Advertisement

- Australia

- /

- Diversified Financial

- /

- ASX:RMC

3 ASX Stocks Estimated To Be Trading At Discounts Of Up To 36.5%

Simply Wall St

Reviewed by Simply Wall St

The Australian market has recently experienced a slight downturn, with the ASX200 closing down 0.38% at 8,462 points, amidst sector-specific fluctuations such as a sell-off in Real Estate and modest gains in Materials and Information Technology. In this environment of mixed performance and economic adjustments, identifying undervalued stocks becomes crucial for investors seeking potential opportunities; these stocks are those trading below their intrinsic value despite broader market trends.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Accent Group (ASX:AX1) | A$2.53 | A$4.92 | 48.6% |

| MLG Oz (ASX:MLG) | A$0.625 | A$1.17 | 46.5% |

| Ingenia Communities Group (ASX:INA) | A$4.95 | A$9.24 | 46.4% |

| hipages Group Holdings (ASX:HPG) | A$1.11 | A$1.98 | 44% |

| Genesis Minerals (ASX:GMD) | A$2.41 | A$4.82 | 50% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Vault Minerals (ASX:VAU) | A$0.34 | A$0.65 | 47.8% |

| Energy One (ASX:EOL) | A$5.40 | A$10.52 | 48.7% |

| Ai-Media Technologies (ASX:AIM) | A$0.78 | A$1.38 | 43.3% |

| FINEOS Corporation Holdings (ASX:FCL) | A$1.93 | A$3.74 | 48.4% |

We'll examine a selection from our screener results.

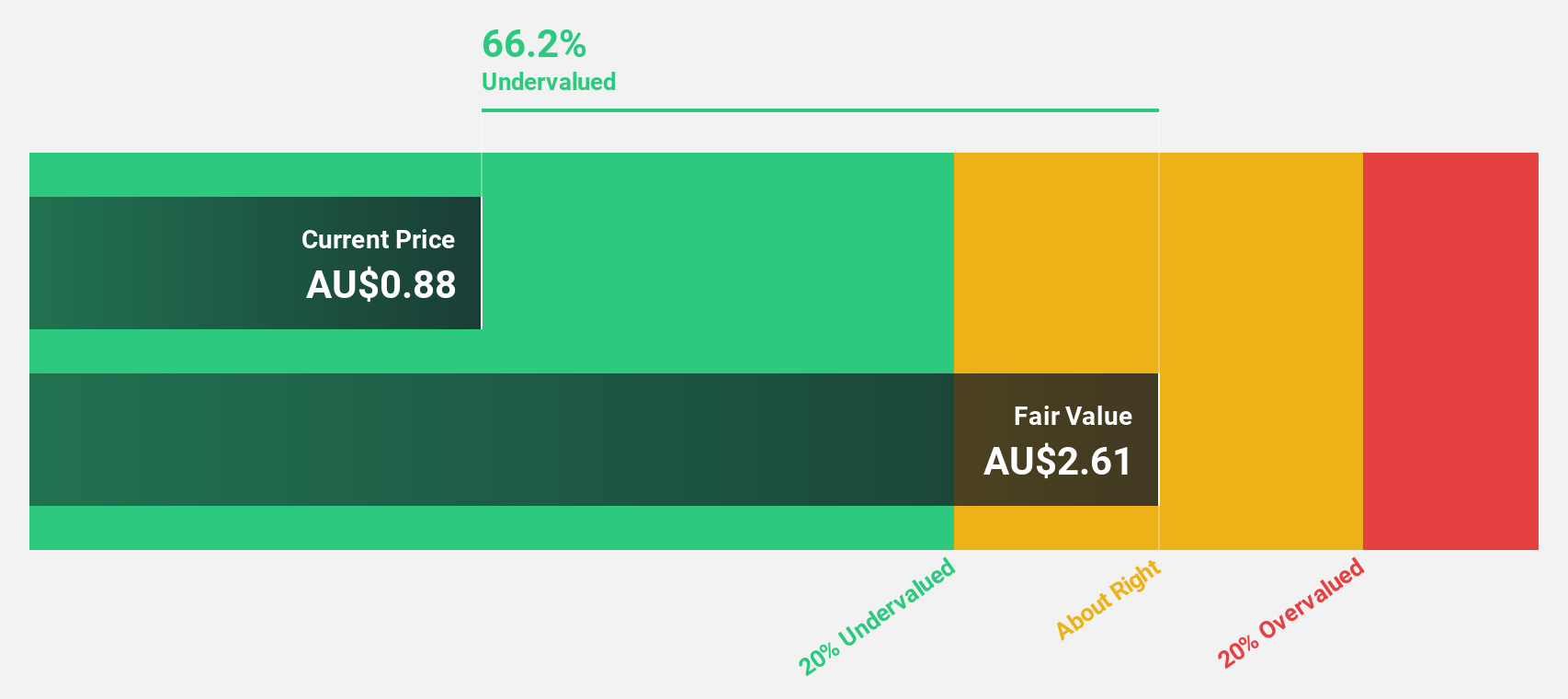

Resimac Group (ASX:RMC)

Overview: Resimac Group Limited is a financial services company offering residential mortgage and asset finance lending products in Australia and New Zealand, with a market capitalization of A$388 million.

Operations: The company's revenue segments include Home Loan Lending at A$123.16 million, New Zealand Lending at A$3.90 million, and Asset Finance Lending at A$20.21 million.

Estimated Discount To Fair Value: 32.6%

Resimac Group is trading at A$0.99, significantly below its estimated fair value of A$1.47, presenting a potential undervaluation based on cash flows. Despite high forecasted earnings and revenue growth of 22.7% and 32.9% per year respectively, concerns arise as dividends are not well covered by free cash flows and debt coverage from operating cash flow is inadequate. Recent executive changes include Pete Lirantzis' appointment as CEO amidst an ongoing share buyback program targeting 2.5% of issued capital.

- Our comprehensive growth report raises the possibility that Resimac Group is poised for substantial financial growth.

- Click here to discover the nuances of Resimac Group with our detailed financial health report.

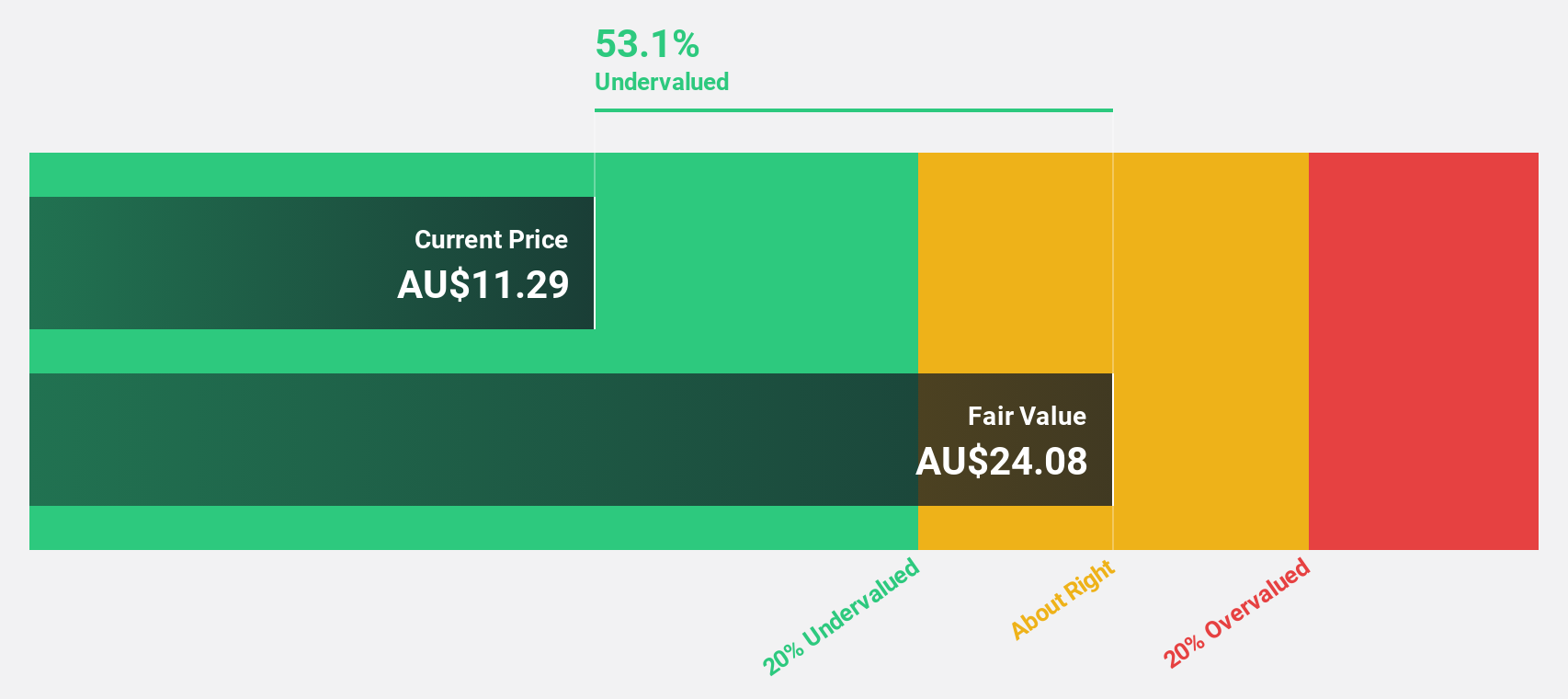

Sandfire Resources (ASX:SFR)

Overview: Sandfire Resources Limited is a mining company focused on the exploration, evaluation, and development of mineral tenements and projects, with a market capitalization of A$4.79 billion.

Operations: The company's revenue segments include the Motheo Copper Project generating $346.47 million, MATSA Copper Operations contributing $565.68 million, and Degrussa Copper Operations adding $29.40 million.

Estimated Discount To Fair Value: 33.1%

Sandfire Resources is trading at A$10.4, below its estimated fair value of A$15.56, suggesting undervaluation based on cash flows. Earnings are expected to grow 40.17% annually, outpacing the Australian market's average revenue growth of 5.8%. However, a forecasted low return on equity of 12.2% in three years and slower revenue growth at 8.6% per year could be concerns for investors evaluating long-term profitability prospects amidst recent executive changes and index adjustments.

- Upon reviewing our latest growth report, Sandfire Resources' projected financial performance appears quite optimistic.

- Dive into the specifics of Sandfire Resources here with our thorough financial health report.

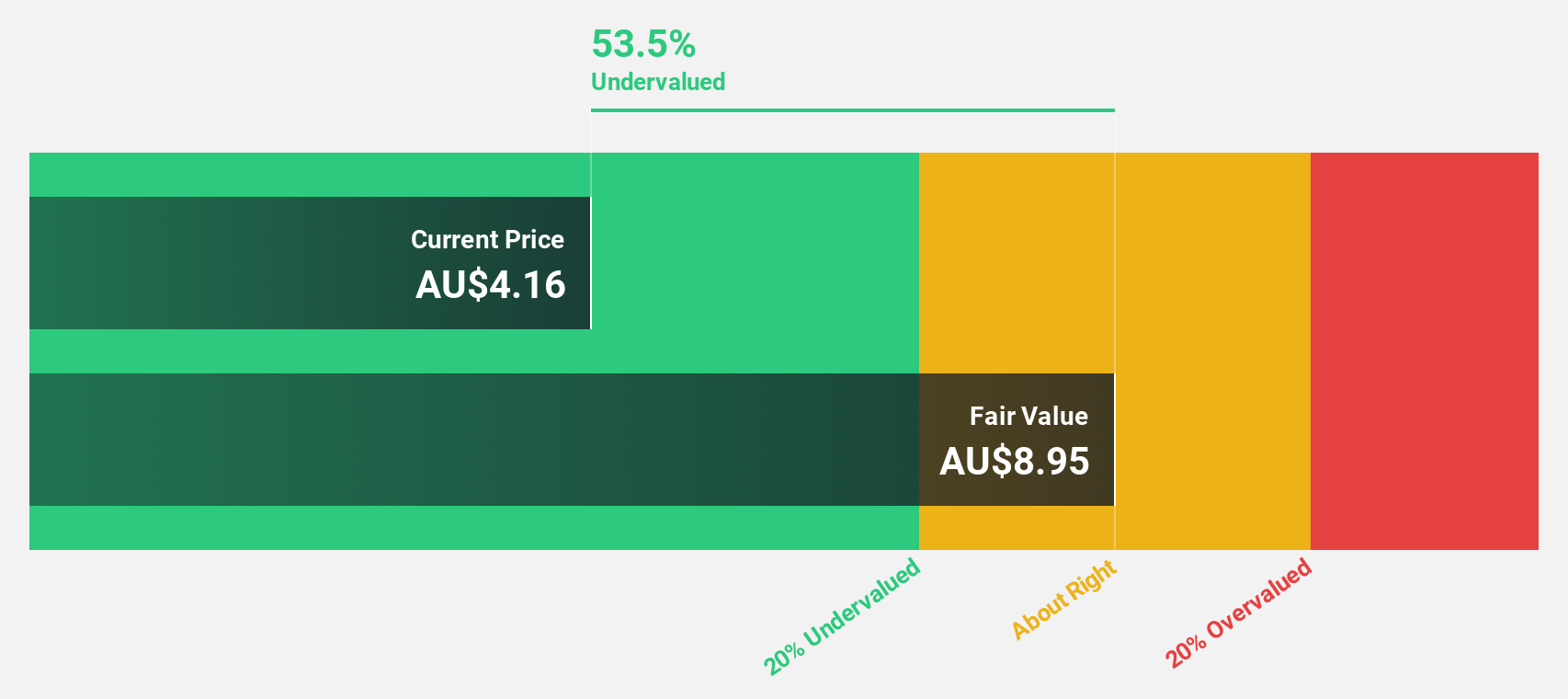

Select Harvests (ASX:SHV)

Overview: Select Harvests Limited is an Australian company involved in the cultivation, processing, packaging, and sale of almonds and related by-products, with a market cap of A$594.01 million.

Operations: The company generates revenue primarily through its almond segment, which accounts for A$337.29 million.

Estimated Discount To Fair Value: 36.5%

Select Harvests, trading at A$4.24, is undervalued based on cash flows with an estimated fair value of A$6.68. The company recently reported a significant turnaround, achieving A$337.29 million in sales and a net income of A$1.5 million for the year ended September 2024, up from a substantial loss previously. Although earnings are projected to grow significantly at 36.08% annually, challenges include past shareholder dilution and a forecasted low return on equity of 7.5%.

- In light of our recent growth report, it seems possible that Select Harvests' financial performance will exceed current levels.

- Unlock comprehensive insights into our analysis of Select Harvests stock in this financial health report.

Next Steps

- Investigate our full lineup of 35 Undervalued ASX Stocks Based On Cash Flows right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:RMC

Resimac Group

Provides residential mortgage and asset finance lending products in Australia and New Zealand.

High growth potential and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor