Advertisement

- Australia

- /

- Diversified Financial

- /

- ASX:HLI

Investors Aren't Buying Helia Group Limited's (ASX:HLI) Earnings

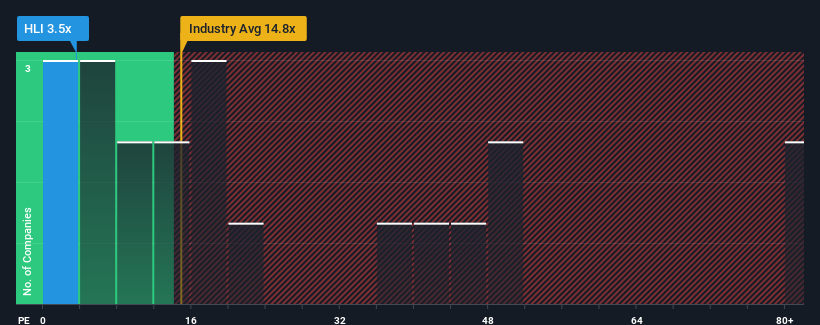

When close to half the companies in Australia have price-to-earnings ratios (or "P/E's") above 19x, you may consider Helia Group Limited (ASX:HLI) as a highly attractive investment with its 3.5x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Recent times have been advantageous for Helia Group as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Helia Group

Is There Any Growth For Helia Group?

The only time you'd be truly comfortable seeing a P/E as depressed as Helia Group's is when the company's growth is on track to lag the market decidedly.

If we review the last year of earnings growth, the company posted a terrific increase of 61%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to slump, contracting by 19% per annum during the coming three years according to the three analysts following the company. Meanwhile, the broader market is forecast to expand by 17% each year, which paints a poor picture.

With this information, we are not surprised that Helia Group is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Helia Group's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Helia Group maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 3 warning signs for Helia Group (2 can't be ignored!) that you should be aware of.

You might be able to find a better investment than Helia Group. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Helia Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:HLI

Helia Group

Helia Group Limited, together with its subsidiaries, is involved in the loan mortgage insurance business primarily in Australia.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor