Advertisement

Shareholders Would Not Be Objecting To Waterco Limited's (ASX:WAT) CEO Compensation And Here's Why

Key Insights

- Waterco will host its Annual General Meeting on 25th of October

- CEO Soon Goh's total compensation includes salary of AU$469.6k

- The total compensation is similar to the average for the industry

- Waterco's total shareholder return over the past three years was 55% while its EPS grew by 52% over the past three years

The performance at Waterco Limited (ASX:WAT) has been quite strong recently and CEO Soon Goh has played a role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 25th of October. It is likely that the focus will be on company strategy going forward as shareholders hear from the board and cast their votes on resolutions such as executive remuneration and other matters. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

See our latest analysis for Waterco

Comparing Waterco Limited's CEO Compensation With The Industry

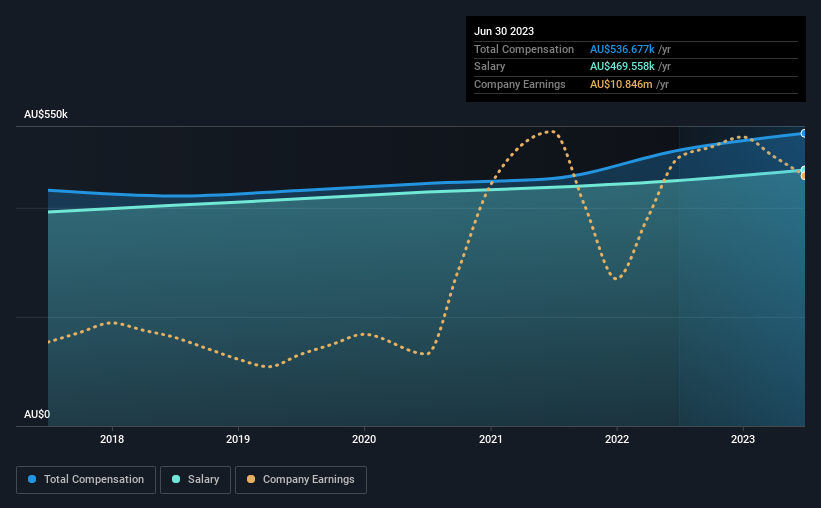

Our data indicates that Waterco Limited has a market capitalization of AU$149m, and total annual CEO compensation was reported as AU$537k for the year to June 2023. That's a modest increase of 6.1% on the prior year. We note that the salary portion, which stands at AU$469.6k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the Australia Leisure industry with market capitalizations below AU$316m, reported a median total CEO compensation of AU$490k. So it looks like Waterco compensates Soon Goh in line with the median for the industry. What's more, Soon Goh holds AU$81m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$470k | AU$450k | 87% |

| Other | AU$67k | AU$56k | 13% |

| Total Compensation | AU$537k | AU$506k | 100% |

Speaking on an industry level, nearly 44% of total compensation represents salary, while the remainder of 56% is other remuneration. Waterco is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Waterco Limited's Growth Numbers

Waterco Limited's earnings per share (EPS) grew 52% per year over the last three years. It achieved revenue growth of 4.6% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Waterco Limited Been A Good Investment?

Most shareholders would probably be pleased with Waterco Limited for providing a total return of 55% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. Instead, investors might be more interested in discussions that would help manage their longer-term growth expectations such as company business strategies and future growth potential.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 1 warning sign for Waterco that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Waterco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:WAT

Waterco

Manufactures, wholesales, and exports equipment and accessories in the swimming pool, spa pool, spa bath, rural pump, and water treatment industries in Australia, New Zealand, Asia, North America, and Europe.

Mediocre balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|3.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|19.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor