72 million.

Operations: The company's revenue segments include PWR C&R at A$41.98 million and PWR Performance Products at A$111.26 million.

Insider Ownership: 13.2%

Revenue Growth Forecast: 12% p.a.

PWR Holdings' earnings are projected to grow at 15.6% annually, surpassing the Australian market's 12% growth rate. Revenue is expected to increase by 12% per year, outpacing the market average of 5.9%, although below the ideal growth threshold of 20%. The company boasts high insider ownership with no significant recent insider trading activity. PWR's Return on Equity is forecasted to reach a robust 26.5% in three years, indicating strong financial health and operational efficiency.

- Take a closer look at PWR Holdings' potential here in our earnings growth report.

- Our valuation report here indicates PWR Holdings may be overvalued.

Next Steps

- Embark on your investment journey to our 95 Fast Growing ASX Companies With High Insider Ownership selection here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:AMI

Aurelia Metals

Engages in the exploration and production of mineral properties in Australia.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives